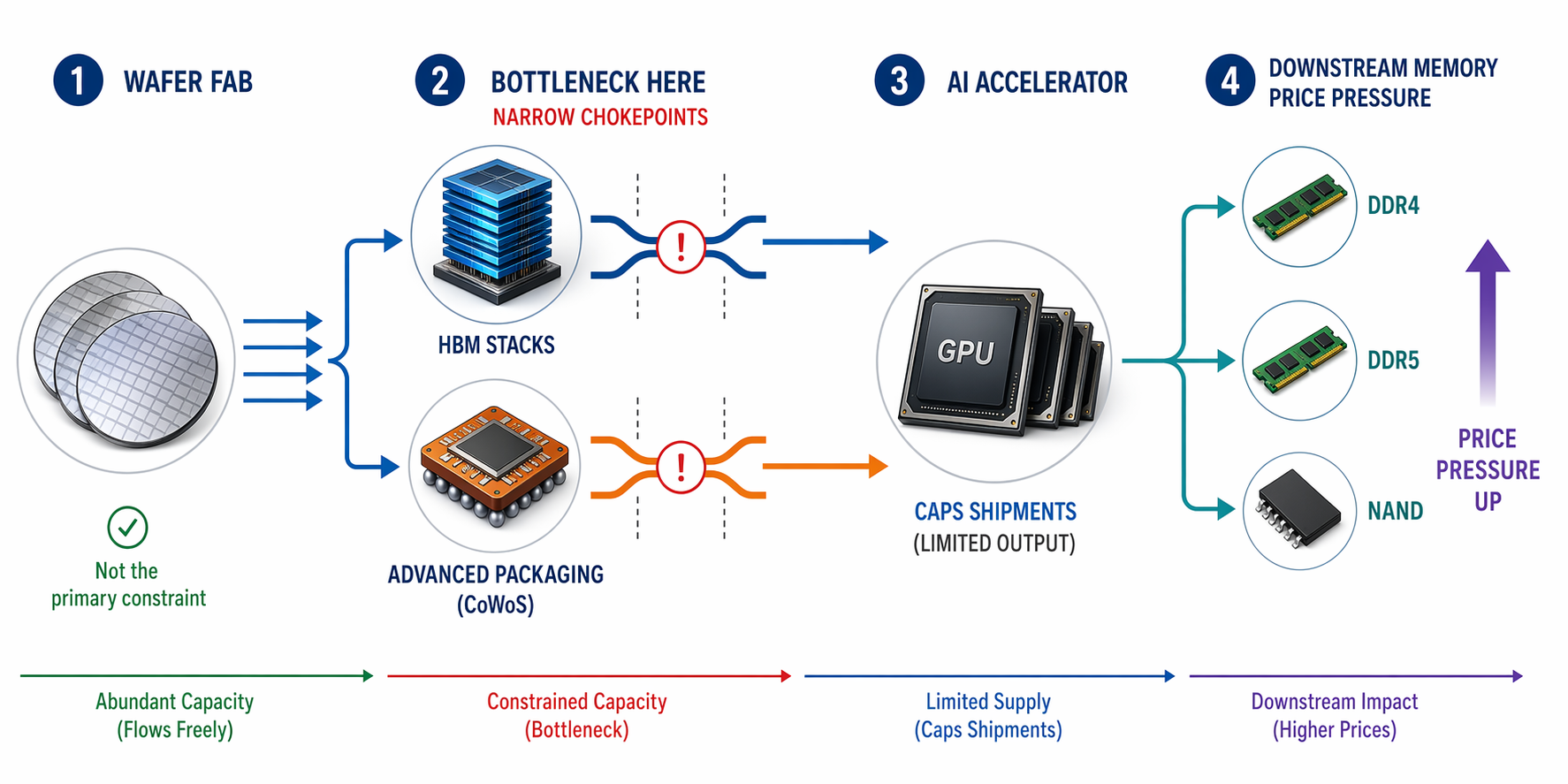

A useful 2026 semiconductor supply chain AI chip outlook starts with a correction: more front-end wafer capacity does not automatically mean more AI accelerators. Wafers still matter, but they are no longer the clean diagnostic for why the most sought-after AI chips are late, allocated, or expensive. The tighter question is whether enough high-bandwidth memory can be stacked close enough to the logic die, and whether enough advanced packaging capacity exists to put the whole assembly together at acceptable yield.

