The cleanest way to misread the Nvidia AI chip supply chain in Q3 2026 is to start with the fab expansion headline and stop there. TSMC can expand CoWoS capacity, Nvidia can reserve more supply, and memory vendors can talk about new HBM ramps, yet an enterprise buyer can still be told that usable accelerator capacity arrives next year, or later. That is not a contradiction in the supply chain. It is the supply chain.

The public signal says capacity is expanding. The procurement signal says the booking window has not cleared. Silicon Analysts estimates that TSMC is moving monthly CoWoS capacity toward 120,000 to 130,000 wafers per month by the end of 2026, while also estimating that more than 85% of 2026–2027 capacity is already pre-booked and that Nvidia holds roughly 60% of that capacity, or about 595,000 wafers.[1] Those figures should be treated as directional allocation signals rather than audited customer-by-customer truth. But directionally, they explain why a new buyer can hear “capacity is up” and still have no near-term place in line.

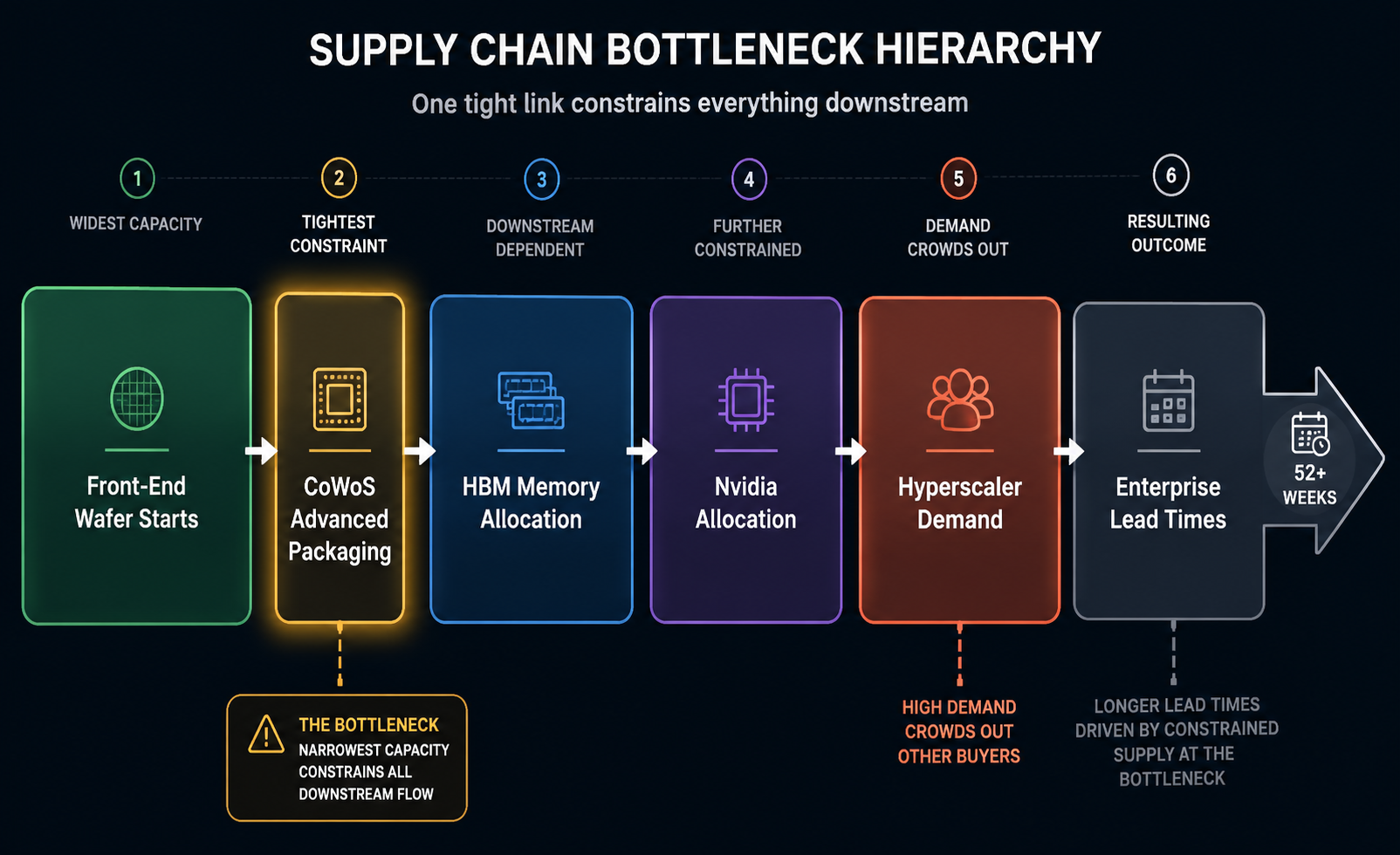

The Constraint Is After the Wafer

A front-end wafer start is not the same thing as a deployable AI accelerator. For an H100-class or Blackwell-class system to reach a customer, the chip must pass through advanced packaging, attach to high-bandwidth memory, land inside a board and system allocation, and then compete with hyperscaler demand before an enterprise delivery date becomes real.

