Market Context: The AI Supply Chain Tools Landscape in 2026

The gap between intent and execution in supply chain AI has never been wider. According to a 2025 ABI Research survey of 490 professionals across the US, Mexico, Germany, and Malaysia, 94% of supply chain companies plan to deploy AI or generative AI for decision support within two years. Yet a Gartner survey of 120 supply chain leaders in 2025 found that only 23% of organizations have a formal AI strategy in place. That 71-point delta between ambition and structured execution defines the market in Q2 2026.

The financial stakes are substantial. Accenture's 2024 analysis of 1,148 companies across 10 industries in 15 countries found that organizations with AI-mature supply chains are 23% more profitable than their peers. McKinsey estimates that AI-enabled distribution can reduce logistics costs by 5–20%, cut inventory by 20–30%, and lower procurement spend by 5–15%. Meanwhile, 85% of executives plan to increase AI spending in 2026, with 1 in 5 expecting a 20% or greater increase, per a 2025 Supply Chain Brain survey.

This strategy-implementation gap is not just a planning problem — it is a vendor evaluation problem. When 64% of supply chain leaders say AI capabilities are important when evaluating new technology (ABI Research 2025), but most organizations lack the internal frameworks to distinguish genuine AI integration from marketing veneer, the risk of selecting the wrong platform — or the wrong tier of platform — is high.

