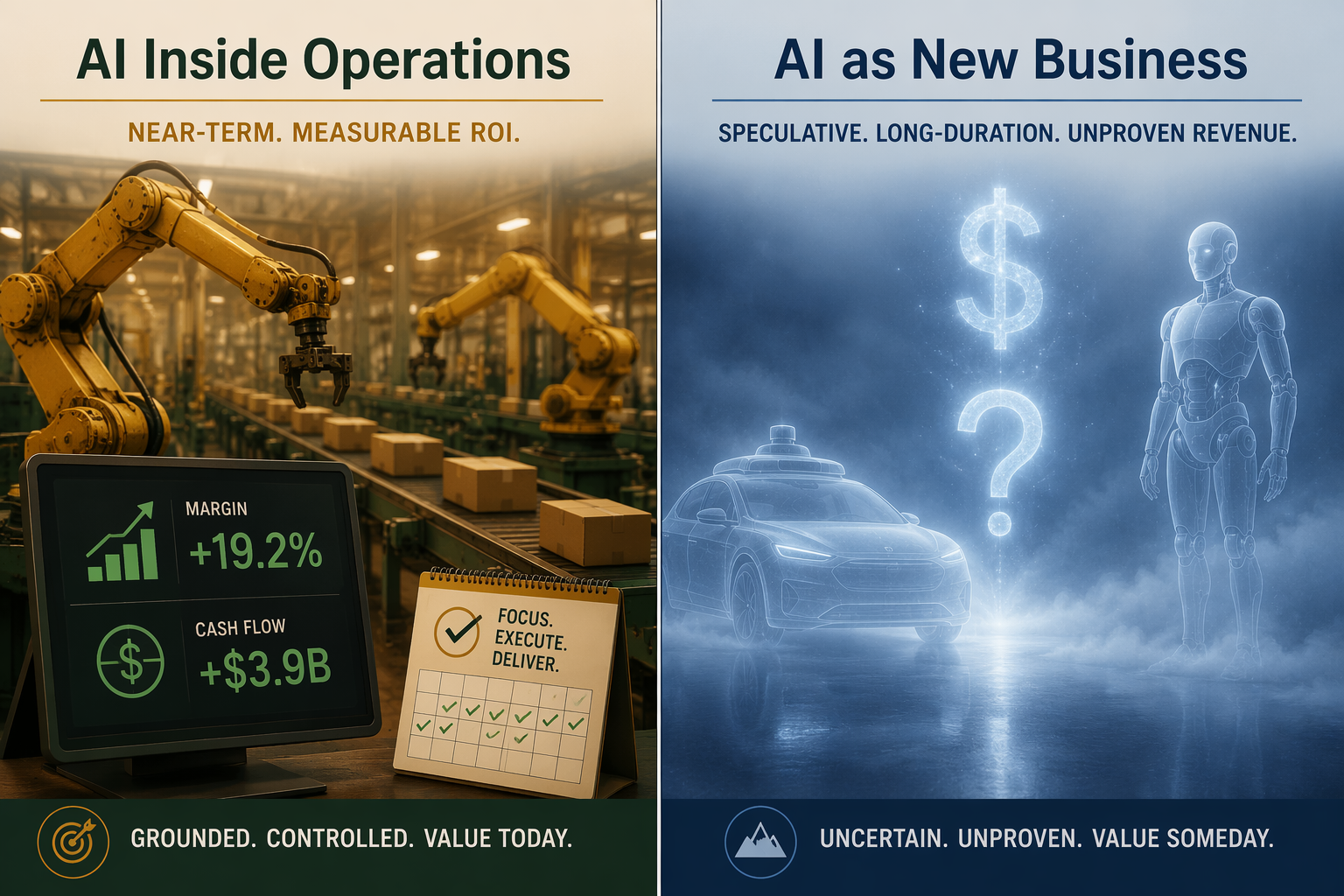

Tesla’s Q1 2026 did not offer the clean story either side usually wants. Automotive gross margin reached 21.1%, or 19.2% excluding regulatory credits, up 478 to 670 basis points year over year depending on the measure used. Operating profit more than doubled to $940 million, and operating cash flow reached $3.9 billion, up 83% year over year.[1][2] Those are not vanity metrics. They are the kind of numbers that make a plant manager, procurement lead, or CFO stop and ask what changed inside the operating system.