That distinction matters because CoWoS is not generic backend capacity. It is the packaging step that lets large AI accelerators and HBM stacks sit close enough together to deliver the memory bandwidth modern training and inference workloads need. More front-end wafer starts help only if the downstream packaging and memory are available at the same time. A buyer who secures silicon without securing CoWoS and HBM has not secured capacity; they have secured one input into a queue.

| Layer | What It Controls | Procurement Signal |

|---|---|---|

| Front-end wafer starts | Initial silicon production | Useful only when downstream packaging and memory are already aligned |

| CoWoS advanced packaging | Integration of accelerator die with HBM | Booking window and pre-booked allocation |

| HBM memory | Bandwidth required for AI accelerators | Supplier allocation by generation, especially HBM3E and HBM4 |

| Nvidia allocation | Which OEMs, clouds, and customers receive finished accelerator supply | Confirmed delivery position, not verbal demand registration |

| Hyperscaler demand | Crowding pressure on available supply | Reserved capacity and capex commitments |

| Enterprise lead time | When usable compute actually arrives | Hardware delivery date plus facility readiness |

This is why lead-time numbers are evidence of the bottleneck structure, not just a complaint about scarcity. Spheron describes H100-class hardware lead times in the 36–52 week range, while Vamsi Talks Tech describes Blackwell B200 allocation as extending into the second half of 2027 for new entrants.[2][3] The important word is “new.” Buyers already inside the allocation stack are having a different year from buyers trying to enter it now.

CoWoS and HBM Bind Together

CoWoS gets most of the bottleneck attention because it is visibly narrow. HBM is just as unforgiving because it is not a late accessory that can be swapped in after the accelerator is built. The memory allocation has to be committed alongside the package plan. If the HBM is missing, the package slot is not enough. If the package slot is missing, the HBM does not turn into a finished Nvidia system.

Enki AI describes HBM3E as sold out for 2026 with double-digit year-over-year price increases, and says SK Hynix, with roughly 62% share, supplies about two-thirds of Nvidia’s allocation.[4] Astute Group adds the structural reason this is not a normal memory tightness story: producing a gigabyte of HBM takes 3–4 times as many wafers as DDR5.[5] That makes the AI memory shift a drain on wafer capacity inside the memory industry itself, not just a matter of moving finished modules from one customer to another.

For procurement, the practical consequence is harsh but clarifying. A supplier update that says wafer capacity is available does not answer the question. The question is whether the required HBM generation is allocated, whether that HBM is matched to a CoWoS window, and whether the finished Nvidia system has a confirmed place in the customer allocation sequence.

Hyperscaler Demand Turns Tightness Into Queue Position

The shortage is not only a technical packaging problem. It is also a purchasing-power problem. Silicon Analysts reports combined hyperscaler capex of about $434 billion over the trailing four quarters, projected at about $700 billion for calendar 2026, with roughly 75% targeting AI infrastructure directly.[6] Tom’s Hardware reports that four customers represent 61% of Nvidia’s revenue, a concentration that helps explain why ordinary enterprise buyers do not experience the market as an open catalog.[7]

Those numbers do not prove that every enterprise delay is caused by hyperscalers. They do show the shape of the crowding. When the largest buyers reserve supply early, commit across multiple years, and absorb systems as fast as vendors can package them, later buyers are not merely waiting for manufacturing capacity. They are waiting for allocation capacity.

That is the part that gets lost in cheerful quarterly supplier reviews. “Capacity is expanding” can be true at the same time that the next available enterprise delivery slot moves right. The buyer’s problem is not whether the industry will be larger in the abstract. It is whether their program has a claim on the constrained steps that convert industry capacity into a rack they can power, cool, and use.

The Booking Window Is the Better Signal

A capacity number tells you how much a process may be able to produce at a point in time. A booking window tells you when the next buyer can enter that process. For AI accelerators in 2026, the second number is more useful to an enterprise planner than the first.

Silicon Analysts argues that the leading indicator for AI supply relief is not instantaneous wafers per month, but the lead time over time for CoWoS and HBM; as long as CoWoS lead times remain above 52 weeks, expansion headlines are weak near-term supply signals.[8] That is a narrower claim than saying the booking window perfectly predicts delivery. It does not. A booked package slot can still be affected by yield, memory availability, system integration, export rules, customer priority, or facility readiness. But if the booking window is still stretching beyond a year, the buyer should not treat a capacity expansion headline as usable relief.

This is also where precision should make people more skeptical, not less. Estimates such as Nvidia holding roughly 60% of CoWoS capacity or more than 85% of 2026–2027 CoWoS being pre-booked are useful because they reveal the allocation direction.[1] They are less useful if treated as clean, auditable per-customer apportionment. A procurement team does not need false certainty. It needs enough signal to stop planning around the wrong bottleneck.

