The June 2026 semiconductor selloff looked, at first glance, like another demand scare. It was not. The cleaner reading is more physical: investors had been pricing AI accelerator growth as if the next quarter could always be solved with more allocation, and Broadcom’s guidance made that assumption harder to hold. Intellectia estimated that roughly $1.4 trillion in market value was erased across the semiconductor complex in one session, a top-down figure that should be treated as an aggregate market estimate rather than a precise operating measure. NVIDIA alone was estimated to have lost about $300 billion in that session.[1][2]

That is the center of the AI chip supply chain’s stock market impact in 2026: a company can have healthy demand, visible customers, and strong AI exposure, yet still disappoint the market if the factory calendar will not move. Broadcom’s issue, as described in the June selloff coverage, was not a collapse in end-market appetite. It could not raise guidance because TSMC had no additional manufacturing allocation to provide.[1]

The Market Was Repricing a Ceiling

A demand shock changes the numerator. Customers pull back, orders slow, utilization falls, and inventories begin to tell on themselves. A supply ceiling changes the denominator. Customers still want the part, but the supplier cannot turn that demand into shipped revenue quickly enough. The June event belongs much closer to the second category.

The distinction matters because equity markets often compress both stories into the same red screen. In prior semiconductor down-cycles, selloffs were frequently interpreted through the familiar machinery of weak consumer electronics, inventory corrections, or broad macro demand deterioration. This episode had a different trigger. The market did not need proof that AI compute demand had vanished. It needed only to learn that one of the companies feeding that demand could not pull more capacity from the foundry system.

Broadcom’s role in the selloff is important because it made the constraint legible. Investors were not merely reacting to softer language. They were reacting to the implication that upside revenue, at least in the near term, was bounded by another company’s allocation decision. When a supplier’s growth story depends on TSMC capacity that is already spoken for, guidance becomes less a forecast of demand and more a disclosure of physical access.

That is why the reaction spread beyond Broadcom. NVIDIA, AMD, TSMC, memory suppliers, substrate vendors, and equipment names do not all share the same exposure, but they do share the same market narrative: AI growth only becomes revenue when wafers, advanced packaging, HBM, substrates, and test capacity arrive in the right sequence. A missed assumption at one layer forces investors to revisit the whole stack.

Why a Tiny Unit Share Can Move a Trillion-Dollar Sector

The volatility looks less strange once the revenue mix is separated from the unit mix. Deloitte’s 2026 semiconductor outlook estimates that AI chips account for roughly half of semiconductor revenue while representing less than 0.2% of unit volume.[3] That is not a normal product mix. It means a very small number of high-value units can carry a large portion of the sector’s expected growth.

For supply-chain teams, that ratio is the operational explanation for the stock-market violence. If a mature microcontroller program slips, the affected unit count may be large but the value density is lower. If an AI accelerator shipment slips, the lost revenue can be large even when the number of physical devices is small. The bottleneck does not need to touch most semiconductor units to affect most of the market’s growth imagination.

It also explains why small capacity signals receive oversized attention. A few thousand additional advanced-packaging slots, an HBM allocation change, or a foundry utilization comment can alter the expected shipment path for the most valuable chips in the market. Equity analysts may phrase that as multiple compression or guidance risk. Planners hear something more familiar: the allocation book is full.

