The hard question for a supply chain management control tower in 2026 is not whether it can see more exceptions. Most of them can. The question is whether anything useful happens after the exception appears.

That distinction matters because the category is still high on investment lists while its operational record remains uneven. FourKites cites a finding that only 22% of shippers with more than $1 billion in revenue rate their control towers as “highly effective at driving action,” even though control towers were sold precisely as a way to move from fragmented monitoring to coordinated response.[1] Blue Yonder’s 2026 Supply Chain Compass adds the demand-side pressure: 37% of organizations named control towers as a 2026 priority, up 6 points, while the share of leaders who felt ready for the future fell from 73% in 2025 to 66% in 2026.[2]

That is the effectiveness gap. Control towers are becoming more important at the same time that buyers are less willing to confuse awareness with action. A screen that tells a planner a shipment is late may be useful. A system that predicts the miss, recommends a feasible recovery path, books the alternate move, updates the customer commitment, and records why it acted is a different use case entirely.

The value sits between alert and action

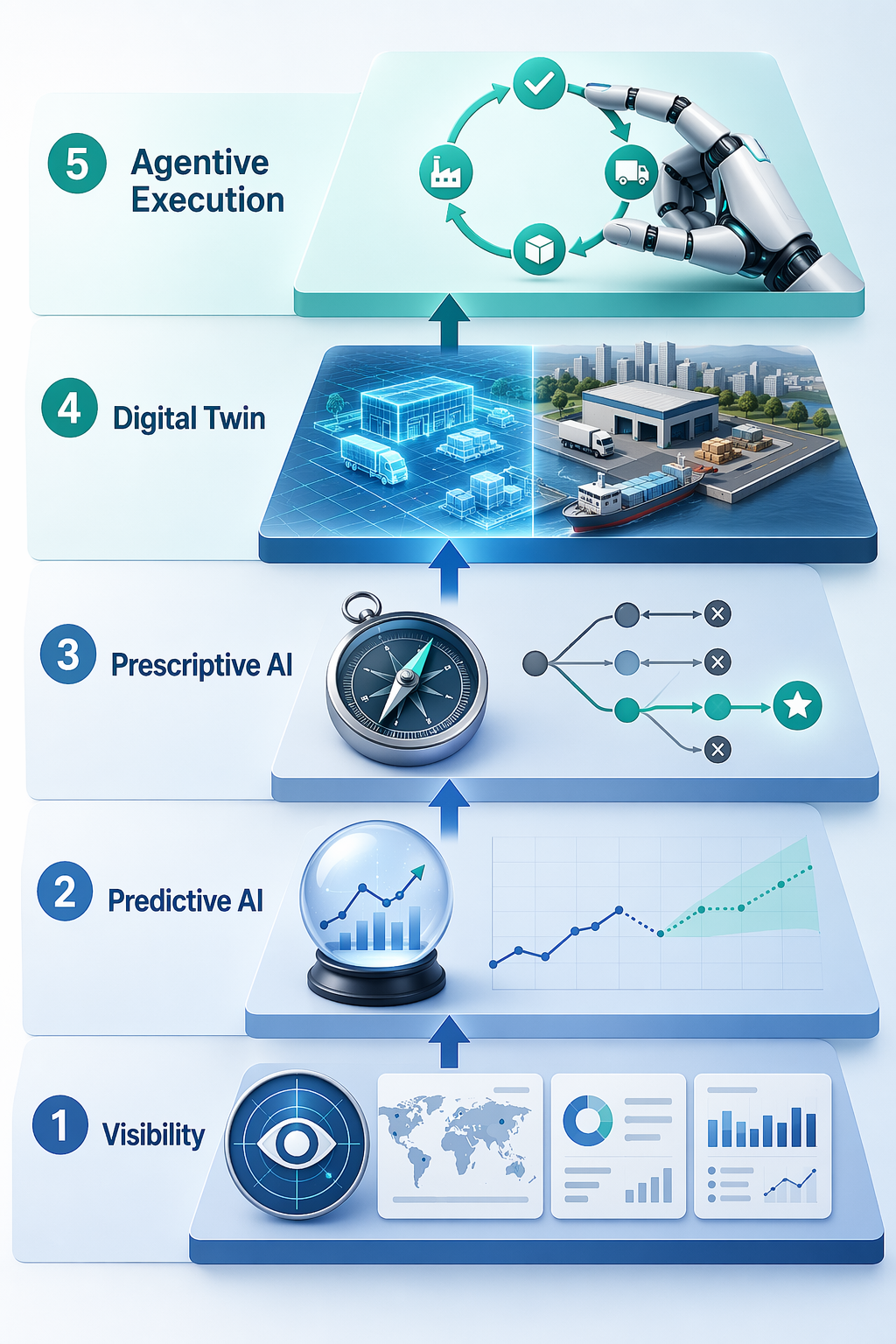

A modern control tower has to be evaluated as a capability gradient, not as a single product label. At the low end, visibility platforms aggregate status, location, inventory, and risk signals. One level up, predictive AI estimates what is likely to happen next: a missed appointment, a stockout, a late supplier delivery, a route failure. Prescriptive AI then recommends a response. Digital twins let teams test the response against a simulated operating model. Agentive execution closes the loop by carrying out selected actions within approved limits.