That distinction is not academic. TSMC had already identified advanced packaging, rather than wafer production alone, as the industry's primary bottleneck by 2025, and Deloitte's 2026 semiconductor outlook treats that constraint as still active in the current cycle.[1] Market reports also describe HBM supply as effectively sold out through 2026 to major AI vendors, with Samsung, SK Hynix, and Micron controlling nearly all of a structurally undersupplied market.[2][3]

The Constraint Has Moved Behind the Fab Gate

The old shortage story was easier to track. If the fab was full, the queue lengthened. If wafer starts increased, relief eventually appeared. AI accelerators complicate that model because the logic die is only one part of the shipment. A modern accelerator needs HBM stacks placed very close to the compute die, usually through advanced packaging flows such as CoWoS-class integration or other 2.5D and 3D approaches. If either the memory stack or the packaging slot is missing, the finished accelerator does not ship.

That is why wafer capacity can look healthier than the actual delivery picture. A foundry can process more leading-edge wafers and still leave customers waiting if the back-end integration queue cannot absorb the output. Procurement teams that only watch foundry expansion announcements are looking at the wrong mile marker. The more relevant signal is where the assembled module stops moving.

HBM and advanced packaging also reinforce each other as constraints. HBM is not a generic memory part that can be substituted late in a build. It is stacked, tested, and qualified for tight electrical and thermal requirements, then integrated close to the processor through packaging steps that are themselves capacity-limited. A shortage in one layer strands capacity in the other. Extra logic wafers do not solve that; they can simply create more inventory waiting for memory or packaging.

Why Advanced Packaging Is So Slow to Expand

Advanced packaging is often described as capacity, but it behaves less like a simple square-footage problem and more like a controlled industrial choreography. CoWoS-class flows involve interposers, multiple large dies, HBM stacks, substrate constraints, inspection steps, thermal considerations, and yield management across a much more complex assembly than a conventional package. Each added interface gives buyers another place where output can be delayed.

Deloitte cites TSMC's CoWoS capacity target at about 100,000 wafers per month, which is a large number in packaging terms but still has to be measured against the scale of accelerator demand from the biggest AI buyers.[1] The same outlook points to back-end engineering talent as part of the problem, not just tools or factory space.[1] That matters because packaging expansion requires process know-how, failure analysis, supplier coordination, and production discipline; it is not a capacity lever that flips as quickly as a purchase order.

This is where elegant AI chip narratives often skip a floor. The accelerator may be designed around extraordinary compute density, but the shipment is gated by mundane execution: qualified memory supply, packaging line availability, test capacity, rework limits, and people who understand how to stabilize a difficult back-end process. The fab is visible because it is capital intensive. The package is decisive because it is where the accelerator becomes a deliverable product.

HBM Allocation Does Not Stay Inside the AI Market

The HBM squeeze would be easier to contain if it only affected hyperscalers and accelerator vendors. It does not. HBM uses DRAM capacity, supplier attention, test resources, and capital allocation that memory makers cannot simultaneously devote to ordinary DDR4, DDR5, LPDDR, NAND, NOR flash, and embedded memory categories. The exact internal allocation decisions vary by supplier and contract, but the direction of incentive is clear: when AI buyers are willing to reserve scarce HBM output, memory makers prioritize the highest-value queue.

That is the cannibalization mechanism procurement teams should care about. A factory planner building industrial controls may never buy an HBM stack. An automotive electronics team may not have a single AI accelerator on its bill of materials. Yet both can still face higher DRAM quotes, longer lead times, or unexpected redesign pressure because the memory supplier's best capacity and management attention have been pulled toward AI infrastructure.

The pricing data fit that mechanism. Forbes, citing Gartner's April 2026 forecast, reported that DRAM prices rose by about four times between September and November 2025 and that Gartner expected DRAM prices to increase 125% and NAND prices 234% in 2026.[4] Because the Gartner figures are being referenced here through the Forbes report rather than a directly verified primary release, they should be treated as a cited market forecast, not as an independently revalidated dataset.

Supplyframe's Commodity IQ points in the same direction from the buyer's side: as of Q2 2026, its memory demand index was up 70% quarter over quarter, lead times were up 25%, and pricing was up 57%.[5] Those figures do not prove that every increase comes from HBM. They do show that memory pressure is broad enough to show up in procurement-facing demand, lead-time, and price indicators rather than only in semiconductor investor commentary.

| Signal | What it measures | Why procurement should care |

|---|---|---|

| HBM reported sold out through 2026 | Allocation tightness for AI memory stacks | Signals limited ability for accelerator vendors to increase shipments even if logic wafers are available |

| CoWoS capacity target near 100,000 wafers per month | Back-end packaging expansion ambition | Shows that the critical capacity debate has shifted into advanced integration, not only wafer starts |

| DRAM and NAND price forecasts rising sharply | Expected mainstream memory price movement | Turns the AI buildout into a BOM risk for non-AI electronics programs |

| Memory demand, lead times, and pricing rising in Q2 2026 | Buyer-facing procurement conditions | Confirms that the constraint is affecting purchasing operations, not just chipmaker strategy |

The DDR5 Problem Is a Warning, Not a Complete Map

DDR5 is where the AI memory squeeze becomes visible to buyers who do not participate in AI accelerator allocation. Deloitte's outlook cites industry discussion that DDR5 prices could reach $700 by March 2026, up from about $250 in October 2025.[1] That is the kind of movement that turns a memory line item into a product-margin problem.

