Market Context: The AI Supply Chain Landscape in 2026

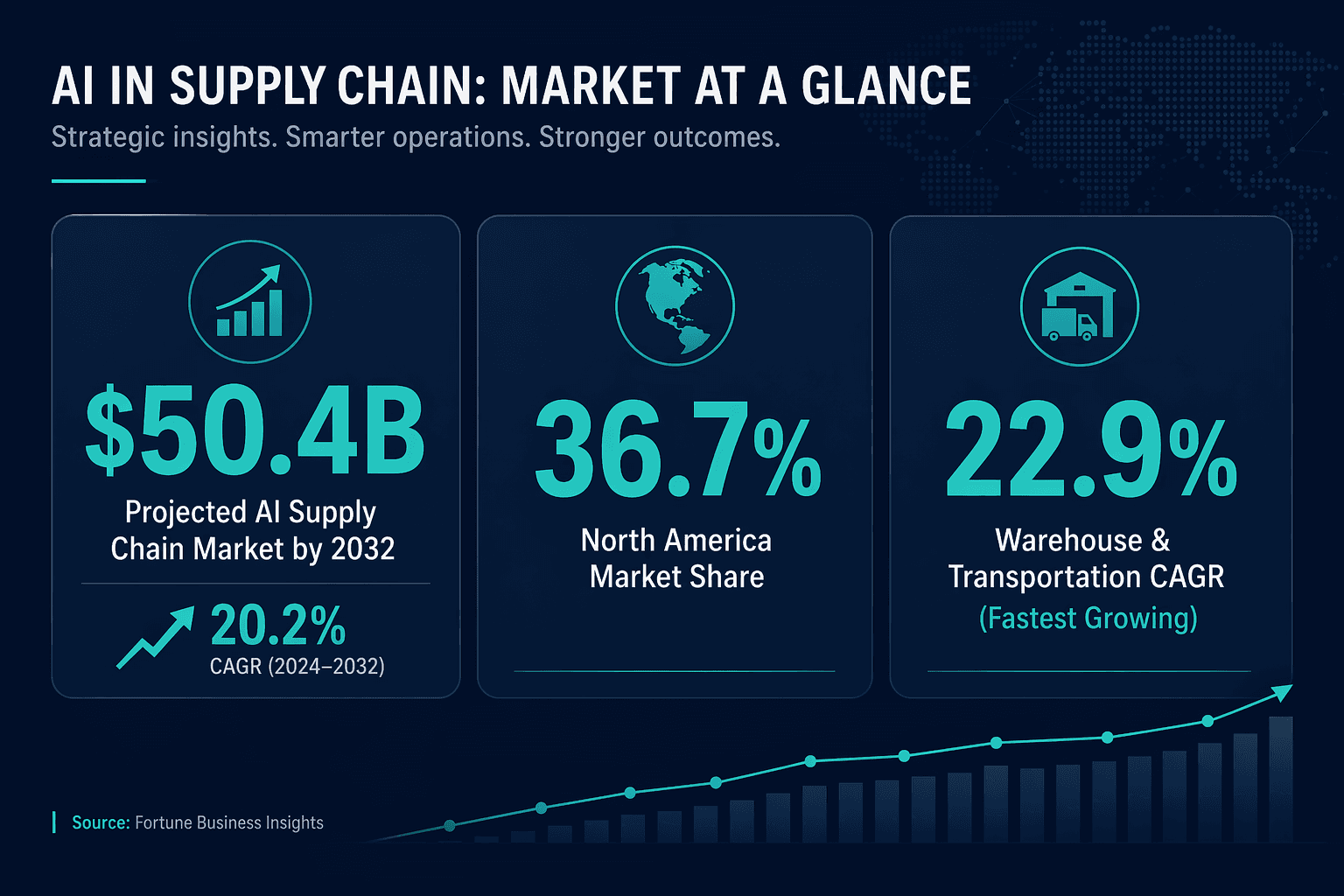

The market for AI in supply chain has crossed a critical threshold. According to MarketsandMarkets (Report SE 6402, January 2026), the sector was valued at $13.93 billion in 2025 and is projected to reach $50.41 billion by 2032, growing at a compound annual rate of 20.2%. North America currently holds the largest regional share at 36.7%, while warehouse and transportation management — the fastest-growing application segment — is expanding at a 22.9% CAGR.

