The first problem with using AI to support automotive supply chain reshoring is not whether the technology is impressive. It is whether the math survives the finance review. Reshoring can add 10% to 30% in costs versus offshoring, based on BCG modeling republished by IBM, and that range is large enough to overwhelm a weak resilience story before procurement even gets to supplier qualification or plant readiness.[1]

Yet the reshoring discussion has not gone away. The Reshoring Initiative counted 244,000 reshored and foreign direct investment jobs announced in 2024, with 88% of those announced roles in high- or medium-high-tech categories; semiconductor and EV battery localization drove two-thirds of the activity.[2] The word “announced” matters. It does not mean hired, staffed, trained, or productive. But it does show where board attention, public incentives, and capital planning are moving.

That is the uncomfortable operating environment for automotive leaders in 2026: reshoring remains expensive, but the variables that used to sit outside the landed-cost model now sit inside the executive decision. Tariffs move. Logistics lanes lose reliability. Battery rules and localization pressures change sourcing options. A tier-two disruption can stop a final assembly line just as effectively as a tier-one failure. AI does not erase those costs. Its useful role is narrower: it can make the assumptions visible enough to defend, challenge, and revise before a reshoring commitment becomes a public promise.

The Cost Gap Is the Starting Line

A reshoring proposal that starts with patriotism or vague resilience language usually collapses into a spreadsheet argument anyway. Labor, capex, supplier development, engineering changeovers, tooling, energy, tax exposure, and inventory policy all have to be paid for somewhere. If the base case carries a 10% to 30% cost penalty, the business case has to show which risks are being removed, which costs are being avoided, and which uncertainties have become too expensive to ignore.[1]

The better question is not whether AI makes domestic production automatically cheaper than offshore production. The evidence does not support that claim. The better question is whether AI can reduce enough uncertainty around total cost, supplier risk, and localized EV supply chain design to make reshoring defensible against the alternatives.

That distinction also keeps ROI claims in their proper place. McKinsey estimates cited in current market materials suggest AI supply chain optimization can reduce logistics costs by up to 15%, cut inventory by 35%, and improve service levels by 65% in automotive contexts.[3] Those are useful benchmarks, not a blank check. The original source behind those figures was not verifiable, so they should be treated as directional estimates rather than guaranteed outcomes for a reshoring program.

For a CFO, that caveat is not academic. A logistics improvement in an existing network is not the same as a payback case for a new domestic supplier base. Inventory reduction in one product family does not prove a battery localization program will clear its hurdle rate. AI helps when it connects those pieces into a traceable model, not when it converts unrelated benchmarks into a universal ROI promise.