This is where many first-generation programs lost their way. They improved the alert surface without reducing the clerical load beneath it. Gartner has been cited for the estimate that an average disruption can require 34 manual system updates across 6 platforms.[3] Whether a buyer is evaluating logistics, inventory, fulfillment, supply assurance, or end-to-end control tower scope, that is the work that decides the business case: who updates the transportation management system, who changes the order promise, who notifies the customer, who rebalances inventory, who approves the premium freight, and who leaves an audit trail.

The cleanest way to separate the tiers is to ask what the platform can do when a disruption is detected.

| Capability tier | What it mainly does | Where value can show up | Procurement question |

|---|---|---|---|

| Visibility | Aggregates events, statuses, alerts, and milestones | Faster awareness, fewer blind spots, better escalation | Does it reduce work, or only expose more work? |

| Predictive AI | Estimates future service, cost, or inventory risk | Earlier intervention and fewer surprise failures | What decisions change because the prediction arrives earlier? |

| Prescriptive AI | Ranks options and recommends corrective actions | Lower planner effort, better exception prioritization | Can users see the assumptions behind the recommendation? |

| Digital twin | Simulates scenarios against a model of the network | Better trade-off analysis before changing plans | Is the model fed by current operating data or periodic extracts? |

| Agentive execution | Executes approved workflows or transactions autonomously | Reduced handoffs, faster recovery, auditable automation | Which actions can it complete without a human rekeying the decision? |

The category language can be slippery, so functional taxonomy still has a role. IBM describes five control tower types: logistics, inventory, fulfillment, supply assurance, and end-to-end.[4] That classification helps define the operating domain. It does not, by itself, tell a buyer whether the system is passive, predictive, prescriptive, simulated, or execution-capable. For teams that need a more operational breakdown, the control tower functional clusters view is useful because it separates planning visibility, flow control, impact analysis, and response coordination rather than treating every tower as one thing.

What measurable value has been documented?

The strongest ROI claims are attached to platforms that go beyond visibility. FourKites says AI-powered control towers can achieve 4-8 month payback periods, compared with 12-24 month implementations for traditional approaches.[1] That is a prominent benchmark, but it should be treated carefully: it is vendor-reported, not an independently audited industry average. It is still useful as a directional signal because the same source ties the payback logic to a different operating model: fewer manual interventions, faster exception handling, and automation across the alert-to-action loop.

The case evidence in that same material is more concrete. FourKites describes a top-15 food manufacturer using its Intelligent Control Tower and reporting more than $500,000 in detention cost reduction, $800,000 in OTIF penalty reduction, and a 35% improvement in logistics productivity.[1] Those are the kinds of metrics that matter because they land in operating accounts rather than adoption dashboards. Detention falls when loads, appointments, facilities, and carriers are coordinated earlier. OTIF penalties fall when at-risk orders are recovered before a service miss. Logistics productivity improves when coordinators stop chasing the same exception across multiple systems.

Accenture’s control tower materials give a broader, less vendor-specific range: 3-5% logistics cost reduction and 10-20% labor efficiency improvement.[5] Those ranges are not proof that every program clears the hurdle. They do, however, set a reasonable expectation for business-case modeling when the tower is connected to transportation, inventory, fulfillment, and exception-resolution workflows rather than standing beside them as a reporting layer.

The older McKinsey nerve-center research is still relevant for the labor side of the case. In January 2021, McKinsey wrote that 40-60% of planners’ time was spent on transactional activities rather than strategic work, and cited 20-50% forecast-error reductions from supply chain nerve-center approaches.[6] The timing matters: this predates the current generative and agentic AI cycle. But the structural problem has not disappeared. If a control tower leaves planners reconciling alerts, copying data, and coordinating approvals manually, the automation claim is mostly cosmetic.

McKinsey also described a pharmaceutical company receiving more than 200 exception messages per day after implementation.[6] That example should make buyers pause. More exception visibility can be a regression if no one redesigns triage, thresholds, ownership, and resolution paths. A control tower that generates 200 daily messages has not necessarily created intelligence; it may have industrialized interruption.