The same Deloitte report also notes that some industry pundits suggest consumer memory tightness could last a decade.[1] That line is useful as market color, not as a planning baseline. It is not a Deloitte-original firm forecast, and it is too broad to apply cleanly across all memory types, geographies, contract structures, or end markets. A buyer should not build a ten-year cost model from it. The practical takeaway is narrower: memory relief should not be assumed just because wafer capacity headlines improve.

The more dangerous mistake is treating each memory category as an isolated commodity update. DDR4, DDR5, NAND, NOR flash, and specialty memory do not all share identical supply dynamics, but they compete for supplier capital, production planning attention, and in some cases adjacent manufacturing resources. When HBM absorbs the strategic priority, non-AI memory buyers can find that their ordinary parts have become less ordinary in the allocation stack.

What Changes for Sourcing and BOM Planning

For most electronics, automotive, and industrial buyers, the answer is not to ask for direct HBM allocation. That leverage belongs mostly to the largest AI platforms, accelerator vendors, and server supply chains. The realistic work is to map where AI-driven memory and packaging constraints touch the company's own products, then update lead-time and cost assumptions before quotes arrive already stale.

The first planning change is to connect memory exposure to supplier allocation behavior. A BOM that includes DDR5, LPDDR, NAND, NOR flash, or memory-heavy modules should not be reviewed only through last quarter's price file. It should be reviewed against supplier concentration, approved-vendor-list flexibility, lifecycle status, substitution options, and the amount of engineering effort required to qualify an alternative.

The second change is to treat lead-time drift as an early warning, not as a clerical update. When distributor lead times move, when suppliers shorten quote validity, or when preferred parts begin arriving with allocation language, the issue may sit several steps upstream in memory or packaging economics. Teams using structured supplier monitoring can fold these signals into AI supplier risk scoring rather than waiting for a shortage notice to become the first official trigger.

The third change is to stop separating packaging risk from component risk. A finished AI server, high-end module, or memory-rich subsystem may be constrained by substrate availability, advanced packaging slots, test capacity, or HBM allocation before it is constrained by the nominal part number on the purchase order. Supplier scorecards that only grade financial health and on-time delivery miss the capacity layer where the 2026 bottleneck is forming.

This is where broader proactive supply chain risk management has to be concrete. A useful semiconductor resilience view should ask which products depend on memory categories exposed to HBM prioritization, which suppliers have limited alternates, which BOMs can tolerate qualified substitutes, and which customer commitments assume memory prices that no longer match the market. Some teams formalize that through an AI resilience score for supply chain planning process; others use simpler tiered reviews. The method matters less than whether memory, packaging, lead time, and BOM sensitivity are being evaluated together.

The Buyer Impact Is Already Outside the AI Lane

The AI accelerator shortage is not just a story about cloud capacity or chipmaker margins. It is a reordering of semiconductor priority that reaches buyers far from the accelerator socket. HBM gets allocated first. Advanced packaging slots become strategic capacity. Memory suppliers chase the richest mix. Ordinary electronics programs then discover that the parts they used to treat as manageable commodities now carry AI-cycle volatility.

That does not mean every memory part will be unavailable, or that every OEM faces the same exposure. It does mean procurement teams should stop treating wafer fab announcements as the main signal for AI chip supply. In 2026, the more useful questions are whether the required HBM is allocated, whether the package can be built, whether memory suppliers are protecting non-AI capacity, and how much BOM margin remains if DRAM and NAND pricing keep moving before the next sourcing cycle closes.

References

- 2026 Global Semiconductor Industry Outlook, Deloitte

- Semiconductors in 2026: AI Chips & Supply Chains, CrispIdea

- Key Trends Shaping the Semiconductor Industry in 2026, HTEC, April 2026

- AI's Chip Boom Is Creating Labor And Supply Chain Problems, Forbes, May 15, 2026

- Supply Chain Risks 2026, Supplyframe

Comments

Join the discussion with an anonymous comment.