What AI Has to Prove

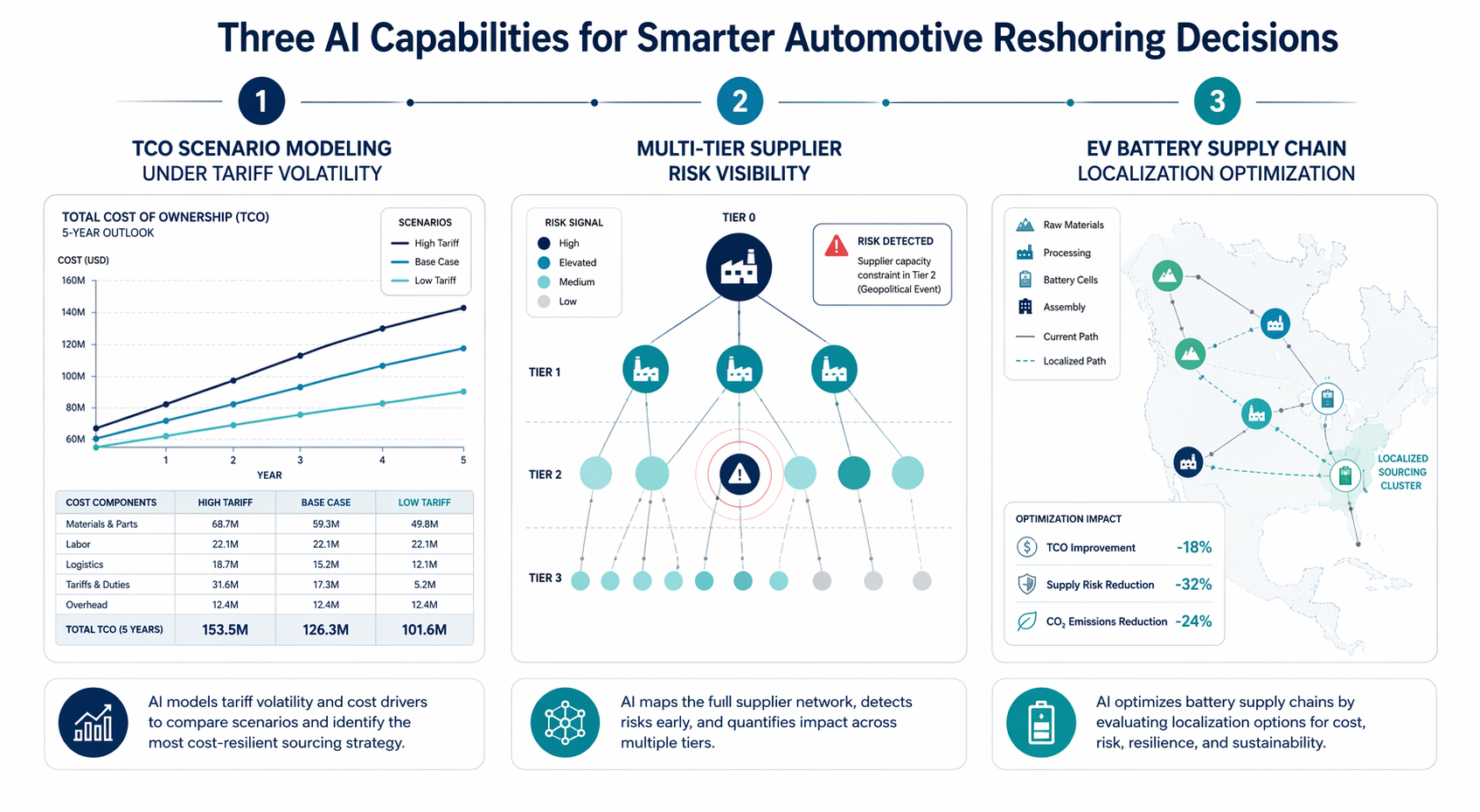

The strongest current case for AI in automotive reshoring sits in three capabilities. They are related, but they should not be collapsed into a single claim about “visibility.” Each answers a different executive objection.

| Capability | Decision It Supports | What It Must Make Auditable |

|---|---|---|

| TCO scenario modeling under volatility | Whether reshoring, nearshoring, dual sourcing, or continued offshoring has the best risk-adjusted cost profile | Tariff assumptions, logistics costs, inventory buffers, supplier transition costs, lead times, and sensitivity ranges |

| Multi-tier supplier risk visibility | Whether the current offshore or domestic network has hidden fragility that changes the sourcing decision | Supplier relationships beyond tier one, disruption signals, exposure by geography, and confidence levels |

| EV battery localization optimization | Where to place sourcing, processing, assembly, and inventory for battery-dependent programs | Material flows, qualifying suppliers, policy exposure, production timing, and trade-offs between cost and resilience |

The sequencing matters. Scenario modeling gives leadership a range of possible futures instead of one fragile business case. Supplier visibility tests whether the assumed network can actually operate under stress. Battery localization optimization then turns a policy or procurement objective into a physical supply chain design problem. A reshoring case that cannot separate those functions is hard to defend because no one can tell which assumption is doing the work.

Scenario Modeling: Make Volatility Explicit

Traditional landed-cost models were built for comparison, not volatility. They can compare labor rates, freight, duties, packaging, inventory, and working capital. They are less useful when the decision depends on tariff movement, supplier insolvency risk, port disruption, material scarcity, or battery-content rules that may change during the program life.

AI-assisted TCO modeling earns its place when it shows sensitivity rather than certainty. A useful model can run the same sourcing decision through different tariff, freight, inventory, and disruption assumptions, then show when the recommendation changes. If offshore supply wins in every scenario, that is an answer. If domestic or regional supply wins only when inventory buffers or disruption probability cross a certain threshold, that is also an answer. The value is not a prettier dashboard; it is the ability to show which assumption would have to be wrong for the recommendation to fail.