Then the same quarter shows the other half of the screen: Tesla produced about 50,000 more vehicles than it delivered, leaving inventory at 27 days of supply, described in one earnings recap as the largest glut in the company’s history.[1] Margin improved while vehicles accumulated. Cash flow strengthened while the delivery side of the system looked less clean. That combination is exactly why Tesla’s AI supply chain manufacturing earnings matter to people outside the Tesla trade. The useful question is not whether Tesla is overvalued in some broad market sense. It is which part of Tesla’s AI story a supply chain leader can responsibly use in an investment case.

The answer starts with a distinction that gets lost quickly in valuation debates. AI inside operations can show up in margin, working capital, labor utilization, uptime, purchasing discipline, and cash conversion. AI as a new business has to show up as revenue, adoption, regulatory clearance, scaled unit economics, and service reliability. Tesla has evidence in the first bucket. Its market capitalization, at roughly $1.5 trillion in July 2026, is also giving it credit for the second bucket before robotaxi and Optimus revenue exists at scale.[3]

The quarter makes operational AI look real

A 670-basis-point improvement in automotive gross margin excluding credits is a meaningful operating event, especially in a market where EV demand is no longer automatically absorbing every unit pushed through the factory.[1][2] Gross margin can move for many reasons: pricing, mix, input costs, depreciation, warranty assumptions, factory utilization, logistics, software attachment, and supplier terms. The important point is narrower than “AI did it.” Tesla’s Q1 numbers show that the manufacturing and supply chain system produced better economics even while demand-side friction was visible.

That is the part worth studying. Supply chain AI is often sold as a planning dashboard, a procurement assistant, or an automation layer whose benefits appear somewhere between “productivity” and “transformation.” Tesla’s Q1 gives a tougher standard: did the system move gross margin, operating profit, cash flow, or inventory? In this case, at least some of the enterprise-level measures moved in the right direction. Operating profit rose 136% to $940 million, and operating cash flow reached $3.9 billion.[1][2]

The inventory number keeps the analysis honest. Producing 50,000 more vehicles than were delivered is not a minor timing footnote when the same discussion is being used to support a premium valuation.[1] If inventory is building, the supply chain has not magically solved the commercial system. It may have lowered unit cost, improved throughput, or released cash from other parts of the cycle, but the end-to-end operating picture still includes vehicles waiting for customers.

For supply chain leaders, that is a familiar tension. A factory improvement program can be successful and still expose a sales-and-operations-planning problem. A purchasing model can reduce input costs and still leave too much finished goods inventory. A labor automation project can improve conversion cost and still fail to fix mix. Tesla’s quarter is useful because it refuses to collapse all of those outcomes into one clean AI victory lap.

Where the evidence is official, and where it is interpretation

The official earnings-level facts support a clear but limited claim: Tesla reported stronger margins, stronger operating cash flow, and higher operating profit in Q1 2026 while carrying a larger inventory position.[1] That is enough to say the operating model improved on several financial measures. It is not enough, by itself, to assign every basis point of improvement to AI.

Some of the more interesting operating mechanisms come from analyst interpretation rather than Tesla’s own formal disclosure. Nitesh Mishra’s LinkedIn analysis, distributed through BingX, describes AI cost-allocation systems that adjust budgets every four hours, lights-out factory sections that reduce labor costs by about 67%, and a negative 12-day cash conversion cycle.[2] Those claims are operationally compelling. They are also not the same kind of evidence as a Tesla shareholder update. A finance team should treat them as hypotheses or external analysis unless they are confirmed in company filings or management commentary.

That distinction matters because the best AI investment cases are not built by borrowing someone else’s narrative. They are built by tracing a mechanism from decision speed to operating result. If an AI model reallocates budget every four hours, the business case needs to show which decision previously waited longer, who acted on the new signal, what spend category changed, and whether the result appears in purchase price variance, expedite cost, overtime, obsolescence, or working capital. Without that bridge, “AI cost allocation” is a description, not an ROI case.

