The budget-room answer to the advantages of supply chain control tower investments is narrower than most sales decks make it sound. The defensible ROI case does not rest on “visibility” as a standalone benefit. It rests on a small group of financial outcomes that can survive a CFO’s follow-up questions: revenue protection, logistics cost reduction, inventory reduction, supply cost reduction, planner productivity, and payback period.

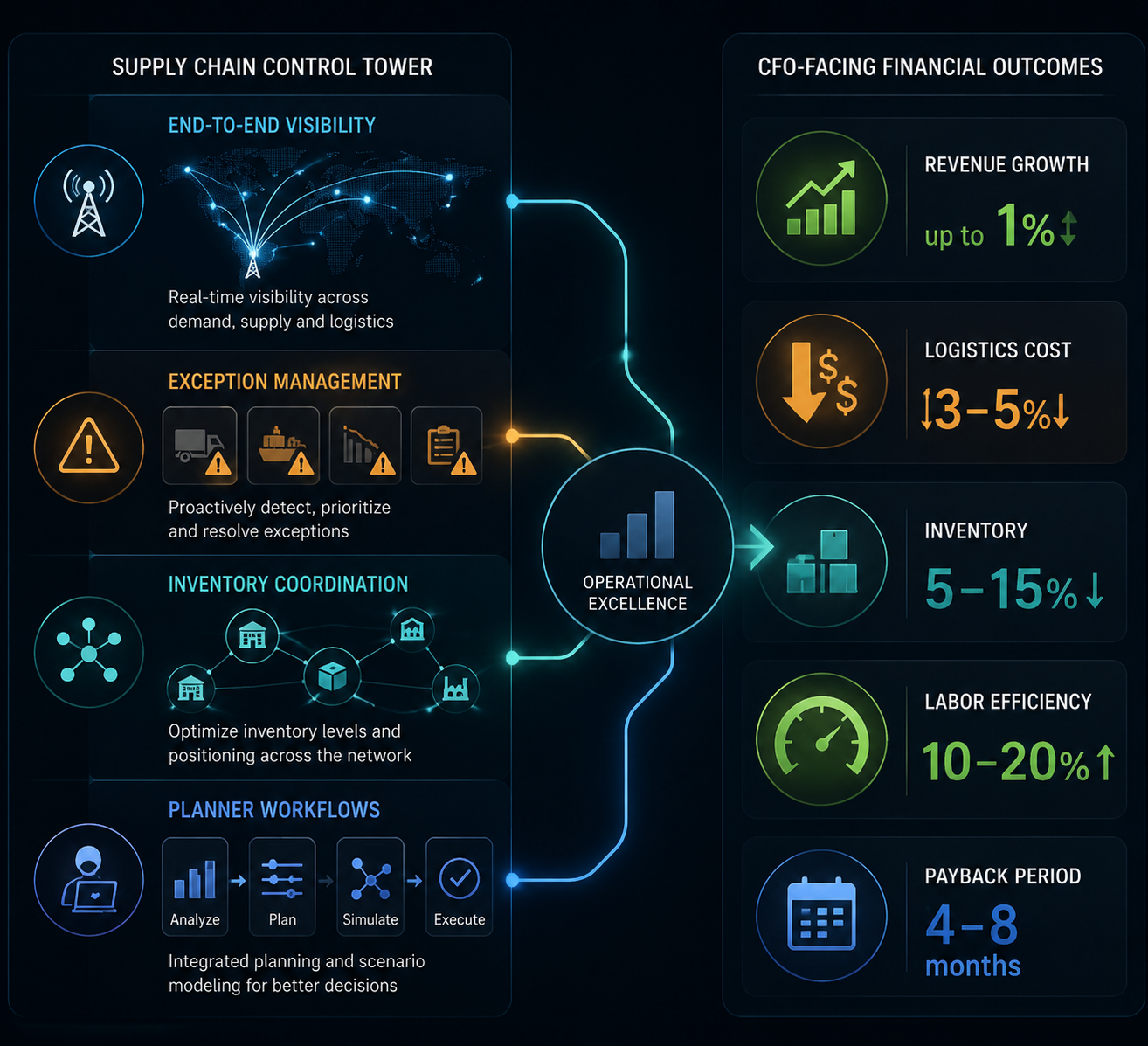

The strongest benchmark set comes from converging, source-attested figures rather than one spectacular deployment story. Accenture reports up to 1% revenue increase from reduced lost sales, 3–5% logistics cost reduction, and 10–20% labor efficiency improvement from supply chain control tower solutions.[1] McKinsey’s nerve-center analysis translates the same general operating idea into executive-scale economics: for a $10 billion company, up to 2% earnings improvement, a $150 million sales boost, and $50 million in cost reduction.[2] CE Interim, citing Nucleus Research and One Network, adds 8% supply cost reduction, 2x–10x productivity gains in certain functions, and a documented 30% inventory reduction in an automotive deployment.[3] FourKites says modern AI-powered control tower implementations can reach 4–8 month payback periods, with one top-15 global food-and-beverage customer reporting more than $500,000 in detention cost reduction, about $800,000 in OTIF penalty reduction, and 35% logistics team productivity improvement.[4]

| ROI category | Source-attested figure | CFO translation |

|---|---|---|

| Revenue protection | Up to 1% revenue increase; McKinsey example: $150M sales boost for a $10B company | Reduced lost sales, better allocation, faster response to supply disruption |

| Logistics cost | 3–5% logistics cost reduction; FourKites customer case: $500K+ detention reduction | Lower detention, fewer expedites, faster exception resolution, tighter carrier execution |

| Supply cost | 8% supply cost reduction, cited by CE Interim from Nucleus Research | Less waste in procurement and supply execution, better coordination across constraints |

| Inventory | 5–15% general reduction range; 30% automotive case cited by CE Interim from One Network | Lower working capital, fewer buffers, better synchronization across nodes |

| Labor productivity | 10–20% labor efficiency improvement; 2x–10x function-specific productivity gains cited from Nucleus Research | Planner and logistics teams spend less time chasing status and more time on decisions |

| Payback | 4–8 months for modern AI-powered implementations, according to FourKites survey material | Shorter approval path if scope, baseline, and benefit ownership are explicit |

What These Numbers Actually Fund

A control tower business case usually fails when it asks finance to buy a system of attention. Finance does not own attention as a P&L line. It owns revenue, gross margin, logistics spend, working capital, headcount productivity, and capital allocation. The control tower has to be translated into those terms before the approval conversation starts.