This is where the BCG/IBM cost penalty becomes useful rather than discouraging. A 10% to 30% gap should force a scenario model to identify the offsetting exposure. Is the current offshore source carrying unacceptable interruption risk? Is tariff uncertainty large enough to change the expected cost? Is expedited freight becoming a recurring operating cost rather than an exception? Is engineering change management slower because supplier collaboration spans too many time zones and tiers? AI can help test those questions, but the burden of proof stays with the business case.[1]

Supplier Risk Visibility: Detection Is Not the Same as Control

Multi-tier supplier visibility is the part of the AI reshoring argument that deserves the most attention because it changes the quality of the evidence. A sourcing director may know the tier-one supplier well and still be blind to a subcomponent, material processor, tooling constraint, or logistics dependency two tiers away. Reshoring does not fix that blindness by itself. A domestic plant can still depend on an offshore material stream, a single qualified chip, or a supplier whose own upstream network is fragile.

Ford’s disruption prediction work is a useful example because it is framed around signal detection, not generic transformation. The reported system uses time-series models to detect disruption signals across the supply base, with a cited precision of 0.85 in the source material.[4] Precision is not the same as full prevention, and it does not say every disruption can be avoided. It does suggest that AI can improve the timing and quality of supplier risk alerts before the impact reaches production.

That timing can change a reshoring decision. If a model repeatedly identifies early disruption signals in a current offshore network, the reshoring case can move beyond general geopolitical concern into a documented risk history. If the same model shows that risk is concentrated in one sub-tier material or geography, the answer may be targeted dual sourcing rather than full reshoring. That is a more useful outcome than a binary domestic-versus-offshore debate.

Audi’s work with Prewave points to a different part of the problem: external risk monitoring across languages and countries. The reported deployment monitors supply chain risks across 150 countries in more than 50 languages.[5] That is not the same capability as Ford’s time-series disruption prediction. It is a scanning layer, designed to catch weak signals from public, regional, and multilingual sources that a centralized procurement team may not see quickly enough.

For reshoring, that matters because the risk register is no longer limited to direct suppliers and familiar geographies. A materials shortage, labor dispute, weather event, regulatory action, or insolvency signal may first appear in local-language sources. AI monitoring does not make the signal true by itself. It gives the organization a faster reason to investigate, validate, and decide whether the sourcing assumption still holds.

BMW’s AIconic procurement control tower shows yet another distinction: procurement search and risk workflow at scale. The reported system supports more than 1,800 employees and handles over 10,000 searches daily for supply risk.[6] That is less about one prediction model and more about how a large procurement organization retrieves, compares, and acts on supplier risk information without forcing every buyer to build a separate evidence trail.

In a reshoring review, that operating model can be as important as the algorithm. If purchasing, logistics, compliance, and manufacturing are each using different supplier facts, the business case becomes a negotiation over whose spreadsheet is authoritative. A control tower can improve defensibility when it gives teams a common view of supplier exposure, search history, issue status, and escalation logic. It does not remove judgment, but it reduces the amount of judgment hidden in disconnected files.

Agent-Assisted Sourcing Moves the Decision Closer to Execution

Toyota’s reported deployment of AI procurement agents moves the discussion from monitoring into assisted decision work. Deloitte’s 2026 agentic supply chain report describes nine specialized AI agents on Azure OpenAI, deployed in early 2025 for design, compliance, and sourcing decisions.[7] The important point is not that agents replace sourcing professionals. It is that the system separates specialized tasks that are often blended together in a sourcing review.

Design input, compliance screening, supplier discovery, and sourcing recommendation are different activities with different failure modes. A design agent may surface component constraints earlier. A compliance agent may flag policy or documentation issues. A sourcing agent may compare suppliers against qualification criteria. In a reshoring case, those distinctions matter because the decision can fail for reasons that do not appear in the initial cost model: a domestic supplier cannot meet a design requirement, a documentation burden changes the launch timeline, or a substitute material introduces a qualification delay.

Agent-assisted procurement is still an area where governance has to be explicit. The defensible version keeps humans accountable for supplier selection, engineering approval, legal review, and commercial commitments. The risky version lets an agent’s recommendation appear more certain than the underlying data. For reshoring, where the capital and political stakes are high, every recommendation needs a visible path back to source data, assumptions, constraints, and approval history.