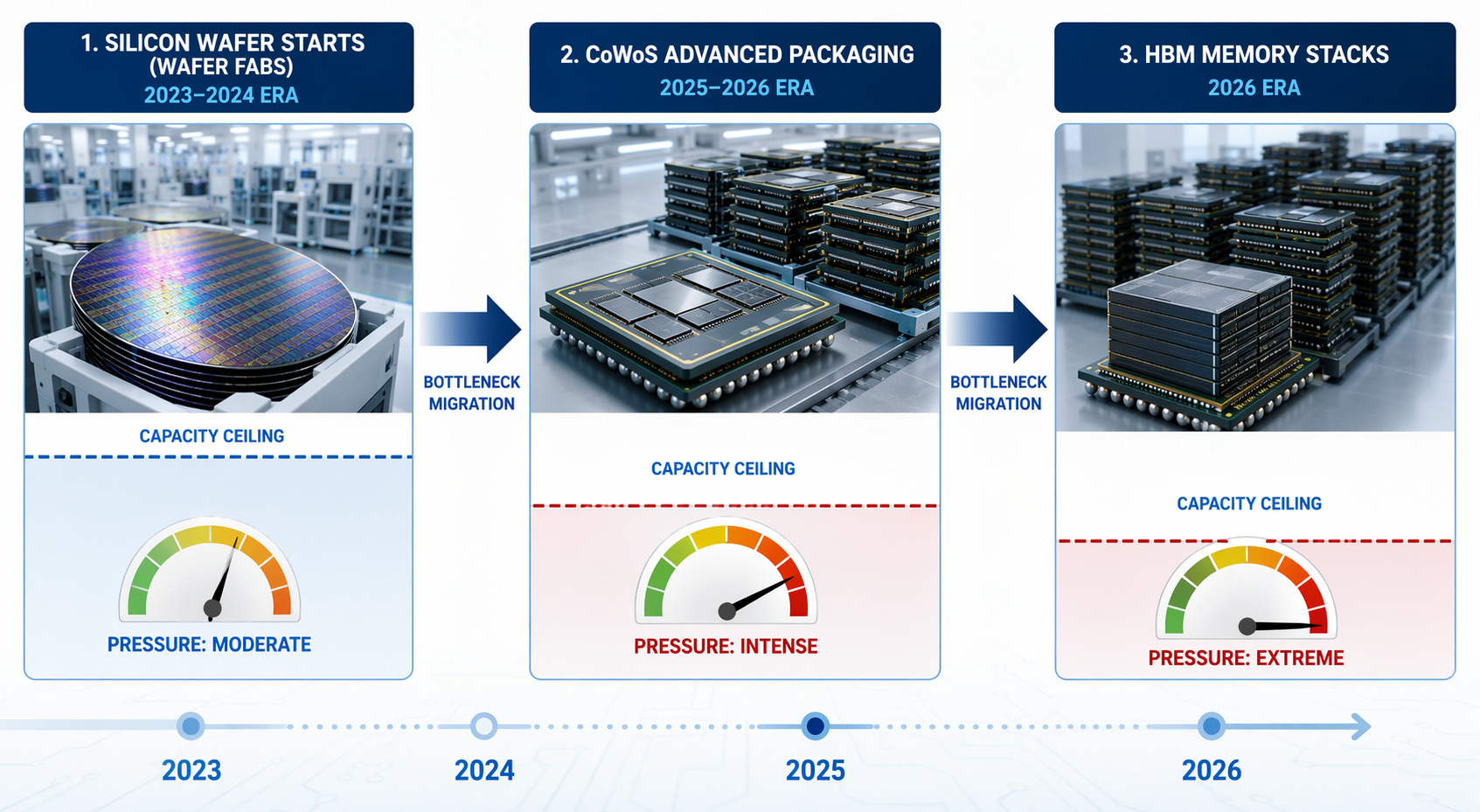

The Bottleneck Has Moved Downstream

The easy version of the AI chip story says there are not enough wafers. That was a useful shorthand earlier in the cycle, but it is no longer precise enough. The binding constraint has migrated. Wafer starts still matter, but for leading AI accelerators the practical ceiling can sit at advanced packaging, especially CoWoS, and at HBM memory availability.

CNAS reports that TSMC’s CoWoS expansion toward roughly 100,000 wafers per month still has not been enough to clear the AI accelerator backlog.[4] That phrasing matters. Expansion is not the same as available supply. A line can be growing, qualified, and heavily committed at the same time. In allocation meetings, the question is not whether the supplier has announced more capacity. It is whether the customer can obtain a dated, usable slot.

CoWoS is where the market’s abstract AI demand becomes a queue. The GPU or custom accelerator die is not the finished product. It has to be integrated with high-bandwidth memory and packaged in a way that can support the bandwidth and power demands of AI workloads. If the foundry can produce the die but the packaging slot is unavailable, the shipment still waits. That is why procurement teams watching lead times often saw the constraint before stock screens did; the delay was sitting between fabrication and finished accelerator supply.

The same dynamic is visible in procurement-level discussions of NVIDIA GPU availability. Persistent lead times above 52 weeks are not only a sign of strong demand; they are a sign that the back end of the supply chain cannot flex instantly when buyers want more compute. A useful companion view is Why Nvidia AI Chip Lead Times Stay Above 52 Weeks, which follows how CoWoS constraints show up as allocation delays rather than as a simple shortage headline.

HBM Is Not a Side Component

HBM has become another ceiling on AI accelerator shipments. Enki’s 2026 supply-chain risk guide reports that HBM memory prices increased by more than 600% in 2025.[5] A price move of that scale does not, by itself, prove shortage in every product lane. It does show that the memory layer is not passive. When HBM is tight, an accelerator vendor can hold the logic roadmap and still lack the memory configuration needed to ship at plan.

This is where many market explanations become too smooth. They treat AI chips as if each vendor controls a single production dial. The actual chain has several dials owned by different companies: foundry wafer capacity, advanced-packaging throughput, HBM supply, substrates, test capacity, power availability at data centers, and the customer’s own deployment schedule. In June, the dial that mattered most was not final customer demand. It was upstream allocation.