The lights-out claim deserves the same discipline. A 67% labor-cost reduction in a section of a factory would be significant if verified, but it would still need boundaries: which section, which labor pool, what volume, what quality escape rate, what maintenance burden, and what depreciation load.[2] A partially automated area can be an excellent investment without proving that the whole factory, much less the whole enterprise, deserves an AI platform multiple.

This is where Tesla is more useful as a measurement lesson than as a template. The operating indicators that matter are not exotic. They are gross margin excluding credits, operating cash flow, inventory days, production-to-delivery spread, subscription revenue mix, capex intensity, and cash conversion. ChainSignal’s work on the supply chain AI ROI measurement gap reaches a similar practical point: productivity claims are not enough unless they land in the P&L, balance sheet, or service metrics that capital committees already trust.

FSD changes the margin mix without solving the volume question

Full Self-Driving complicates the Q1 read because it shifts part of the automotive business toward recurring software economics. Tesla had 1.28 million paid FSD subscribers, up 51% year over year, and moved to a subscription-only model in February 2026, according to the earnings recap and related analysis.[1][2] Recurring software income can lift margin even if unit delivery growth is less impressive. That is a real business-model change, not just a story about autonomy.

For an automotive manufacturer, high-margin software attached to the installed base can make the income statement less dependent on the next physical unit. For a supply chain executive, the lesson is more general: AI-enabled software revenue and AI-enabled operating savings should be measured separately. One improves the economics of units already in the system. The other may create a revenue stream that behaves differently from manufacturing throughput.

But FSD subscription growth does not erase the 50,000-unit production-delivery gap.[1] A software mix shift can improve gross margin while finished goods still build. That is not a contradiction; it is the operating reality of a company straddling manufacturing, software, and future mobility services. It also means supply chain teams should avoid using margin improvement alone as proof that demand, inventory, and service-network constraints have been solved.

| Metric or claim | What it can support | What it cannot support by itself |

|---|---|---|

| Automotive gross margin ex-credits of 19.2% | Operational economics improved in Q1 2026 | All improvement came from AI |

| Operating cash flow of $3.9B | The business converted operations into cash more effectively in the quarter | Future AI businesses are already de-risked |

| 50,000 more vehicles produced than delivered | Demand, mix, timing, or channel friction still matters | Manufacturing efficiency is irrelevant |

| 1.28M paid FSD subscribers | Software mix is becoming more material | Robotaxi revenue exists at scale |

| Analyst claims about four-hour budget allocation and lights-out sections | Possible mechanisms to investigate | Tesla-confirmed operating facts |

The capex bill belongs to a different risk category

The valuation debate changes once the discussion moves from Q1 operating gains to Tesla’s 2026 capital plan. Analyst previews and reporting point to more than $25 billion of 2026 capex, compared with $8.5 billion in 2025, funding six new factories, Terafab, Cortex 2 with 230,000 H100-equivalent GPUs, Optimus production lines, and a Cybercab pilot.[3] Reuters and Yahoo Finance also reported the 2026 capex guidance.[4][5] That is not a normal efficiency-program budget. It is a platform-building budget.

A plant-level AI project can often be evaluated within quarters: did scrap fall, did labor hours per unit improve, did changeover time shrink, did inventory turns improve, did premium freight decline? A $25 billion-plus capex program aimed at factories, AI infrastructure, robotaxis, and humanoid robots has a longer and less forgiving evidence chain. It has to pass through construction, commissioning, supplier readiness, model performance, regulation, production ramp, customer adoption, service economics, and competitive response before it earns the revenue multiple already implied by the market.

That does not make the spend irrational. Tesla’s strategy has long depended on integrating hard assets and software closer than most automakers would attempt. The issue is timing and proof. If the capex is justified by lower manufacturing cost, the supporting metrics should look like cost per unit, yield, depreciation per unit, labor utilization, warranty rates, and throughput. If the capex is justified by robotaxi or Optimus revenue, the supporting metrics have to move toward fleet utilization, regulatory authorization, robot unit cost, field reliability, attach rates, and paid usage. Those are different underwriting files.

The market is already blending those files. Baptista Research’s Q2 2026 preview cited Tesla trading around 135 times last-twelve-month EBITDA and 373 times last-twelve-month diluted earnings as of July 9, 2026.[3] Multiples like that are not explained by current automotive earnings alone. They reflect expectations for future AI, robotaxi, Optimus, and related revenue streams.

