On one front, AI-assisted drones are reaching supply vehicles more than 100 km behind the line. On another, drones and sea drones have helped push commercial carriers away from the Red Sea and Suez Canal. Those are not separate defense stories. For supply chain leaders, they are two sides of the same operating problem: logistics assets are becoming reachable, and logistics routes are becoming repriced.

That is the practical meaning of AI drone attacks as supply chain disruption. The issue is not whether drones are novel or dramatic. The issue is whether a threat can change routing, lead time, safety stock, supplier qualification, insurance cost, and executive escalation thresholds. On the evidence now available, it can.

The logistics target is moving farther from the front

BBC Verify reported in May 2026 that Ukraine’s Hornet system used AI trained on four years of combat footage and had destroyed more than 150 Russian supply vehicles, with an operational reach more than 100 km beyond the front line.[1] That report matters because it does not just describe a better weapon. It describes a change in what counts as a protected logistics zone.

A supply truck, fuel convoy, maintenance vehicle, or ammunition movement that sits outside artillery range has traditionally been treated differently from one moving close to contact. That distinction does not disappear, but it weakens when AI-assisted targeting helps a system identify and pursue logistics assets farther back. The planning consequence is plain: rear-area movement can no longer be assumed to be low-friction just because it is not near the visible line of fighting.

The Hornet case should be handled carefully. BBC Verify is the strongest named source in the available material, with expert attribution from Clément Molin of Atum Mundi, Robert Tollast of RUSI, and Nick Brown of Janes.[1] Independent second-source verification is still limited. That narrows the claim: the case is not proof that every conflict will immediately produce the same effect. It is evidence that autonomous or AI-assisted targeting is already being applied to logistics vehicles at distances that should make planners revise their assumptions about where disruption can begin.

For commercial supply chains, the military setting is not a reason to ignore it. Military logistics often shows what happens when attackers prioritize fuel, repair, transport, and replenishment rather than only high-profile assets. If the tactic matures, the civilian analogue is not a drone hovering over a warehouse in every market. It is a higher likelihood that transport nodes, border corridors, ports, energy terminals, and fleet support infrastructure become part of the target set in regions where conflict risk already exists.

