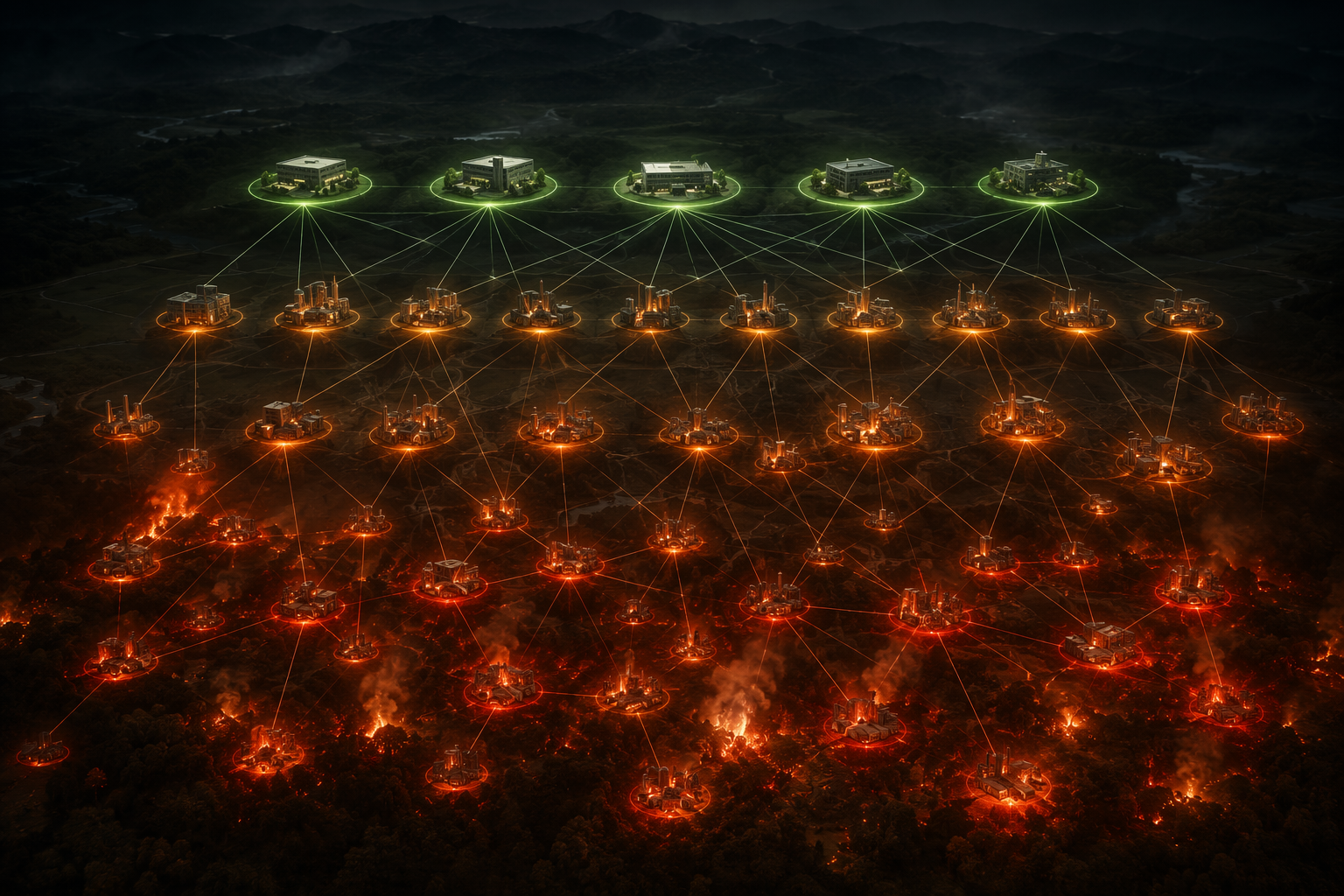

A tier-1 supplier can look clean in a procurement review and still depend on a small upstream facility sitting near a fire corridor, a vulnerable substation, or a road that closes before flames ever reach the plant. That is the uncomfortable starting point for AI wildfire disruption planning: the supplier record says one thing, the physical network says another.