These top-line numbers, however, mask a more uneven reality on the ground. The Oliver Wyman and Prequel Ventures EU Supply Chain Tech Report (February 2026) found that only about 15% of companies have achieved full industrialization of AI across their supply chain functions. The top 15% of adopters enjoy nearly three times the technology industrialization advantage over the bottom 15%. The primary barrier cited by two-thirds of survey respondents is poor and fragmented data quality — not a lack of available AI technology.

This gap between market potential and real-world deployment maturity is precisely why a structured vendor directory matters. Supply chain leaders evaluating AI investments need to understand not just which companies offer AI, but which category of AI they offer — and whether that category aligns with their most pressing operational need.

Why a Functional Taxonomy Matters: Avoiding Apples-to-Oranges Vendor Comparisons

The single most common mistake in supply chain AI vendor evaluation is comparing platforms that serve fundamentally different functions. A demand planning platform like Kinaxis RapidResponse, built for probabilistic forecasting and what-if simulation across multi-echelon networks, cannot be meaningfully compared to a real-time visibility platform like Project44, which tracks shipment-level events across carriers. Both use AI, but they solve different problems, consume different data, and deliver value through different metrics.

The AI supply chain market has fragmented into distinct functional clusters, each with its own dominant vendors, evaluation criteria, and implementation patterns. Treating all "AI supply chain companies" as interchangeable leads to misaligned shortlists, wasted evaluation cycles, and ultimately poor technology decisions.