Digital twin claims sit one level higher on the capability gradient. nShift’s 2026 mid-year analysis cites BCG data that early digital-twin adopters achieved 20-30% better forecast accuracy and 50-80% fewer delays.[7] Those figures should not be read as a guaranteed control tower outcome. They are better read as evidence that simulation and current operating data can improve decisions when the model is close enough to the real network to test feasible actions, not just idealized plans.

Across these sources, the pattern is consistent enough to be useful for procurement. Visibility can create value, especially where the baseline is fragmented and opaque. Predictive and prescriptive capabilities create more value when they change the timing and quality of intervention. Agentive execution has the largest upside when it eliminates the manual updates, approvals, and handoffs that currently sit between diagnosis and correction. For broader ROI comparison across supply chain AI categories, the supply chain AI use case ROI benchmark view is the more appropriate frame.

Vendor classes are more useful than vendor labels

The market is often described as if every platform is converging on the same destination. That is too generous. Most vendors are adding AI language, but they do not start from the same system of record, do not control the same execution workflows, and do not have the same right to act.

A better shortlist starts with archetypes.

| Archetype | Typical center of gravity | Representative vendors | Best-fit question |

|---|---|---|---|

| Visibility-led | Tracking, milestones, alerts, shipment visibility, partner signals | Project44, E2open, FourKites in its visibility-plus-AI posture | Do we mainly need cleaner external visibility, or do we need the platform to change execution? |

| Planning-led | Demand, supply, inventory, S&OP, allocation, scenario planning | Blue Yonder, Kinaxis, o9 Solutions | Will better planning decisions flow into executable transactions quickly enough? |

| Execution-native | Dispatch, routing, carrier assignment, fulfillment operations, workflow automation | Locus, logistics execution layers, agentic control tower platforms | Which decisions can the system carry out without manual rekeying? |

| ERP-suite native | Enterprise process integration, master data, finance and order context | SAP, Oracle | Is native integration more valuable than specialized network depth? |

Blue Yonder is best understood as planning-led, embedded in the Luminate platform. That can be powerful when the organization’s pain is tied to demand-supply balancing, inventory positioning, and planning decisions that need broader network context. The buyer’s question is whether the corrective actions can move from plan to execution without falling back into manual coordination.

Kinaxis and o9 Solutions also sit closer to the planning and scenario-modeling side than to pure execution. Kinaxis is associated with concurrent planning and rapid scenario comparison. o9 frames its platform around an integrated “digital brain.” These approaches are valuable when the decision problem is network-wide trade-off analysis: what to prioritize, where to allocate constrained supply, how to rebalance demand and capacity. They are weaker fits if the immediate requirement is automated transportation execution after a facility delay or carrier failure.

FourKites, Project44, and E2open are easier to understand if the starting point is visibility. Project44 is strongly associated with transportation visibility and track-and-alert workflows. E2open brings a broader connected-network footprint. FourKites has pushed from real-time visibility into predictive and prescriptive control tower capabilities, which is why its ROI claims are tied to intelligent exception handling rather than location tracking alone.[1] For buyers, the issue is not whether these platforms can show better data. It is how far they can go into decisioning and whether execution still depends on another system and another human.

Locus represents a more execution-native posture, especially around automated dispatch, routing, and field logistics decisions. That matters when the control tower must do more than tell a dispatcher that the plan is broken. If the platform can re-sequence routes, adjust assignments, and push changes into the operational workflow, the cost case looks different from a visibility dashboard that waits for someone else to act.

SAP and Oracle are separate evaluation cases because they sit inside larger enterprise application estates. SAP-native control tower capabilities may appeal where S/4HANA process integration, master data governance, and enterprise standardization matter more than best-of-breed logistics depth. Oracle’s Supply Chain Command Center is notable for its AI-agent direction, with 13+ AI agents described in the site profile, which puts it closer to the AI-native command-center conversation than a classic dashboard module. The deeper vendor comparisons belong in the supply chain AI vendor directory, the SAP supply chain control tower profile, and the Oracle Supply Chain Command Center profile.

Autonomy changes the buying test

The jump from prescriptive recommendation to autonomous action is not just a feature upgrade. It changes liability, governance, and operating design. A system that recommends expediting a shipment leaves the approval burden with a planner. A system that books the expedite within policy consumes budget, changes capacity, affects carrier commitments, and may alter customer promises. That is why autonomous control tower discussions need to be tied to approval thresholds, exception classes, role design, and auditability from the beginning.

The practical transition usually starts with bounded autonomy. Low-risk actions can be automated first: notifying stakeholders, enriching an exception with root-cause context, updating an ETA, generating a recovery option, or routing an approval to the right owner. Higher-risk actions need tighter controls: authorizing premium freight, reallocating constrained inventory, changing customer commitments, or overriding a production plan.