The economic stakes are no longer abstract. The 2018 California wildfires were associated with $88.6 billion in supply chain disruption losses, and one peer-reviewed wildfire-supply-chain modeling paper notes that about 85% of supply chain risks sit in tier 2 through tier 4 suppliers rather than the first tier most companies monitor most closely.[1] That does not mean every sub-tier supplier is dangerous. It means the usual file structure of procurement risk—supplier name, contract owner, category, region, annual spend—does not match the way wildfire disruption travels.

The practical question is narrower than “can AI predict wildfires?” Procurement teams need to know whether probabilistic models can translate wildfire likelihood into supplier-level decisions early enough to matter: where to preposition inventory, which alternate source deserves qualification, which facility needs a continuity review, and which component path has become a single point of failure before fire season begins.

The Blind Spot Is Physical, Not Administrative

Traditional supplier risk reviews tend to stop where direct contractual visibility stops. A tier-1 manufacturer completes a questionnaire, confirms a business continuity plan, and perhaps discloses a few critical sites. The review may flag a high-risk country or a concentration of spend. It often does not map the upstream resin plant, the packaging supplier, the single-source machining subcontractor, the transmission line serving a facility, or the road segment that connects a plant to the next node.

Wildfire disruption does not respect that boundary. A fire can damage a supplier site directly, force evacuation, interrupt power, close a transport route, or reduce labor availability. Smoke and emergency restrictions can matter even when the fire perimeter does not reach the facility. For procurement, the relevant object is not “the supplier” as a legal entity. It is the facility-component-transport path that keeps a bill of materials moving.

That distinction explains why sub-tier mapping matters. If a low-spend tier-3 facility produces a specialized input used by multiple tier-1 suppliers, the spend file will understate its importance. If several approved suppliers depend on the same upstream processor in a fire-prone area, the sourcing matrix may look diversified while the physical network remains concentrated.

This is where AI can be useful, provided the claim is kept within bounds. The strongest current use case is not autonomous procurement or precise seasonal certainty. It is probabilistic exposure mapping: combining hazard, climate, facility, and network data so risk managers can rank where disruption would be both plausible and consequential.