EV Battery Localization Is a Network Design Problem

EV battery localization is where reshoring language can become especially imprecise. A battery supply chain is not one supplier moved from one country to another. It involves materials, processing, cells, modules, packs, logistics, recycling, compliance, production timing, and qualification capacity. Semiconductor and EV battery localization accounted for two-thirds of 2024 reshoring and FDI job announcements in the Reshoring Initiative data, which explains why the topic dominates executive attention.[2]

AI can help here by optimizing across constraints that do not fit cleanly into a unit-price comparison. A battery localization model may need to compare supplier qualification lead times, transportation exposure, inventory policies, energy availability, compliance requirements, production ramp schedules, and exposure to policy shifts. The output should not be “local is better.” The output should show which network design best supports the vehicle program under defined assumptions.

This is also where announced manufacturing investment should be treated carefully. Stellantis has been reported as planning a $13 billion U.S. investment tied to more than 5,000 jobs, a 50% production increase by 2029, and fully modernized assembly lines.[8] Those figures are useful as a scale signal for domestic manufacturing modernization, but they should not be read as proof that every reshoring case clears its economics. A public investment plan is not the same as a verified unit-cost comparison or supplier-readiness audit.

The Evidence Is Stronger on Adoption Than on Universal Payback

There is enough evidence to say automotive manufacturers are moving AI into production-grade supply chain work. Ford’s disruption prediction, Audi and Prewave’s multilingual monitoring, BMW’s procurement control tower, and Toyota’s specialized procurement agents are not abstract whiteboard examples.[4][5][6][7] They show real operational categories: signal detection, external risk monitoring, enterprise procurement search, and agent-assisted sourcing.

There is less evidence to say AI reliably eliminates the reshoring cost penalty. The ROI benchmarks are promising, but the McKinsey figures should be treated as estimates, and some OEM outcome claims circulating in secondary sources need verification against original OEM or vendor publications before they are used as hard proof in a board case.[3] That does not weaken the practical argument for AI. It narrows it to the part that can be defended.

The manufacturing investment environment supports continued AI adoption. Deloitte’s 2026 Manufacturing Industry Outlook reports that 80% of manufacturing executives plan to invest at least 20% of their improvement budgets in smart manufacturing.[9] That is adoption intent, not reshoring effectiveness. It suggests the tooling budget is becoming easier to justify, while the reshoring decision still has to stand on its own economics.

When AI Makes Reshoring Defensible

AI makes a reshoring decision defensible when it changes the quality of the evidence presented to leadership. A defensible case does not say the organization wants resilience. It shows the scenarios tested, the assumptions that moved the recommendation, the supplier risks found below tier one, the cost of doing nothing, and the operating constraints attached to a localized network.

That case should be able to answer several questions without rebuilding the model from scratch: What happens if tariffs change? Which supplier node creates the highest production risk? How much inventory is being carried because of uncertainty rather than planned service strategy? Which domestic or regional suppliers are qualified, and which only appear viable before engineering review? What is the launch risk if battery materials, cells, modules, and pack assembly are localized on different timelines?

The answer may still be no. AI can show that the reshoring premium is too high, that a dual-source strategy is enough, or that supplier development would take longer than the program allows. Those are valuable outcomes. They prevent a public commitment from outrunning the operating model.

The answer may also be yes, but only under specific conditions: when tariff exposure and disruption risk materially change expected cost; when multi-tier visibility shows fragility that the old sourcing model underpriced; when EV battery localization improves program control enough to justify the added cost; and when the assumptions remain auditable after the announcement.

That is the useful boundary. AI does not make automotive reshoring cheap. It can make reshoring defensible when it is used to model total cost under volatility, expose supplier risk across tiers, and optimize localized EV supply chains with assumptions that executives can inspect before they commit.

References

- BCG modeling on reshoring cost penalties, IBM, 2023.

- Reshoring Initiative 2024 Data Report, Reshoring Initiative.

- McKinsey estimates on AI supply chain optimization in automotive contexts, McKinsey & Company.

- Ford disruption prediction AI case material, Futurice blog / Scalence.

- Audi / Prewave multilingual supply chain risk monitoring case material, Scalence.

- BMW AIconic procurement control tower case material, Star Global.

- 2026 agentic supply chain report, Deloitte, 2026.

- Stellantis $13B manufacturing plan coverage, IndustrialSage.

- 2026 Manufacturing Industry Outlook, Deloitte, 2026.

Comments

Join the discussion with an anonymous comment.