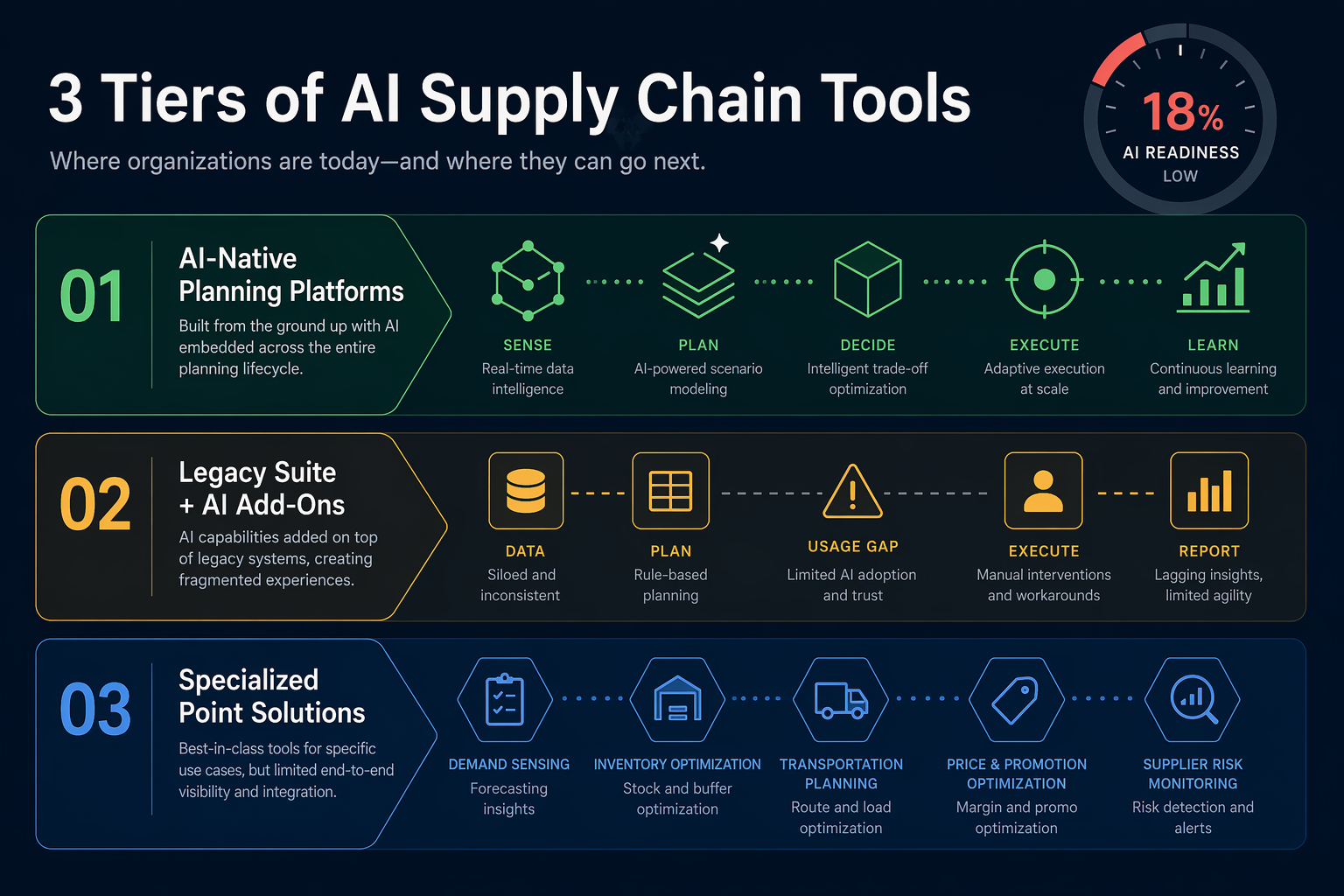

The 2026 AI supply chain tools market splits into three distinct tiers, each with different architecture, adoption patterns, and risk profiles. Understanding which tier fits your organization's AI maturity, integration landscape, and speed-to-value requirements is the core evaluation challenge.

Tier 1: AI-Native Planning Platforms — Where ML Is the Core

AI-native platforms were built from the ground up with machine learning as their planning engine, not as an add-on layer atop a deterministic rules-based system. This architectural choice has measurable consequences for user satisfaction and adoption. G2 review scores collected in mid-2025 place AI-native platforms at the top of the satisfaction spectrum: Flowlity at 4.9/5, ToolsGroup at approximately 4.7/5, and o9 at 4.2/5.

These platforms share several structural characteristics. They ingest large volumes of historical and real-time data, generate probabilistic forecasts rather than single-point estimates, and continuously retrain models as new data arrives. They are designed for planners who want to interrogate model outputs, adjust assumptions, and run what-if scenarios — not for organizations that want a black-box forecast delivered on a fixed schedule.

| Platform | G2 Score (mid-2025) | Core Differentiator | Notable 2026 Development |

|---|---|---|---|

| Flowlity | 4.9/5 | MCP server for external AI assistant integration | Production MCP server (Flowlity Co-planner) enables Claude, ChatGPT, and Microsoft Copilot to query live planning data |

| ToolsGroup | ~4.7/5 | Strong AI use cases across demand and inventory | Continued focus on probabilistic planning for retail and CPG |

| o9 Solutions | 4.2/5 | Enterprise Knowledge Graph for complex global supply chains | Digital Brain platform expansion; user-friendly interface remains a noted challenge |

| Kinaxis | 4.0/5 | Concurrent planning with AI for exception management | Maestro Chat adopted by ~2/3 of user base; Maestro Agents launched October 2025 |

| Relex | Not in G2 comparison | AI-native for retail and grocery forecasting | Best-in-class demand forecasting for retail verticals |

Real-world outcomes from AI-native deployments are documented but require careful source attribution. A pharmacy services company deploying Kinaxis Maestro improved forecast accuracy by 47%, reduced on-hand inventory by 14%, and improved inventory turns by 34% within three months, per vendor-published case study data. A global candy maker operating in 80+ countries with 34,000+ employees improved forecast accuracy by over 23% using E2open Demand Planning and Demand Sensing. These figures represent vendor-reported outcomes and may reflect cherry-picked results rather than typical performance.

Tier 2: Legacy Suite AI Upgrades — What Works vs. What's Still Aspirational

The largest installed base in supply chain planning belongs to the legacy enterprise suites: SAP IBP, Blue Yonder, and Oracle SCM Cloud. Each has announced significant AI investments. The critical question for evaluators is not whether these vendors have AI features on their roadmaps, but whether those features are actually being used in production by real customers.

The evidence suggests a significant adoption gap. G2 satisfaction scores for legacy suites trail AI-native platforms by a notable margin: SAP IBP at 4.3/5, Blue Yonder at 4.1/5, and Kinaxis at 4.0/5. More tellingly, an independent critique cited in Flowlity's vendor comparison notes that "almost no customers" of Blue Yonder are using AI in day-to-day planning operations. Blue Yonder launched "Cognitive Solutions" agents built on Microsoft Azure AI Foundry in 2025, but the gap between announcement and production adoption remains wide.

| Vendor | G2 Score (mid-2025) | AI Feature Announced | Adoption Reality |

|---|---|---|---|

| SAP IBP | 4.3/5 | MCP support for SAP HANA Cloud (Q1 2026) | Infrastructure-level support, not natively within IBP workflows |

| Blue Yonder | 4.1/5 | Cognitive Solutions agents on Azure AI Foundry (2025) | Independent critique: "almost no customers" using AI in day-to-day planning |

| Oracle SCM Cloud | Not in G2 comparison | AI-powered supply chain planning features | Limited independent data on production AI adoption |

This does not mean legacy suites should be dismissed. For organizations with deep SAP or Oracle ERP investments, the integration cost of switching to an AI-native platform may outweigh the AI capability gap. The question is whether the AI features offered by the legacy suite are sufficient for the organization's planning complexity, or whether they represent a minimum viable product that will require significant internal development to operationalize.