How a Probabilistic Wildfire-Supplier Model Works

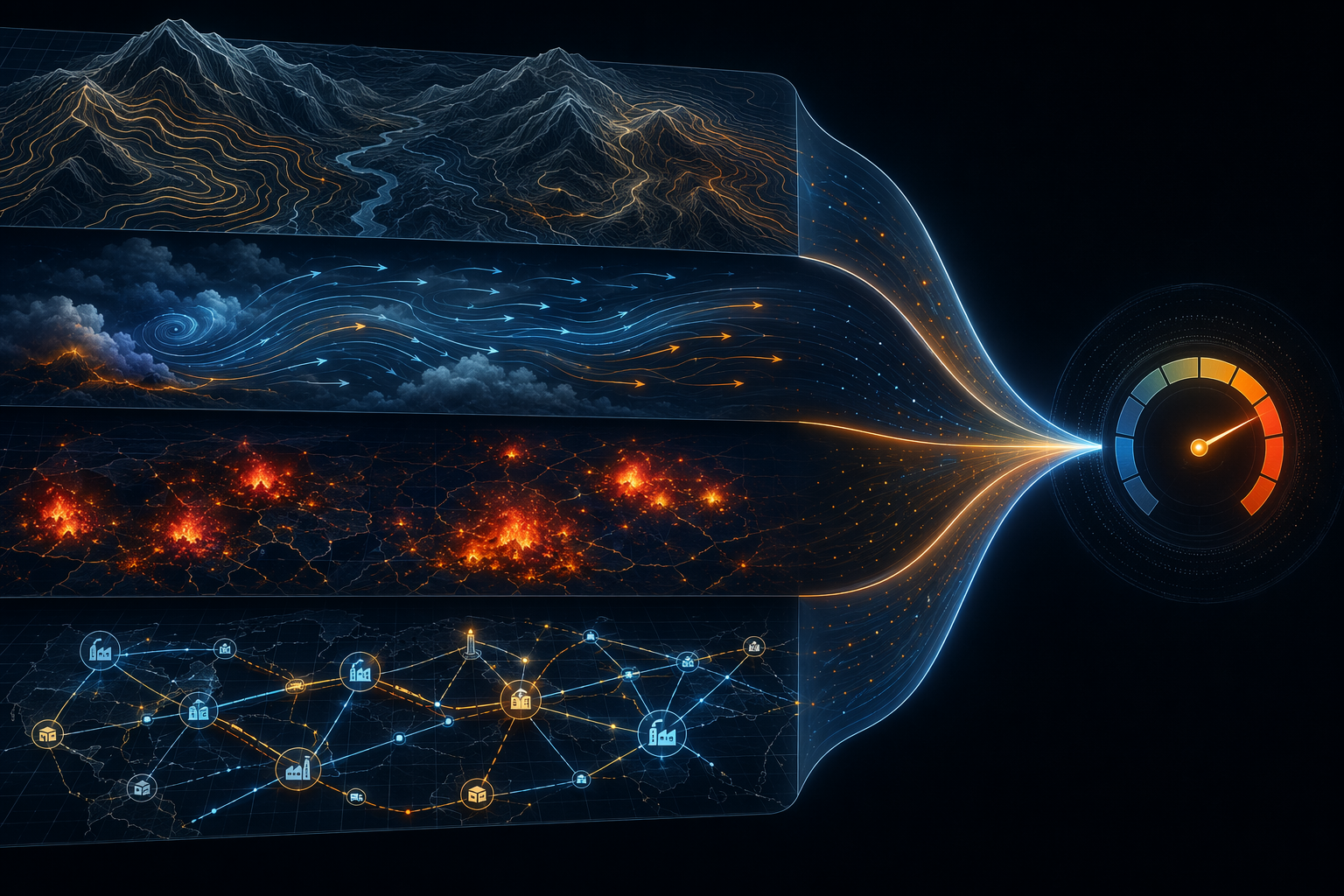

The most useful published framework for this problem is Ma et al. 2022, which models wildfire risk to supply chains by connecting ignition likelihood, fire spread, component vulnerability, and network-level cost impact.[1] Its importance is not that it settles the market. It does not. The framework was validated on a hypothetical sustainable aviation fuel supply chain in the Pacific Northwest, so it should not be treated as a broad benchmark across industries.[1] Its value is methodological: it shows the steps required to move from a regional fire map to a supplier-network consequence.

A basic hazard map can show that a county, province, or industrial zone is fire-prone. That is useful but too blunt for procurement action. The Ma et al. approach asks a more operational chain of questions: how likely is ignition in the relevant area, how might the fire spread, which supply chain components or facilities lie in the affected footprint, how vulnerable are those components, and what cost or service impact would follow if they fail.[1]

| Model layer | What it adds for procurement |

|---|---|

| Ignition likelihood | Separates general wildfire-prone regions from locations with higher modeled probability of fire starting |

| Fire spread modeling | Estimates whether a facility, corridor, or asset could plausibly fall inside an affected area |

| Component or facility vulnerability | Distinguishes exposed nodes from nodes likely to suffer meaningful interruption |

| Network cost impact | Connects a damaged or unavailable node to production, sourcing, and inventory consequences |

The difference between the first and last row is the difference between climate awareness and supply chain planning. A supplier facility may sit in a moderate hazard zone but feed a component with no qualified alternate. Another facility may sit in a severe zone but produce a commodity input with multiple substitutes. The same wildfire probability does not create the same procurement priority.

The model also has to carry uncertainty honestly. Historical fire patterns help, but they are not a stable operating manual. The UNDRR Global Assessment Report 2025 warns about the growing and often invisible costs of wildfire risk, and the limitation here matters: wildfire behavior under climate change is non-stationary, so models trained on past fire regimes may underperform as conditions shift.[2] For a risk team, that is not a reason to ignore the model. It is a reason to ask how often it is recalibrated, which assumptions are stress-tested, and whether the output is presented as a probability range rather than a deterministic answer.

A procurement team can use this kind of model to create a ranked exposure view. The ranking should not simply be “highest fire probability.” It should combine probability with business consequence: sole-source components, long qualification lead times, high revenue products, constrained logistics routes, and facilities that appear in multiple supplier paths. That is where the low-spend tier-3 site can outrank a much larger supplier in the risk review.