What Procurement Should Change

The response is not to panic-buy every GPU quote that appears. It is to make the sourcing process match the actual constraint map. Vamsi Talks Tech lays out four procurement moves: secure CoWoS in parallel with wafer slots, lock HBM before committing front-end starts, track the booking window rather than capacity headlines, and start facility assessment at the same time as hardware orders.[3] Each one protects against a different failure mode.

Secure CoWoS in Parallel With Wafer Slots

A wafer commitment without a packaging path is an incomplete supply plan. Procurement should ask suppliers to identify the packaging allocation attached to the proposed accelerator delivery, not just the chip family, OEM, or expected production quarter. If the answer is that packaging will be arranged later, the buyer is being asked to accept the most important uncertainty after the commercial commitment.

The better question is concrete: which CoWoS window supports this delivery date, and what customer priority does that window carry if higher-volume buyers pull forward demand? A supplier may not disclose the full chain, but the quality of the answer usually tells a procurement team whether the date is allocation-backed or forecast-backed.

Lock HBM Before Treating the Accelerator Plan as Real

HBM should be treated as a gating item, not a bill-of-material line that appears after sourcing has already selected the accelerator. The procurement file should specify the HBM generation, the supplier exposure where available, the allocation status, and the consequence if the memory generation changes. That last point matters because “available memory” and “qualified memory for the intended accelerator platform” are not the same thing.

For buyers trying to reserve Blackwell-class systems, this also means checking whether the delivery date is tied to HBM3E availability, an HBM4 transition plan, or a supplier-specific qualification path. The research supports caution here rather than a broad claim: HBM pricing and lead-time figures vary by supplier and generation, so procurement should not apply a single memory assumption across all Nvidia platforms.

Track the Booking Window, Not the Press Release

The operating metric should be simple enough to survive an executive review: how many weeks from order commitment to usable capacity, and is that number compressing over successive checks? If CoWoS and HBM booking windows stay above a year, the planning assumption should remain constrained even if annual capacity targets rise.

- Ask suppliers for lead-time movement over time, not only current quoted delivery.

- Separate wafer availability, CoWoS availability, HBM allocation, and finished-system allocation in the sourcing tracker.

- Flag any quote where the delivery date depends on “expected capacity additions” without a named allocation path.

- Treat new-entrant Blackwell timing differently from incumbent hyperscaler or cloud-reserved capacity.

Start Facility Readiness While the Hardware Is Still in Queue

Long hardware lead times create a bad habit: teams wait for firmer delivery before checking power, cooling, floor load, cage readiness, network changes, and operations staffing. That sequence turns a supply-chain delay into a deployment delay. If the accelerator delivery slips, the facility work may feel premature. If it does not slip, a late power or cooling finding can waste the scarce allocation the buyer fought to obtain.

This is where infrastructure planning and procurement have to sit in the same room earlier than usual. The hardware order is no longer the start of the deployment clock. The packaging and memory queue started earlier, often before the enterprise buyer had a signed internal business case. Facility readiness has to catch up while the supply queue is still moving.

The Enterprise Buyer’s Near-Term Reality

None of this argues that TSMC capacity additions are meaningless, or that Nvidia’s supply-chain execution is weak. The opposite is closer to the truth: the technical stack is expanding under extraordinary demand. But procurement teams do not buy long-run industry direction. They buy a delivery position for a model rollout, a data center cage, a cloud-reserved-capacity plan, or a budget year that closes whether the accelerator arrives or not.

The same concentration that makes Taiwan foundry execution strategically important also makes disruptions hard to absorb. ChainSignal has covered how AI can help supply chains plan around earthquake risk in Taiwan through AI supply chain planning for earthquake risk. In the Nvidia accelerator chain, resilience planning has to include not only front-end continuity, but also packaging concentration, HBM qualification, and allocation priority.

In Q3 2026, the practical conclusion is narrower and more useful than a shortage forecast. A buyer planning AI compute should treat CoWoS and HBM booking windows as the real supply signal, and treat capacity expansion headlines as background context until lead times actually compress. If the booking window still says 52-plus weeks, the queue has not cleared just because the factory slide got more optimistic.

References

- Why CoWoS Lead Times — Not Wafer Capacity — Are the Real AI Bottleneck, Silicon Analysts

- GPU Shortage 2026, Spheron

- The GPU Supply Chain Crisis, Vamsi Talks Tech

- AI Chip Supply Chain Risk 2026, Enki AI

- Semiconductor supply chains under strain, Astute Group

- The Hyperscaler Capex Wall, Silicon Analysts

- A deeper look at the tightened chipmaking supply chain, Tom's Hardware

- Foundry Allocation Status 2026, Silicon Analysts

Comments

Join the discussion with an anonymous comment.