The useful question after Nvidia’s FY2026 results is not whether AI infrastructure demand is real. It is. The useful question is whether a supply chain leader should change the next planning-cycle budget for a warehouse safety model, freight audit workflow, demand-planning copilot, or procurement assistant because Nvidia’s stock just moved.

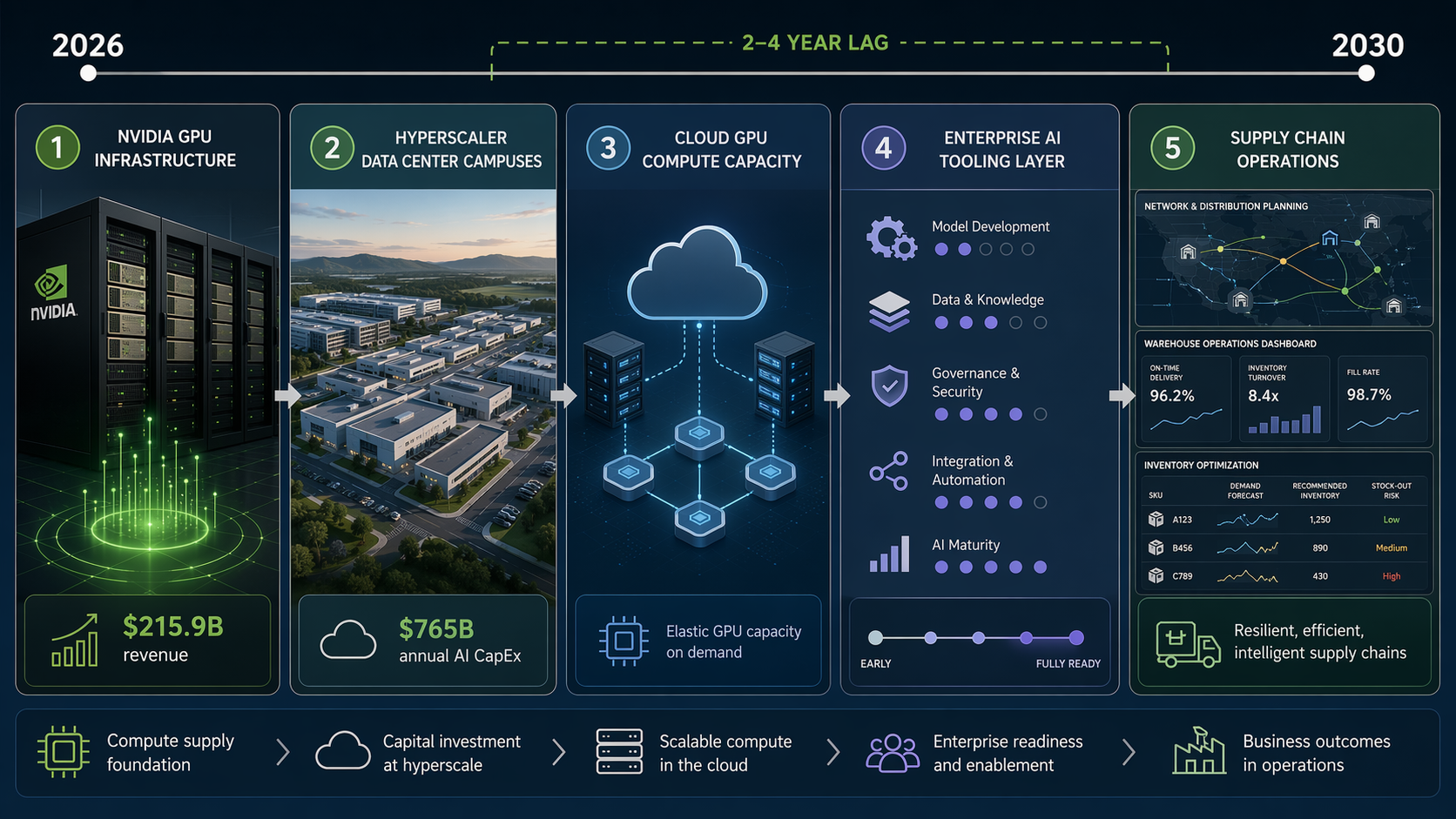

The short answer: treat Nvidia as an infrastructure confidence indicator, not as a budget trigger. Nvidia’s $215.9 billion in FY2026 revenue, 65% year-over-year growth, $123.3 billion in net income, $97 billion in free cash flow, and 93% year-over-year growth in its Data Center segment are too large to dismiss as market theatre.[1] But supply chain AI tooling sits several layers downstream from GPU orders. Stock moves can tell you how investors feel about the AI build-out this week; they do not tell you whether your transportation team has clean enough accessorial data to automate invoice exceptions next quarter.