A pragmatic evaluation approach: ask each legacy suite vendor for the names of three customers using their AI features in production for at least six months, and conduct reference calls focused on adoption depth, not just purchase intent. If the vendor cannot provide such references, the AI capability is likely still aspirational.

Tier 3: Specialized Point Solutions — Dominating Specific Functions

For organizations that need deep capability in a single supply chain function — and are willing to manage integration across multiple platforms — specialized point solutions often deliver the highest ROI. These vendors focus on one domain, accumulate domain-specific training data, and build features that generalist platforms cannot justify developing.

| Function | Representative Vendor | Documented Outcome | Source Type |

|---|---|---|---|

| Demand Forecasting (Retail) | Relex | AI-native forecasting for retail/grocery; best-in-class per multiple analyst assessments | Analyst consensus |

| Logistics Visibility | FourKites | Real-time shipment tracking and predictive ETAs across modes | Industry standard |

| Supplier Risk | Interos | Multi-tier supplier risk scoring and monitoring | Industry standard |

| Procurement Automation | Pactum | Veritiv (5,000-6,000 suppliers) improved long-tail supplier efficiency and uncovered COGS savings | Vendor case study |

| Logistics Optimization | 7bridges | Philipp Plein: €2M annual savings, 17x ROI | Vendor case study |

| Route Optimization | Shipsy | Kout Food Group: 20% reduction in delivery time, 37.5% improvement in order clubbing efficiency | Vendor case study |

| Spend Analytics | LevaData | Global manufacturer: $14M cost savings | Vendor case study |

The trade-off with point solutions is integration complexity. Each additional platform creates another data pipeline to maintain, another set of API contracts to manage, and another vendor relationship to oversee. For organizations with mature data engineering teams and a clear integration architecture (data lake, API gateway, event bus), this cost is manageable. For organizations still running supply chain on spreadsheets and email, the integration burden of multiple point solutions can outweigh their functional advantages.

Decision Framework: When to Choose AI-Native vs. Suite vs. Point

No single tier is optimal for every organization. The right choice depends on your current AI maturity, integration landscape, organizational capacity for change management, and speed-to-value requirements. The following framework maps organizational profiles to the appropriate tier.

| Evaluation Dimension | AI-Native Platform | Legacy Suite + AI | Point Solution |

|---|---|---|---|

| Best for AI maturity | Organizations with existing data infrastructure and ML capability | Organizations with deep ERP investment and limited AI readiness | Organizations with a single high-priority pain point |

| Integration complexity | Moderate to high; requires data pipeline modernization | Low; leverages existing ERP data and workflows | High; each point solution adds a new integration |

| Speed to value | 3–12 months depending on data readiness | 6–18 months; AI features may require additional configuration | 1–6 months for the specific function |

| Scalability across functions | High; designed to expand across planning, procurement, logistics | High; suite covers all functions, but AI depth varies | Low; limited to the specific function |

| User satisfaction (G2) | 4.0–4.9/5 | 4.0–4.3/5 | Varies widely by vendor |

| Risk of AI feature non-adoption | Low; AI is the core value proposition | High; AI features may go unused in practice | Low; the solution exists specifically for the AI use case |

A common pattern in 2026 is the hybrid approach: an AI-native platform for demand planning and inventory optimization (where ML accuracy directly impacts working capital), a legacy suite for transactional procurement and order management (where ERP integration is paramount), and a point solution for logistics visibility or supplier risk (where domain-specific data networks provide unique value). This approach maximizes capability where it matters most while minimizing disruption to existing workflows.

2026 Trends Shaping the Market: Agentic AI, MCP Protocols, and Digital Twins

Three technology trends are reshaping the vendor evaluation landscape in 2026, and each has implications for which tier of platform will serve an organization best over a 3–5 year horizon.

Agentic AI for Autonomous Exception Handling

Gartner predicts that 15% of daily logistics decisions will be made autonomously by AI agents by 2028, and that by 2031, 60% of supply chain disruptions will be resolved without human intervention. These are not distant forecasts — they are near-term planning assumptions that should influence platform selection today.