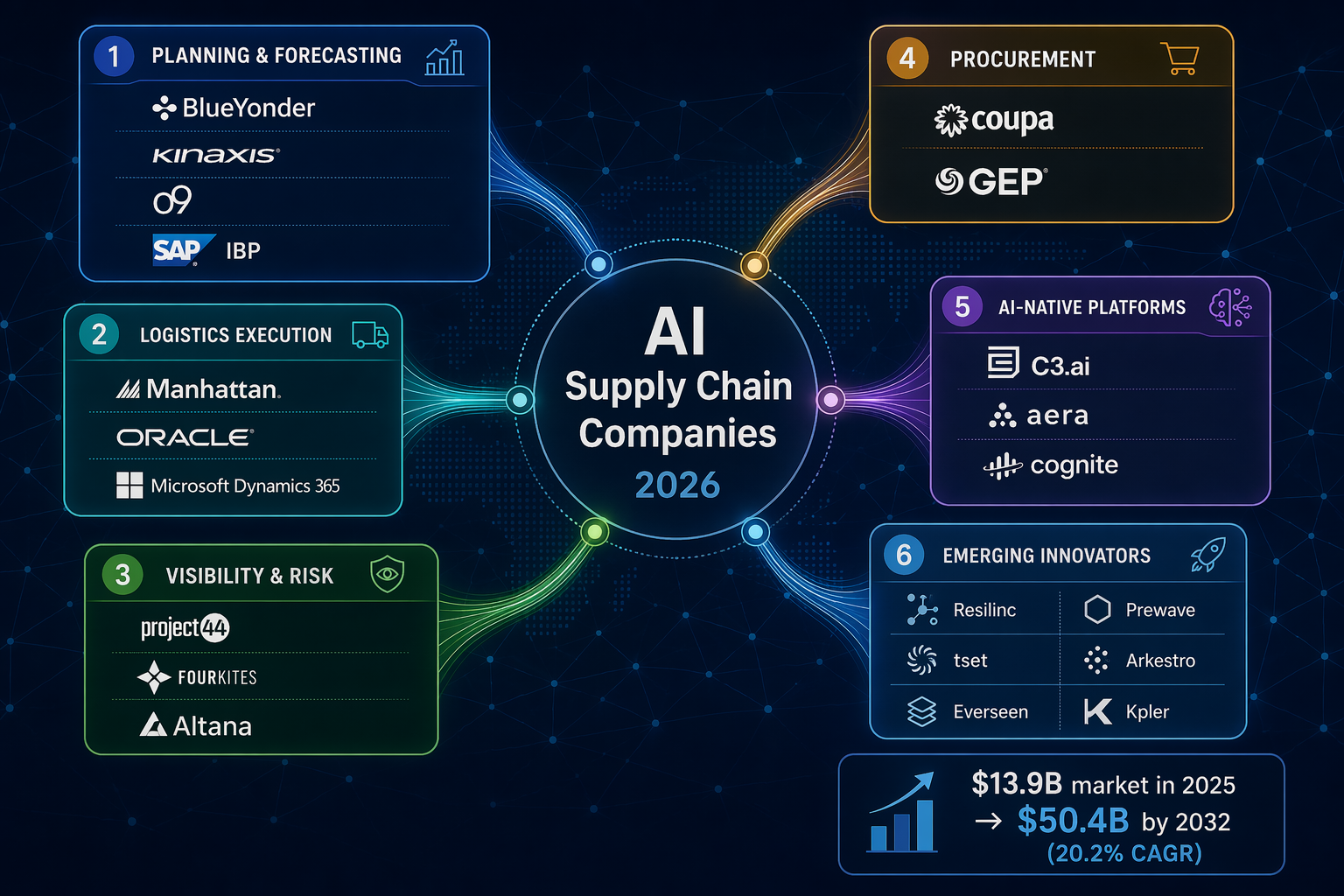

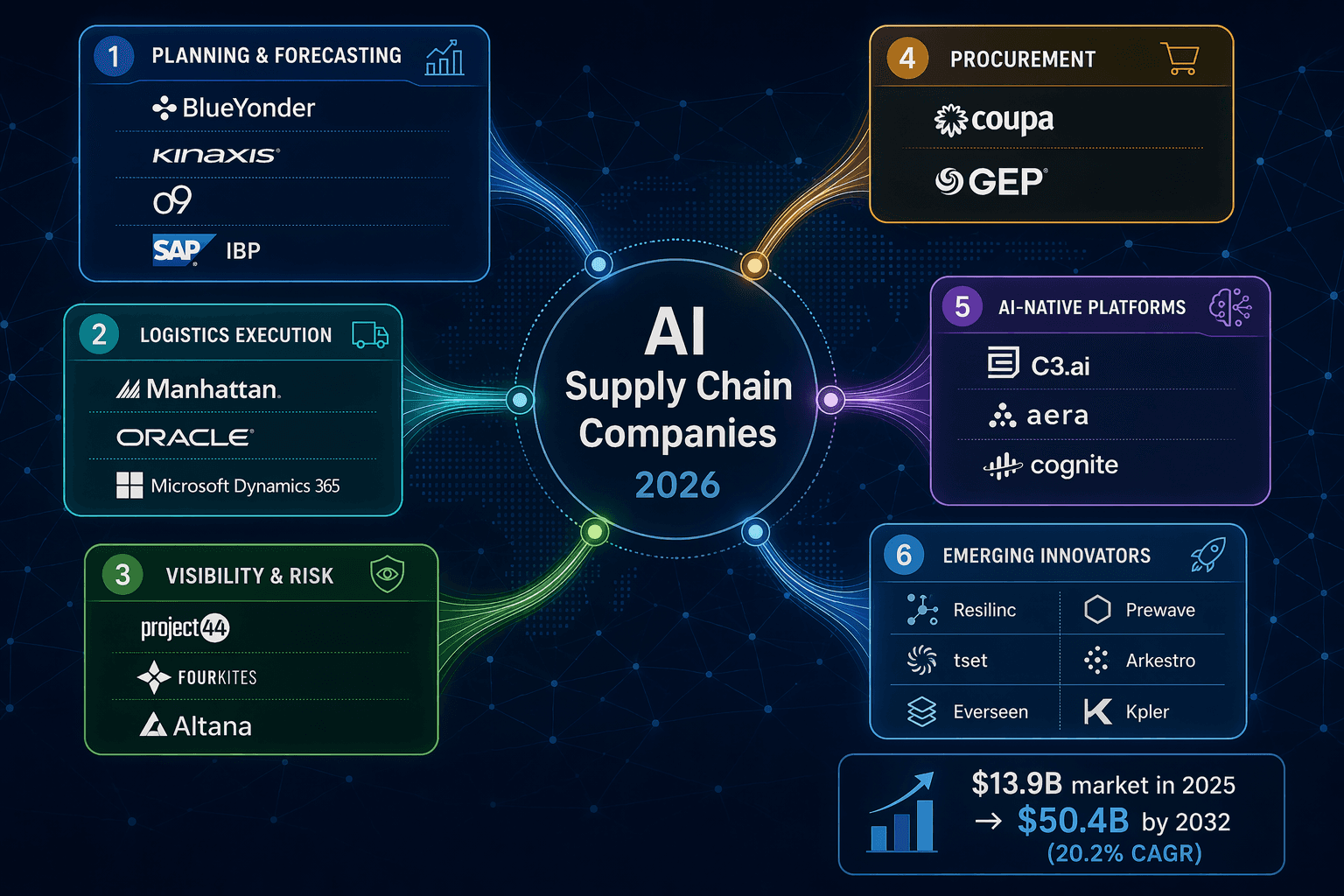

The six-category taxonomy below — Planning & Forecasting, Logistics & Warehouse Execution, Visibility & Risk, Procurement & Spend, AI-Native Platforms, and Emerging Innovators — provides a framework for matching operational needs to the right vendor category before comparing individual products within that category.

Category 1: AI Planning & Forecasting

This category includes the most mature segment of AI supply chain software: platforms purpose-built for demand forecasting, inventory optimization, sales and operations planning (S&OP), and integrated business planning (IBP). These systems ingest historical sales data, promotional calendars, and external demand signals to generate probabilistic forecasts and recommend inventory positioning.

The dominant players in this space are well-established, with deep ERP integrations and large enterprise customer bases. MarketsandMarkets identifies SAP SE, Oracle, and Blue Yonder as "star players" with strong market share and product footprint in the overall AI supply chain market.

Key Vendors in AI Planning & Forecasting

| Vendor | Core AI Methodology | Target Company Size | Key Differentiator |

|---|---|---|---|

| Blue Yonder Luminate | AI-driven planning, control tower | Enterprise | End-to-end suite with strong retail/CPG footprint; partnered with Viva Energy Group (Sept 2025) to deploy AI-powered category management across 1,000+ convenience stores |

| Kinaxis RapidResponse | Real-time concurrent planning, what-if simulation | Enterprise | Single data model for end-to-end visibility; strong in high-tech and automotive |

| o9 Solutions | Digital twin architecture, AI-based demand and supply planning | Enterprise | Platform-native digital twin; strong in complex multi-echelon environments |

| SAP Integrated Business Planning (IBP) | Demand sensing, inventory optimization | Enterprise | Deep SAP S/4HANA integration; natural fit for SAP-centric organizations |

| Logility | AI-powered demand forecasting and inventory optimization | Mid-Market to Enterprise | Strong in process manufacturing and consumer goods |

| John Galt Solutions | AI-driven supply chain planning (Atlas platform) | Mid-Market | Focus on mid-market affordability and speed of deployment |

| RELEX | AI-driven demand forecasting and replenishment | Mid-Market to Enterprise | Strong in grocery and retail; unified platform for forecasting, replenishment, and space planning |

Comments

Join the discussion with an anonymous comment.