That is the point where the control tower becomes part of the oversight model, not just the operations model. Human-in-the-loop, human-on-the-loop, and exception-only governance are different designs. A logistics team may allow the system to reassign local delivery routes automatically while requiring human approval for carrier substitution above a cost threshold. A planning team may allow automated scenario generation while reserving allocation decisions for planners during shortage conditions. The AI oversight spectrum for supply chain is useful here because the same control tower can contain several autonomy levels at once.

For logistics-heavy use cases, the agentic version is already becoming its own buying category. The relevant test is whether the platform can observe an event, decide on the next best action, execute through connected systems, and monitor the result. That narrower logistics pattern is covered in more depth in agentic logistics control towers.

The implementation risk starts before the algorithm

The most avoidable failure is buying a decision engine before the event data can support decisions. nShift’s 2026 analysis calls event-capture data quality the most underfunded and most critical layer of the control tower stack.[7] That is exactly right operationally. If appointment events are late, carrier milestones are inconsistent, inventory positions are stale, supplier confirmations are unreliable, or order priorities are not encoded, the AI layer will spend its time making confident recommendations from weak signals.

Data readiness is not a generic cleansing project. For a control tower, the useful questions are tied to decisions:

- Which events arrive early enough to change the outcome?

- Which systems must be updated after a decision is made?

- Which master data fields determine feasible options, such as carrier eligibility, customer priority, facility constraints, and inventory availability?

- Which actions require approval, and which can be executed inside policy?

- Which decisions need a retained explanation for audit, dispute resolution, or customer review?

That list is more useful than a generic “single source of truth” requirement. A control tower does not need perfect data everywhere before it creates value. It does need reliable data for the specific decisions it is expected to automate or recommend. A logistics detention use case needs different event fidelity than an allocation-control use case. A supply assurance tower needs different supplier and purchase-order signals than a last-mile dispatch tower. The supply chain AI data quality checklist is the right prerequisite work before an organization lets a control tower move from alerting into execution.

Integration depth is the second prerequisite. A platform that predicts a late inbound delivery but cannot update allocation logic, transportation plans, customer commitments, or inventory projections will still depend on manual bridges. Those bridges are where cycle time, errors, and accountability gaps accumulate. The 34-update disruption estimate is uncomfortable because it names the hidden work that dashboards rarely remove.[3]

The third prerequisite is operating design. If every exception still routes to the same queue, the platform has not changed the work. Buyers should insist on seeing how the system suppresses noise, assigns ownership, escalates only when needed, and records closed-loop outcomes. Without that, the control tower may raise the maturity of monitoring while lowering the productivity of the people expected to respond.

How to judge whether the business case is real

A credible control tower business case should be built around named decisions, not broad visibility claims. “Improve supply chain visibility” is not specific enough. “Reduce detention by predicting facility congestion and rescheduling appointments before dwell accumulates” is specific enough to model. “Improve service” is too broad. “Reduce OTIF penalties by identifying at-risk orders, recommending recovery actions, and updating commitments through connected execution systems” is testable.

The evaluation should track four measurements before and after implementation: exception volume, manual touches per exception, cycle time from detection to action, and business outcome movement. If exception volume rises but manual touches do not fall, the platform may have improved sensing without improving work. If recommendations are accepted but execution still happens outside the system, the ROI will depend on human follow-through. If actions execute automatically but the audit trail is weak, the risk has moved from inefficiency to governance.

That is also how to keep vendor demos honest. Ask the vendor to walk through one disruption after the alert fires. Which data sources detect it? Which model predicts the impact? Which alternatives are generated? Which constraints are checked? Which system executes the chosen action? Which human approves or monitors it? Which record proves what happened? If the answer turns back into dashboards and emails, the product may still be useful, but it is not the same value proposition as an AI-powered decision-and-execution layer.

AI-powered supply chain control towers can deliver measurable value. The evidence is strongest when the platform closes the alert-to-action loop, has enough event and execution data to act on, and is governed for semi-autonomous or autonomous decisions. Visibility-only towers may still be worth buying for fragmented networks. They should not be priced, evaluated, or sold as if they deliver the same operating leverage as systems that predict, prescribe, simulate, execute, and leave a decision trail.

References

- Why Supply Chain Control Towers Didn't Deliver on Their Promise, FourKites

- Blue Yonder Releases 2026 Supply Chain Compass Survey, BusinessWire, March 2026

- Agentic AI in Supply Chain Management: From Visibility to Action, Locus

- What is a supply chain control tower?, IBM

- Benefits of Supply Chain Control Tower Solutions, Accenture

- Reimagining the supply-chain control tower, McKinsey & Company, January 2021

- Supply chain control tower 2026: dashboard to decision, nShift, 2026

Comments

Join the discussion with an anonymous comment.