Revenue lift is the cleanest top-line argument, but it is also the easiest to overstate. Accenture’s “up to 1%” figure is specifically tied to reduced lost sales, not a general claim that a control tower creates new demand.[1] That distinction matters. The investment case should show where demand already exists but revenue leaks because product is in the wrong place, allocation decisions arrive late, substitutions are not coordinated, or a disruption is visible only after the customer has already missed the delivery window.

McKinsey’s $10 billion-company example gives executives a useful scale reference. A $150 million sales boost and $50 million cost reduction are large enough to matter at the CEO level, but the numbers come from a nerve-center model, not necessarily a software-only deployment.[2] That makes the figure powerful and bounded. It supports the argument that an integrated operating layer can move enterprise economics; it does not prove that buying a dashboard without process authority will do the same.

Logistics cost reduction is often easier to defend because the leakage is already visible in invoices: detention, demurrage, spot premiums, expedites, manual exception handling, missed appointments, and carrier performance variation. Accenture’s 3–5% logistics cost reduction benchmark gives a reasonable range for the budget model.[1] FourKites’ customer case makes the mechanism more concrete: a top-15 global food-and-beverage company reported more than $500,000 in detention cost reduction and about $800,000 in OTIF penalty reduction after using AI-powered digital workers inside its control tower environment.[4]

That case is useful because it names the cost pockets. It is also still a vendor-published customer case, so it should not carry the whole investment proposal. The better use is to let Accenture anchor the logistics range, then use the food-and-beverage example to show how a line item could move when alerts turn into assigned work, exception triage, and faster intervention.

Inventory Reduction Is a Working-Capital Argument, Not a Visibility Claim

Inventory is where the word “visibility” creates the most confusion. Seeing more inventory does not automatically reduce it. Inventory comes down when better information changes planning confidence, replenishment timing, safety-stock policy, allocation, or coordination across suppliers, plants, distribution centers, and customers.

The available evidence supports a general 5–15% inventory reduction range, with CE Interim citing a One Network automotive deployment that documented a 30% inventory reduction.[3] The 30% figure is a real case reference, not a normal expectation for every buyer. In a CFO-facing model, it belongs in the upside scenario unless the company has similar baseline conditions: excess buffers, fragmented planning, poor supplier synchronization, or a multi-enterprise network where inventory exists because no one trusts the timing of the next node.