The Signal Is Strong, But It Is Not Direct

There is a reason executives reach for Nvidia first. It is the cleanest public scorecard for the upstream AI infrastructure cycle: chips, systems, networking, data center demand, and the hyperscaler appetite behind them. When Nvidia’s Data Center revenue grows the way it did in FY2026, it says cloud platforms, model developers, and large enterprise infrastructure buyers are still committing capital to AI capacity.[1]

That matters for supply chain teams because the tools they eventually buy depend on this upstream build-out. Lower-latency planning assistants, multimodal warehouse monitoring, exception-handling agents, and simulation-heavy network design all benefit when compute becomes more available and vendors can spread infrastructure costs across a wider base of customers.

But the translation path is long. Nvidia sells into infrastructure demand. Supply chain leaders buy workflow outcomes. Between those two points sit hyperscaler capital budgets, cloud GPU availability, model economics, software vendor packaging, data integration, security review, change management, and the operational question nobody can outsource: whether the use case saves money or improves service at a level that survives budget scrutiny.

| Signal | What It Can Tell A Supply Chain Leader | What It Cannot Tell Them |

|---|---|---|

| Nvidia revenue and Data Center growth | AI infrastructure spending remains large and visible | A specific supply chain AI use case is ready to scale |

| Hyperscaler capex | Cloud providers are still building capacity | Enterprise software prices will fall on a fixed schedule |

| Nvidia stock reaction | Investor sentiment toward the AI build-out has changed | Warehouse, freight, planning, or procurement AI budgets should be accelerated or frozen |

| Supply chain AI adoption surveys | Interest and budget activity are moving | Teams trust autonomous decisions in critical workflows |

The $40 Billion Question Behind “Demand”

The harder part of reading Nvidia is that not all demand signals are equally clean. CNBC reported in May 2026 that Nvidia had made more than $40 billion in equity bets across the AI ecosystem, including $30 billion tied to OpenAI, $3.2 billion to Corning, $2.1 billion to IREN, $2 billion to Marvell, $2 billion each to Lumentum and Coherent, $2 billion to CoreWeave, and $2 billion to Nebius.[2]

For an operator, that list changes the way the revenue signal should be read. Equity investment can be a rational way to secure supply chains, expand capacity, support strategic customers, and deepen a platform ecosystem. It can also make the demand picture harder to parse when some recipients are current or potential buyers of Nvidia-powered infrastructure.

The right conclusion is not that demand is fake. The available evidence does not support that. The right conclusion is that some portion of the AI infrastructure cycle may be supplier-supported, customer-concentrated, or strategically financed, so supply chain teams should avoid converting headline GPU demand into a straight-line forecast for enterprise application readiness.

Analysts do not agree on how troubling this is. CNBC reported Wedbush’s view that Nvidia’s investment activity strengthens its moat, while Mizuho characterized some neocloud bets as “questionable” and said the pattern “smells like pre-funding GPU purchases.”[2] That is a tension, not a verdict. A supply chain budget owner does not need to settle the capital-markets argument. They only need to avoid using a potentially circular infrastructure signal as if it were direct evidence that a vendor’s inventory optimization agent, dock-door vision model, or invoice audit product is ready for enterprise-wide rollout.

This is where boardroom shortcuts get expensive. If Nvidia’s investment portfolio is read only as proof of unstoppable end-user demand, AI budgets can get pulled forward before data and governance are ready. If it is read only as circular financing, useful projects can get paused even when the operating case is already proven. Both reactions confuse capital structure with deployment evidence.

Capex Can Be Real And Still Arrive Late For Enterprise Buyers

Goldman Sachs’ AI infrastructure tracking puts the scale in context: a baseline estimate of $765 billion in annual AI capital expenditure in 2026 and $7.6 trillion cumulatively by 2031.[3] Those numbers support the view that infrastructure build-out is not a niche cycle. They also explain why Nvidia remains such a watched proxy for AI spending.

The useful caveat is buried in the economics rather than the headline. Goldman Sachs notes that assumptions about the useful life of AI silicon can shift aggregate costs by hundreds of billions of dollars.[3] If chips have shorter productive lives than buyers expect, depreciation pressure, upgrade cycles, and cloud pricing economics look different. If useful lives stretch longer, the cost curve can improve. Neither outcome maps neatly onto a supply chain application roadmap.

For supply chain AI, a 2-4 year lag is a practical assumption, not a law of physics. Infrastructure has to become available, model providers have to turn it into usable capabilities, enterprise software vendors have to package those capabilities into workflows, and customers have to integrate them with messy systems of record. A planning assistant that can explain forecast variance is not purchased directly from a data center capex line. It shows up after several rounds of productization, security review, customer proof, and operating model redesign.

That delay should shape budget timing. Infrastructure strength justifies keeping an AI roadmap alive and funded. It does not justify skipping the usual gates: data availability, workflow ownership, measurable benefit, exception handling, and accountability when the model is wrong. The closer a use case is to back-office review work, the easier it is to test now. The closer it is to autonomous decisions that affect service, safety, inventory, or customer commitments, the more the lag matters.