What Changes When the Forecast Arrives Six Months Earlier

Seasonal lead time is the operational hinge. A real-time alert during an active fire may help logistics reroute shipments, but it rarely gives sourcing teams enough time to qualify a new supplier, build safety stock, or change a production plan. A six-month signal is different. It sits inside the planning window where procurement, inventory, and operations can still move.

The clearest deployment signal in the available material is Hitachi’s work with ClimateAi. ClimateAi says Hitachi uses six-month seasonal AI forecasts to anticipate climate-related supply chain risks, including cyclone and wildfire seasons, and to preposition inventory before disruption windows arrive.[3] This is still a vendor case study, not an independently benchmarked proof that AI reduces disruption across industries. Its value is more specific: it shows the kind of decision cadence that makes wildfire planning actionable.

With enough lead time, the action set changes. Inventory teams can move stock closer to demand or away from exposed nodes. Procurement can pull forward qualification work for alternates. Operations can decide whether a constrained component deserves a temporary buffer. Finance can see whether the proposed mitigation is proportional to the modeled exposure.

This is also where internal workflow integration matters more than the elegance of the model. A seasonal forecast that stays in a risk dashboard will not change much. It has to reach the people who own allocation, purchasing cadence, supplier qualification, and inventory policy. Teams already working on AI safety stock optimization across multi-echelon inventory networks have a natural place to use these signals, because wildfire exposure becomes one input into where inventory buffers should sit rather than a separate seasonal report.

The same applies to sourcing. A model that identifies repeated wildfire exposure in a component path can support geographic diversification or nearshoring analysis, but it should not automatically trigger a sourcing change. Alternate sourcing has cost, quality, capacity, and qualification consequences. The better use is to put wildfire exposure into the same decision frame as lead time, switching cost, and supplier capability. For teams building that broader location case, AI nearshoring supply chain planning is the adjacent problem.

The Market Is Forming Around Three Capabilities

Vendor coverage numbers can be useful, but they are easy to overread. A platform that covers many businesses is not automatically good at predicting disruption. A platform that tracks many events is not automatically good at mapping sub-tier dependency. The relevant question is what the system can see, how frequently it updates, and whether it connects exposure to the procurement object that needs action.

Interos says its catastrophic risk model covers 94.5 million businesses, which is notable because sub-tier visibility is one of the main gaps in wildfire disruption planning.[4] The number is a scale signal, not a validation result. Buyers still need to know how the platform infers relationships, how it handles private or missing supplier data, and whether a mapped entity corresponds to the facility or component path that matters.

Everstream Analytics reported tracking more than 143 wildfire events in 2023, which points to the event-monitoring side of the category.[5] That capability matters during active incidents, especially when a fire intersects logistics lanes, facility locations, or regional infrastructure. It is a different capability from long-range probabilistic planning, and mature programs will usually need both: seasonal exposure ranking before the season and live monitoring once the season begins.

Sentrisk, a Marsh offering, represents another category entry: geospatial AI and risk advisory applied to supply chain mapping.[6] That matters because large enterprises often buy this capability through risk, insurance, or resilience programs rather than through procurement software alone. The buying path can shape the implementation. If the tool is owned by enterprise risk but not connected to sourcing and inventory workflows, the model may identify exposure without changing decisions.

For readers shortlisting platforms, the practical comparison belongs less in a feature grid and more in architecture questions: supplier graph depth, facility-level resolution, hazard model transparency, update frequency, workflow integration, and evidence from live operating environments. A broader vendor scan can start with the 2026 AI supplier risk monitoring vendor directory, but wildfire planning adds a geospatial and seasonal layer that generic supplier risk tools may not handle well.

Adoption Interest Is Not the Same as Proven Disruption Reduction

There is real buyer pull behind AI in supply chain risk, but it should be read carefully. ABI Research’s 2026 survey found that 65% of respondents said AI or GenAI capabilities are important for technology purchase decisions in supply chain.[7] That is a purchase-intent signal. It does not prove deployment quality, model accuracy, or reduced wildfire disruption.

The same caution applies to market-size narratives. One cited estimate put the wildfire risk AI platform market at $2.8 billion in 2025 with a 14.2% CAGR, but market growth describes commercial activity, not operational effectiveness.[8] This use case sits at the intersection of supply chain risk AI and wildfire analytics, two categories still developing their integration patterns.