The finance translation is straightforward. Lower inventory can release working capital, reduce carrying costs, lower obsolescence exposure, and improve turns. The operating translation is less automatic. Someone has to change the reorder logic, review safety-stock settings, coordinate exception thresholds, and accept the service-level risk that comes with reducing buffers. A control tower can provide the confidence and coordination to do that; it does not make the policy decision by itself.

Labor Productivity Needs a Baseline Before It Becomes Savings

Labor efficiency is one of the most attractive control tower benefits because supply chain organizations know how much time disappears into status checks, spreadsheet reconciliation, carrier follow-up, order chasing, and meeting preparation. Accenture’s 10–20% labor efficiency improvement is a useful planning range.[1] McKinsey adds the operational context: 40–60% of planner time is spent on transactional rather than strategic work.[2]

That is a strong argument, but it needs careful wording. Productivity is not always headcount reduction. Sometimes it is avoided hiring. Sometimes it is faster response with the same team. Sometimes it is planner time redirected from “where is the load?” to “which customer, plant, or supplier gets priority?” A CFO will ask which of those is being claimed.

The Nucleus Research productivity range cited by CE Interim — 2x–10x gains in certain functions — is potentially valuable, but it should be used with the phrase “function-specific” attached.[3] A narrow activity such as exception classification or status retrieval can improve by multiples when automated. That does not mean the entire supply chain planning organization becomes 10 times more productive. The investment case is stronger when it separates task-level automation from organization-level labor efficiency.

Payback Is the Approval Accelerator, But Only If Scope Is Clear

FourKites’ 4–8 month payback claim for modern AI-powered control towers is the kind of figure that gets attention in 2026 budget reviews.[4] It also needs the most context. A short payback period is more plausible when the implementation targets high-friction workflows with measurable leakage: detention, appointment failures, OTIF penalties, manual exception queues, or customer-service escalations. It is less plausible when the first phase is mostly data harmonization, network onboarding, or executive reporting.

This is where the control tower model matters. A visibility layer may improve awareness but leave the work in the same inboxes. An exception-management layer can assign, prioritize, and close the loop. A broader operating nerve center can connect planning, logistics, inventory, and commercial tradeoffs. IBM describes control towers in terms of end-to-end visibility across supply chain processes, while McKinsey’s nerve-center framing emphasizes an operating construct that bridges functions and decisions.[5][2] Those are related ideas, but they are not identical investment cases.

A buyer should therefore define the object being funded before presenting the ROI. Is the proposal for software, a cross-functional operating model, AI agents for exception work, a transportation visibility layer, an inventory coordination layer, or some combination of those? The same phrase can cover all of them. The ROI range becomes more credible when each benefit is tied to the specific operating change that produces it.

How to Calibrate the Evidence

The evidence base is strong enough to anchor an investment case, but not strong enough to justify guaranteed savings language. There is no large, independent, peer-reviewed study among the cited sources that isolates control tower ROI across a broad sample of companies. Most numbers come from consulting research, practitioner analysis, vendor ecosystem data, or documented deployments. That does not make the numbers unusable. It means the source hierarchy has to be explicit.

| Evidence source | Best use in the business case | How to qualify it |

|---|---|---|

| Accenture | Primary benchmark for revenue, logistics cost, and labor efficiency | Use as directional range; tie each figure to the specific value driver Accenture names |

| McKinsey | Executive-scale nerve-center economics and planner-time context | Make clear the example is a nerve-center model and was published in 2021 |

| Nucleus Research via CE Interim | Support for supply cost reduction and function-specific productivity gains | Avoid applying 2x–10x productivity to the whole organization |

| One Network case via CE Interim | Concrete upside example for inventory reduction | Treat 30% as a case result, not the base case |

| FourKites | Current AI-powered control tower examples and payback discussion | Label as vendor-published survey and customer case material |

Accenture and McKinsey should carry the load-bearing parts of the case because they translate control tower and nerve-center capabilities into revenue, cost, labor, and earnings language. Nucleus Research, as cited by CE Interim, adds useful support around supply cost and productivity. FourKites is valuable for current AI-powered operating examples, especially where digital workers are tied to detention, OTIF penalties, and logistics team productivity. It should be presented as vendor-published evidence, not as independent market proof.