The June Selloff Was A Warning About Mood Swings

The June 2026 chip-stock selloff is useful because it shows how fast sentiment can outrun operating reality. The reported episode included a single-session loss of more than $300 billion in Nvidia market capitalization and a 10% drop in SOXX, even as hyperscaler capex commitments for 2026 were still described at roughly $750 billion.[4]

That is exactly the kind of market move that can distort an internal budget meeting. A CFO sees chip stocks fall, an executive committee gets nervous, and suddenly a supply chain analytics team is asked whether its AI roadmap should be slowed. The underlying question may be legitimate: are vendors overpromising, are costs sustainable, are pilots delivering? But a one-day stock move is the wrong instrument for answering it.

The better use of volatility is as a stress test. If a project only survives when Nvidia’s stock is making new highs, it was never really budgeted on operational value. If a project still has a clear payback case when chip sentiment turns negative, it belongs in the portfolio discussion on its own merits.

Adoption Signals Are Positive, But Readiness Is Uneven

Broad AI adoption surveys show momentum. NVIDIA’s State of AI Survey, based on more than 3,200 respondents, reported that 86% were increasing AI budgets in 2026 and 88% reported AI-driven revenue increases.[5] That is a meaningful attitudes-and-budget signal across industries. It should not be mistaken for proof that supply chain teams are ready to hand critical decisions to autonomous systems.

The narrower supply chain evidence is more cautious. A RELEX survey of roughly 500 retail, wholesale, and manufacturing respondents found that only 10% of supply chain leaders trusted AI to make critical decisions autonomously.[6] That difference is not a contradiction. It is the gap between increasing AI budgets and trusting AI with decisions that can create stockouts, missed shipments, unsafe warehouse behavior, or bad supplier commitments.

Gartner’s supply chain management agentic AI forecast points in the same direction from a market-sizing angle, with the category expected to grow from under $2 billion in 2025 to $53 billion by 2030.[7] Because this citation relies on secondary confirmation rather than the full Gartner methodology, the number is best treated as a directional marker: agentic supply chain AI is expected to grow quickly, but the large spend curve is still ahead, not fully present in today’s operating budgets.

This is why the phrase “AI demand” needs narrowing in a supply chain budget review. Demand for accelerators is not the same as demand for autonomous replenishment. Budget increases for AI are not the same as production trust. A vendor demo is not the same as a controlled rollout across distribution centers, lanes, suppliers, and planning regions.

What To Do At The Budget Table

A supply chain AI budget should not ignore Nvidia. It should put Nvidia in the right column. Track the company’s revenue growth, Data Center segment, free cash flow, customer concentration, and investment activity as infrastructure confidence signals. Use them to judge whether the broader AI capacity cycle is still being funded.

Then make the actual spend decision from the operating layer:

- Use-case ROI: Does the project reduce labor, leakage, expedites, safety incidents, inventory exposure, or planning cycle time enough to matter?

- Data readiness: Can the model reach clean, timely, permissioned data without a hidden integration project swallowing the benefit?

- Vendor maturity: Has the product worked in workflows similar to yours, or is it still a demo wrapped around a general model?

- Governance tolerance: Who approves exceptions, who can override the system, and who owns the consequence of a bad recommendation?

- Deployment timeline: Is the use case ready for this planning cycle, or is it better placed in a staged roadmap while infrastructure and tooling mature?

The practical split is straightforward. Continue or expand projects where the operational proof already exists: freight invoice audit, document-heavy procurement workflows, warehouse safety monitoring with human review, demand-planning explanation layers, and Scope 3 data collection are the kinds of bounded use cases that can be evaluated against measurable work. ChainSignal’s guides to supply chain AI ROI from pilot to P&L and what the numbers say about AI ROI in supply chain are better tools for that decision than a semiconductor chart.

Defer or stage projects where the budget case depends mainly on a falling compute-cost story, a vendor’s promise that agents will soon run the workflow end to end, or an executive desire to “do more AI” while the data owners are still unresolved. Nvidia’s FY2026 numbers support confidence that infrastructure investment continues. They do not remove the implementation work sitting inside the supply chain function.

The rule of thumb for Q3 2026 budget reviews is this: Nvidia belongs on the dashboard, not in the approval logic. If Nvidia weakens, ask whether the infrastructure cycle is changing. If Nvidia strengthens, ask whether that improves capacity, pricing, or vendor capability for your specific use case. But approve supply chain AI spend only when the workflow, data, controls, and payback hold up without needing the stock chart to make the argument.

References

- NVIDIA Announces Financial Results for Fiscal 2026 and Fourth Quarter, NVIDIA Newsroom.

- Nvidia’s $40 billion AI investment spree is raising questions on Wall Street, CNBC, May 2026.

- AI infrastructure tracking, Goldman Sachs Insights.

- June 2026 chip stock volatility analysis, Intellectia.ai, June 2026.

- State of AI Survey, NVIDIA Blog.

- Supply chain AI trust survey, RELEX Solutions.

- Gartner Predicts Agentic AI in Supply Chain Management Will Grow From Under $2B in 2025 to $53B by 2030, OpenSky Group, April 2026.

Comments

Join the discussion with an anonymous comment.