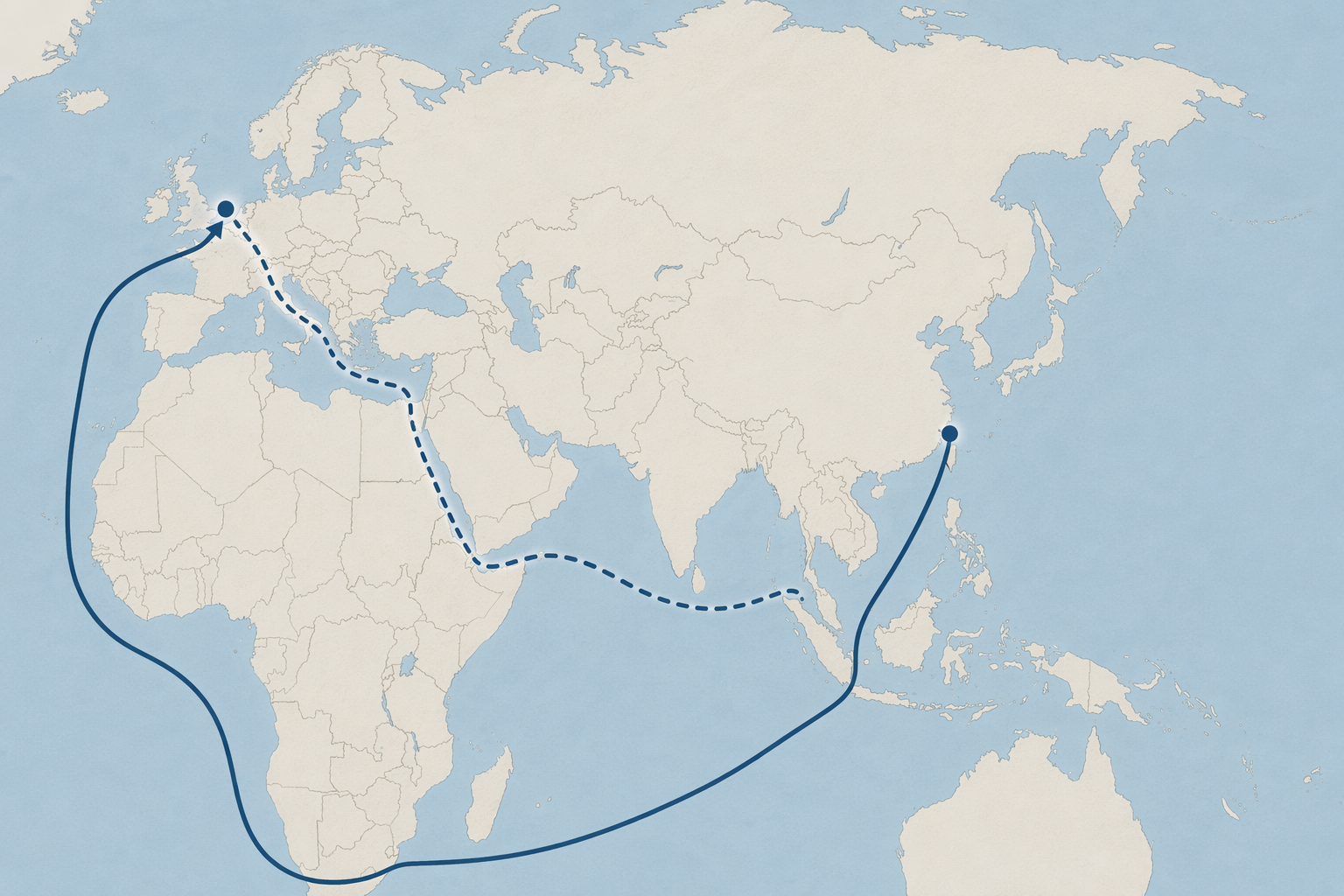

The chokepoint problem is already in the freight math

The Red Sea shows the commercial side of the problem more clearly than any abstract scenario. Since November 2023, more than 100 vessels have been targeted in the Houthi campaign, according to Sentrycs’ account of drone threats to commercial vessels.[2] The more important supply chain number, though, is not the attack count. It is what carriers, insurers, and shippers did after the route stopped behaving like a normal chokepoint.

Project44 reported a 72% decline in Suez container traffic during the Red Sea crisis, a 9% reduction in global container capacity, 5-7% of the global container fleet tied up in Cape of Good Hope routing, 25-40% Asia-Europe freight rate increases, and 10-14 additional transit days.[3] Those figures translate the security event into planning variables: fewer effective ships, longer cash cycles, later inventory arrivals, higher spot exposure, and more buffers that have to be defended in budget meetings.

The Cape diversion is sometimes described as a reroute, as if the system simply chooses a different line on a map. That undersells the effect. A longer route absorbs vessels that would otherwise be available elsewhere. It stretches sailing schedules, equipment cycles, container availability, port calls, and inland appointment windows. A procurement director may experience the same event as a supplier lead-time change; a freight buyer may experience it as a premium; a finance team may experience it as working capital trapped on the water.

The timeline is fluid. The July 2025 sinkings followed a ceasefire collapse, and 2026 reporting describes a persistent but variable threat environment rather than a constant level of attacks.[4] That distinction matters. A quiet month does not automatically restore the old baseline if carriers and insurers still price the corridor as unstable. Conversely, estimates that Cape routing may remain a default through at least 2027 should be treated as consensus planning assumptions, not certainty.[4]

What changes inside the risk framework

The standard geopolitical disruption playbook can still do useful work. It can flag countries, sanctions exposure, port closures, civil unrest, and conflict escalation. It can trigger alternate sourcing reviews and logistics exception management. What it often misses is the mechanics of a drone-enabled disruption vector: the threat is mobile, comparatively low-cost, difficult to attribute quickly, and able to affect logistics without occupying territory or closing a port by formal order.

| Planning variable | How AI-enabled drone risk changes the assumption |

|---|---|

| Routing | A lane may remain technically open while carriers treat it as commercially unattractive or operationally unsafe. |

| Lead time | Transit buffers must account for diversion, convoying, port schedule disruption, and delayed insurance or carrier decisions. |

| Capacity | Longer routes remove effective vessel capacity from the wider network, even for shippers not sailing through the attacked corridor. |

| Inventory | Safety stock arguments shift from temporary exception to structural policy for exposed SKUs and suppliers. |

| Insurance | War-risk premiums become a forward signal, not just a post-event cost line. |

| Escalation | Executive review should trigger before an attack closes a route, when carriers and insurers begin changing behavior. |

The insurance signal deserves more attention than it usually gets. Swiss Re’s SONAR 2025 analysis described new risks from drone technology and noted Red Sea transit war-risk insurance at 0.5-1.0% of cargo value, while Strait of Hormuz hull coverage was around 5% of vessel value.[5] Those percentages are not just insurance trivia. They are market prices for perceived exposure, and they often move before a procurement dashboard has a clean disruption label to apply.

When insurance reprices, several decisions follow. Carriers may alter service strings. Forwarders may narrow routing options. Shippers may face surcharges that are easier to approve after a headline event than before one. Finance teams may challenge higher inventory levels unless the risk team can show that the baseline route is no longer the baseline route in commercial terms.