Vendor-published ROI claims should stay in the directional bucket unless independently verified. Claims such as stockout reduction and revenue-loss reduction may be useful screening signals, but no peer-reviewed studies were found that benchmark AI wildfire disruption planning tools against traditional methods in live multi-industry environments. That gap is important. It means a buyer can reasonably pilot these systems for decision support, but should not present the output as a validated replacement for continuity planning, supplier development, or human review.

What Makes the Output Usable

The implementation problem is not just model selection. It is whether the organization can turn a probability signal into an accountable planning action. A useful wildfire-risk output tells a team which supplier node, component path, facility, or route deserves attention; why it matters; what confidence level surrounds the estimate; and which decision owner needs to act.

- Sub-tier data coverage: the model must identify meaningful tier-2, tier-3, and tier-4 dependencies, not just enrich known tier-1 records.

- Facility-level resolution: wildfire exposure needs to land on plants, warehouses, transport links, and infrastructure dependencies where possible.

- Model transparency: buyers should understand which inputs drive the score, including historical fire patterns, climate projections, terrain, and vulnerability assumptions.

- Live-environment validation: pilots should compare model alerts with actual disruption, near misses, and operational decisions across at least one fire season.

- Workflow integration: outputs need to feed sourcing review, inventory policy, logistics planning, and executive risk governance rather than remain in a standalone dashboard.

There is a familiar failure mode here: the company buys a sophisticated risk signal, assigns no decision rights around it, and then calls the model disappointing. The problem may be the model. It may also be that no one agreed in advance what level of exposure triggers a supplier review, a safety-stock proposal, a logistics contingency, or an executive exception. That is one reason broader AI supply chain projects fail, and it applies sharply to wildfire planning because the lead time is seasonal and the consequences are cross-functional. Teams pressure-testing their operating model may want to pair this use case with the common failure patterns in why AI in supply chain fails.

A reasonable pilot does not need to cover the whole enterprise. It can start with a product family, a constrained component group, or a region with known wildfire exposure. The pilot should map the supplier graph, identify exposed facilities and routes, rank business impact, define pre-season actions, and review results after the season. If the model flagged a high-risk path and the company took no action, that is a governance finding. If the model missed a material disruption, that is a model and data finding. Both are useful.

Where This Belongs in Procurement Planning

AI wildfire disruption planning belongs in the use-case category, not the magic-forecast category. It is credible enough to inform inventory prepositioning, alternate sourcing review, facility prioritization, logistics contingency planning, and geographic diversification. It is not mature enough to run autonomous procurement triggers or promise precise fire-season outcomes.

The best deployments will probably look less dramatic than the sales language around them. A risk manager brings a ranked list of exposed component paths into the pre-season planning cycle. Procurement checks whether the affected suppliers are truly diversified. Inventory teams decide where a temporary buffer is justified. Operations reviews whether a site or lane needs a contingency. Finance asks whether the mitigation cost fits the exposure. The model supplies a sharper map; people still own the decision.

That is a practical improvement over treating a region as covered because a tier-1 supplier filled out a form. The harder questions remain the right ones: how deep is the supplier graph, how current is the facility data, how does the model handle changing fire regimes, and where does the output enter sourcing and inventory workflows? If a vendor can answer those questions with traceable evidence, AI can make wildfire exposure visible early enough for procurement to do something about it.

References

- Probabilistic wildfire risk assessment for supply chain networks, ScienceDirect, 2022, https://www.sciencedirect.com/science/article/pii/S2212420922005593

- Global Assessment Report 2025, United Nations Office for Disaster Risk Reduction, 2025, https://www.undrr.org/gar/gar2025

- Hitachi Global Supply Chain Risk Model, ClimateAi, https://climate.ai/case-studies/hitachi-global-supply-chain-risk-model/

- Catastrophic Risk, Interos, https://www.interos.ai/

- Everstream Analytics Annual Risk Report, Everstream Analytics, 2023, https://www.everstream.ai/

- Sentrisk, Marsh, https://www.marsh.com/

- Supply Chain Management and Logistics Technology Survey, ABI Research, 2026, https://www.abiresearch.com/

- Wildfire Risk AI Platform Market, https://www.marketresearchfuture.com/

Comments

Join the discussion with an anonymous comment.