A Fortune 500 manufacturer using agentic AI achieved 100% visibility into supplier commitments, three weeks' advance warning of disruptions, and a 30% reduction in supply-driven stockouts, per a 2026 Unframe case study. This represents an early production deployment of the pattern Gartner describes. The implication for vendor evaluation: ask each platform vendor how their architecture supports agentic decision-making — not just alerting, but autonomous action with human oversight. AI-native platforms with open APIs and event-driven architectures are better positioned here than legacy suites with rigid workflow engines.

MCP and Open Protocol Support

The Model Context Protocol (MCP) is emerging as a standard for connecting AI assistants to live data sources. Flowlity's production MCP server, which enables Claude, ChatGPT, and Microsoft Copilot to query live planning data, is the most advanced example in the supply chain space as of Q2 2026. SAP IBP has announced MCP support at the SAP HANA Cloud infrastructure level, but not natively within IBP workflows.

For evaluators, MCP support is not yet a must-have criterion — the standard is too new, and most organizations have not integrated external AI assistants into their planning workflows. But it is a leading indicator of architectural openness. Platforms that support MCP or similar open protocols today will be better positioned to integrate with the next generation of AI tools than those that require proprietary interfaces.

Digital Twins for Scenario Planning

Digital twin adoption for supply chain scenario planning is accelerating, driven by the need to model tariff impacts, supplier diversification, and inventory positioning under uncertainty. AI-native platforms with digital twin capabilities allow planners to simulate the effect of a 25% tariff on Chinese-sourced components, a port closure in Rotterdam, or a supplier bankruptcy — and get probabilistic outcomes rather than deterministic guesses.

The key evaluation question for digital twin capabilities is not whether the vendor offers a "digital twin" feature (most do, in some form), but whether the digital twin is connected to live operational data and can be updated in near-real-time. A digital twin that requires a week of data preparation to run a scenario is a consulting tool, not an operational planning capability.

Evaluation Checklist: Cutting Through the Hype

The following checklist is designed to help evaluators distinguish genuine AI capability from marketing claims. It complements the broader evaluation methodology covered in the 2026 AI Supply Chain Tool Buyer's Guide, which provides a full evaluation framework. This checklist focuses specifically on the AI adoption gap.

- Verify AI feature adoption rates with reference customers. Ask each vendor for three customers using their AI features in production for at least six months. Conduct reference calls focused on: What percentage of planners actually use the AI features daily? What was the adoption curve? What features were announced but never used?

- Test explainability and transparency. Ask the vendor to explain, in plain language, how their AI model arrived at a specific forecast or recommendation. If the answer is "the model learned from the data" without a clear explanation of feature importance, training data scope, and confidence intervals, the system lacks the transparency required for production planning decisions.

- Assess data integration requirements honestly. The most common barrier to AI adoption is data quality and fragmentation. Ask the vendor: What data sources are required? What data quality thresholds must be met? How long does initial data integration typically take? If the vendor says "we can integrate in two weeks," ask for the names of customers who achieved that timeline with similarly complex data landscapes.

- Validate ROI claims against independent benchmarks. McKinsey's benchmarks (5–20% logistics cost reduction, 20–30% inventory reduction) are a useful reference range. If a vendor claims results significantly above these ranges, ask for the methodology behind the projection and for references from customers in similar industries with similar data maturity.

- Distinguish between AI features and AI adoption. A vendor may have 50 AI features on their roadmap but zero customers using them in production. Ask: How many customers are using each AI feature in production? What is the median time from purchase to first AI feature deployment? What is the most common reason customers abandon AI features after purchase?

- Evaluate the vendor's AI governance and model management capabilities. As AI features become more autonomous, the ability to monitor model drift, audit decisions, and maintain human oversight becomes critical. Ask: How do you monitor model accuracy over time? What happens when model accuracy degrades? How are model updates communicated to planners? What is the rollback process?

The 2026 AI supply chain tools market offers more capability than ever, but also more noise. The three-tier framework — AI-native platforms, legacy suite AI upgrades, and specialized point solutions — provides a structured way to evaluate options based on your organization's AI maturity, integration landscape, and speed-to-value requirements. The critical insight is that AI features on a roadmap are not the same as AI adoption in production. The vendors that can demonstrate real-world usage, transparent methodology, and measurable outcomes are the ones worth shortlisting.

Comments

Join the discussion with an anonymous comment.