Direct targeting and chokepoint disruption now reinforce each other

A direct logistics-targeting case and a maritime chokepoint case create a stronger conclusion together than either does alone. The Hornet reporting shows logistics vehicles being identified and hit far behind the front.[1] The Red Sea data shows commercial shipping changing behavior at scale after drone and sea-drone threats made a corridor too costly or unsafe for normal operations.[2][3]

That convergence is the structural risk. A company does not need its own vessel to be attacked to feel the effect. It can be hit through carrier capacity, supplier shipment timing, war-risk premiums, port congestion, or a buyer’s inability to get a component to the right factory window. The disruption propagates through the network before it appears as a stockout.

The Black Sea offers reinforcing evidence that unmanned maritime systems are not confined to one theater. Ukrainian naval drones have been reported striking more than 20 Russian vessels and hitting oil-related infrastructure around Novorossiysk.[6][7] That does not mean every energy export terminal or commercial port faces the same threat. It does mean the operating model is no longer theoretical: remotely operated or autonomous systems can put maritime assets and coastal infrastructure into the risk set without requiring a traditional naval engagement.

The old playbook handles shocks better than structural drift

Most companies know how to respond to a discrete disruption. A port closes. A supplier fails. A vessel is delayed. A route is suspended. The event receives a severity rating, teams open a response channel, and the organization waits for the disruption to clear.

AI-enabled drone risk is harder because it can change the default without producing a single clean start date. Carriers may quietly keep vessels away from a corridor. Insurers may widen exclusions or raise premiums. Suppliers may pad shipment windows. Forwarders may stop guaranteeing the same transit time. By the time an executive asks whether the disruption is over, the network may already have learned to operate on a more expensive assumption.

That is why treating this only as a geopolitical risk bucket is too blunt. The category needs its own monitoring logic tied to assets and decisions, not only to countries and headlines. The relevant question is not “Is the region tense?” It is “Which routes, suppliers, ports, vessels, terminals, inventories, and insurance terms change if drone activity increases or if carriers believe it might?”

- Route exposure: lanes that depend on the Red Sea, Strait of Hormuz, Black Sea, or other corridors where drone or sea-drone activity can alter carrier behavior.

- Supplier exposure: vendors whose lead times depend on at-risk ports, inland corridors, fuel movements, or export terminals.

- Capacity exposure: SKUs and business units sensitive to vessel absorption, blank sailings, container shortages, or service-string changes.

- Insurance exposure: lanes where war-risk pricing, exclusions, or hull and cargo coverage changes can make a technically available route uneconomic.

- Decision exposure: thresholds for moving from observation to alternate routing, safety stock release, expedited freight, or executive approval.

What deserves monitoring now

A useful monitoring framework should not wait for a vessel attack to become a global headline. It should track the signals that change commercial behavior: carrier advisories, AIS route shifts, insurance premium movement, port and terminal alerts, militia or military claims, ceasefire status, naval warnings, forwarder service updates, and supplier shipment exceptions. The output should be a planning decision, not a threat digest.

For a lane exposed to the Red Sea, that may mean maintaining two lead-time assumptions: one for a Suez routing environment and one for Cape routing. For a supplier tied to a conflict-adjacent logistics corridor, it may mean reviewing whether safety stock sits too close to the same transport risk that could interrupt replenishment. For a category manager with critical inputs from one region, it may mean qualifying a second route before the premium appears in the next freight quote.

The point is not to overreact to every drone report. The point is to stop treating drone activity as background noise until it becomes an emergency. The material indicators are the ones that move a plan: longer transit windows, reduced effective capacity, changed carrier acceptance, higher war-risk cost, supplier delivery variance, and repeated attacks on logistics rather than symbolic targets.

A dedicated structural risk category

AI-enabled drone attacks now deserve a dedicated structural risk category inside supply chain risk frameworks. The category should sit beside, not inside, generic geopolitical disruption. Its monitoring should be tied to routes, suppliers, ports, insurance signals, and lead-time assumptions, because those are the places where the risk becomes operational.

The next operational question is detection: how to connect drone-threat indicators to shipment, supplier, and lane decisions early enough to act. ChainSignal’s related use case, How AI Risk Monitoring Detects Drone Threats to Supply Chains, carries that question forward from structural assessment into monitoring practice.

References

- Ukraine’s AI drones are hunting Russian supply trucks 100km from the front line, BBC, May 2026.

- Navigating Troubled Waters: The Escalating Drone Threats to Commercial Vessels, Sentrycs.

- The Red Sea Crisis: A Year of Houthi Attacks & Their Impact on Global Shipping, project44.

- Red Sea Shipping Crisis 2026, Suaid Global.

- New risks from drone technology, Swiss Re.

- Ukrainian drone attack on Russian oil terminal exports shows Black Sea long-range strike capabilities, Fortune, May 23, 2026.

- Ukraine’s naval drones are changing the war in the Black Sea, CBC.

Comments

Join the discussion with an anonymous comment.