Why Broadcom’s Guidance Hit NVIDIA Too

It is tempting to build a clean ticker map: Broadcom says one thing, NVIDIA falls by another amount, memory suppliers move for a third reason. The research base does not support that level of precision. What it does support is a directional mechanism. If the market learns that TSMC cannot increase allocation for one major AI silicon supplier, it has to ask whether other AI growth assumptions are also sitting on constrained foundry and packaging capacity.

That repricing does not require a belief that all companies are equally constrained or equally exposed. It requires only a loss of confidence in the idea that capacity can expand smoothly enough to satisfy every revenue forecast. NVIDIA’s estimated one-session market-cap decline was therefore not necessarily a verdict on its customer demand. It was a mark-to-market adjustment on the scarcity value, timing risk, and capacity dependency embedded in AI compute growth.[2]

The more crowded the AI accelerator queue becomes, the more one supplier’s allocation comment can become everyone’s signal. A procurement manager would recognize the pattern immediately: if a constrained factory tells one large customer there is no upside, every other large customer starts rechecking promises.

Capital Spending Is Context, Not Relief

There is plenty of announced investment around AI infrastructure and semiconductor capacity. Enki cites multi-year commitments including $500 billion from NVIDIA, $165 billion from TSMC, and $100 billion from Intel.[5] Those figures help explain why investors still see a long runway for the sector. They do not prove that relief is available in the quarter when guidance is being set.

A fab announcement has to become a completed shell, then installed tools, qualified process capacity, yield, customer qualification, packaging access, and logistics flow. Advanced packaging expansions have their own tool, substrate, qualification, and staffing constraints. HBM capacity has memory-fab and stacking dependencies. The gap between announced capital and shippable AI accelerators is exactly where market risk now lives.

Reshoring and policy support belong in the same category. They matter, especially for long-term geographic resilience and geopolitical exposure, but they should not be read as a near-term allocation guarantee. Supply-chain intelligence teams should track policy risk and industrial capacity together; treating either one as a standalone answer is how organizations miss the actual constraint. For a broader monitoring approach, AI as a Geopolitical Early Warning System for Supply Chains is a useful extension.

The Signals Worth Watching Now

The lesson from June is not that every supply-chain constraint becomes an immediate stock-market event. It is that the right constraint, attached to the highest-value part of the semiconductor mix, can move markets before a conventional demand indicator turns. The useful monitoring framework is therefore operational, dated, and specific.

| Signal | What it actually measures | Why it matters for market risk |

|---|---|---|

| TSMC capacity utilization and allocation commentary | Whether leading-edge manufacturing slots are already committed | Guidance upside can disappear if foundry allocation is unavailable |

| CoWoS monthly output | Advanced-packaging throughput for high-end AI accelerators | Wafer supply may not convert into finished accelerator shipments without packaging capacity |

| HBM forward orders and spot pricing | Memory availability and pricing pressure for AI accelerator builds | Tight HBM can cap shipments even when logic die are available |

| Fab and packaging construction timelines | When announced capacity might become qualified, usable supply | Markets often price planned expansion before it can relieve allocation |

| Hyperscaler Capex guidance revisions | Whether the largest AI infrastructure buyers are still funding deployments | This separates genuine demand softening from supplier-side shipment ceilings |

The last item is important because demand should not be dismissed. If hyperscalers cut Capex guidance, defer data-center builds, or slow deployment schedules, the interpretation changes. June’s catalyst was supply-side, but that does not make demand irrelevant. It means demand was not the fact that broke the market’s assumption in that session.

The same discipline applies outside chip tickers. Physical infrastructure constraints can erase market value when investors have priced growth without checking power, water, land, GPU availability, or deployment pacing. The SpaceX Stock Slump Reveals AI Infrastructure Supply Chain Risks case is a parallel reminder that AI infrastructure risk is not confined to silicon.

What the June Selloff Really Changed

The selloff did not prove that AI demand is fragile. It proved that the market had been treating constrained supply as if it were flexible supply. Once Broadcom could not raise guidance because TSMC allocation was unavailable, the equity story had to absorb a planner’s reality: demand that cannot be built, packaged, and shipped on time is not near-term revenue.

That makes 2026 semiconductor equity risk increasingly a supply-chain risk surface. The most useful early warnings are not broad declarations about AI enthusiasm or generic cycle timing. They are dated signals from the bottleneck stack: foundry allocation, CoWoS throughput, HBM availability, construction slippage, and hyperscaler spending discipline. The people already watching those constraints may understand the next market shock before the market decides what to call it.

Comments

Join the discussion with an anonymous comment.