The FourKites survey context is especially useful as a caution. Its blog states that only 22% of 250 surveyed respondents said their control towers were highly effective.[4] That does not disprove ROI; it explains why vague visibility programs disappoint. The investment case should not assume that a control tower automatically changes behavior. It should name who receives the alert, who owns the exception, what decision rights change, and which financial line captures the result.

Building the CFO Version of the Case

A finance-ready control tower proposal does not need dozens of metrics. It needs a small number of value drivers with baselines, owners, and timing. For a deeper value-driver worksheet, the parallel resource on control tower software ROI can sit behind the executive version. The front-room version should be simpler.

- Start with the leakage baseline: lost sales, detention, expedites, OTIF penalties, excess inventory, manual exception hours, or supply cost variance.

- Assign each benefit to a source range: Accenture for revenue, logistics, and labor; McKinsey for nerve-center earnings scale; Nucleus via CE Interim for supply cost and productivity; FourKites for AI-powered payback and operating examples.

- Separate base-case, upside-case, and case-study figures. A 5–15% inventory reduction range belongs in the model differently from a documented 30% automotive result.

- Define benefit ownership. Logistics owns detention and expedites; planning owns inventory assumptions; commercial teams may own lost-sales recovery; finance validates whether productivity becomes savings, capacity, or service improvement.

- State what the control tower includes. A dashboard, an exception workflow, AI-powered digital workers, and a cross-functional nerve center do not carry the same ROI assumptions.

The strongest version of the case does not ask the CFO to believe in transformation. It asks the CFO to accept a set of bounded assumptions. If logistics spend is large enough, a 3–5% reduction has a measurable P&L effect. If lost sales are material, up to 1% revenue lift is worth testing against the company’s own service and availability data. If planners are spending close to McKinsey’s 40–60% transactional-time range, automation and exception management have a credible productivity target.[1][2]

AI use cases can make that case sharper when they attach to specific work rather than a generic “smarter tower” promise. Exception prioritization, appointment-risk detection, automated status retrieval, detention prevention, and OTIF-risk triage are easier to model than broad visibility. The companion analysis of control tower AI applications is useful when the investment committee wants to know which AI functions produce measurable outcomes rather than which vendor has the broadest feature list.

The Caveats That Keep the ROI Claim Honest

The first caveat is category ambiguity. “Control tower” can mean an organizational nerve center, a software platform, a transportation visibility product, a planning-and-execution layer, or a combined operating model. The ROI claim should match the model. McKinsey’s nerve-center economics should not be pasted onto a reporting dashboard. A vendor customer case should not be treated as an independent benchmark. A task-level productivity gain should not be scaled across all supply chain labor without a workload study.

The second caveat is baseline dependence. Companies with high detention exposure, frequent expedites, poor OTIF performance, excess buffers, or fragmented exception ownership have more visible leakage to recover. Companies that already have disciplined transportation execution, clean master data, mature planning processes, and tight inventory governance may still benefit, but the near-term ROI ceiling is lower.

The third caveat is timing. FourKites’ 4–8 month payback claim can be credible for targeted AI-powered workflows, but broader enterprise control tower programs may include integration, governance, data quality, and change-management work that pays back on a different timeline.[4] If the proposal includes both a fast detention-reduction use case and a slower network-wide planning integration, those should not be blended into one payback number.

The fourth caveat is benefit conversion. A planner who saves time does not automatically create EBITDA improvement. A warehouse that sees inbound risk earlier does not automatically reduce inventory. A logistics team that receives better alerts does not automatically avoid detention unless decision rights, escalation rules, and carrier actions change. Control tower ROI is earned in the operating model after the signal appears.

A responsible 2026 investment case can still be strong. The independent and semi-independent evidence converges around a practical range: up to 1% revenue lift, 3–5% logistics cost reduction, 8% supply cost reduction, 5–15% inventory reduction with higher case-specific upside, 10–20% labor efficiency improvement, and potentially short payback for targeted AI-powered implementations.[1][3][4] Those are usable numbers when they are attributed correctly, modeled as directional ranges, and tied to a clearly defined control tower model.

References

- Benefits of Supply Chain Control Tower Solutions — Accenture

- Building a digital bridge across the supply chain with nerve centers — McKinsey

- Supply Chain Control Tower: Real-Time Visibility & ROI — CE Interim

- Why Supply Chain Control Towers Didn't Deliver on Their Promise (And What's Changing) — FourKites

- What is a Supply Chain Control Tower? — IBM

Comments

Join the discussion with an anonymous comment.