Analyst disagreement is a map of the missing proof

The spread among analysts is not just a disagreement about a target price. It is a disagreement about how much credit to give Tesla before the new revenue categories scale. Baptista Research cited JPMorgan at a $475 target with a Neutral view, Morgan Stanley at $415, Wedbush at $600 with a bullish view, and GLJ Research modeling $83.4 billion of revenue, about 30% below consensus.[3] The point is not that one house has the correct number. It is that reasonable models diverge sharply once robotaxi, Optimus, and AI infrastructure become central to the valuation.

That divergence should feel familiar to anyone who has taken a large automation request to an investment committee. The base case may be supported by scrap reduction, material savings, and labor redeployment. The upside case may include new service revenue, pricing power, or market share gains. The problem starts when the upside case is treated as if it has the same evidentiary status as a measured cost takeout.

Tesla’s valuation gives the upside case enormous weight. A supply chain leader should not copy that weighting into an internal AI proposal. Public equity markets can wait years, reprice narratives daily, and tolerate wide dispersion in outcomes. A manufacturing or supply chain capex request usually has to compete with tooling, capacity, quality, resilience, and working-capital projects that have nearer payback and clearer accountability.

This is why the distinction between operational AI ROI and new-business AI ROI is not academic. ChainSignal’s benchmarks on realistic AI ROI timelines are a useful counterweight to Tesla exceptionalism: most companies should not expect every AI program to behave like a high-conviction public-market narrative. The right timeline depends on whether the program is improving an existing process or trying to create a new revenue category.

Execution risk is not a footnote to vertical integration

Tesla’s vertical integration is part of what makes its operating AI story interesting. The company has pursued deep integration across vehicles, batteries, software, robotics, and manufacturing systems, with outside analysis describing 80% to 87% vertical integration and pointing to the lithium refinery opened in January 2026 as another step in that direction.[6] The logic is straightforward: the more of the system Tesla controls, the more places it can instrument, optimize, and redesign.

Control also concentrates execution risk. The 4680 battery program has faced production delays, and the lithium refinery is too new to judge on ROI.[6] Tesla disbanded the Dojo project in August 2025 and restarted it in January 2026, which shows that even the AI infrastructure roadmap is iterative rather than settled.[3] AI5 chip plans add another layer: reporting and analysis have pointed to supply involving TSMC and Samsung, while Tesla’s Q4 call coverage emphasized the AI5 chip as part of the next infrastructure push.[7][8]

None of that invalidates the strategy. It does mean the path from vertical integration to scaled AI revenue is not automatic. Every additional layer — battery chemistry, chip supply, factory automation, robotics components, model training, fleet operations — creates both a coordination advantage and a failure point. That is usually how ambitious manufacturing systems work. The slides get cleaner as the system gets harder.

The Optimus supply chain illustrates the point without needing a science-fiction detour. Motley Fool coverage of Tesla’s Q3 earnings call highlighted the roughly 10,000-component challenge in the humanoid robot supply chain.[9] That is not just a procurement statistic. It means supplier qualification, design changes, quality control, component availability, cost-down work, and production learning curves all have to line up before Optimus becomes a scaled business rather than a strategic option.

The discontinued Model S and Model X, reported by Business Insider and the BBC, belong in the same execution-risk file.[1][10] They show that Tesla is willing to simplify the vehicle portfolio as it shifts attention toward robots and AI. That may be strategically coherent. It also reminds capital allocators that every pivot has an opportunity cost, especially when the mature automotive business is still carrying the cash-generation burden.

What a supply chain leader can actually take from Tesla

The most useful takeaway from Tesla’s Q1 is not “spend like Tesla.” It is to separate the evidence by economic type before asking for money. AI inside operations deserves to be judged on operational and financial measures that can move within the existing business. AI as a new business deserves a longer timeline, a higher uncertainty band, and a different proof package.

- For AI inside operations, require traceability to margin, conversion cost, inventory days, service level, yield, premium freight, planning latency, procurement savings, or cash conversion.

- For AI as new business, require evidence of customer adoption, revenue conversion, regulatory readiness, field reliability, unit economics, and the operating model needed to scale.

- For analyst or vendor claims, label them separately from company-confirmed results and do not let them carry the base case.

- For capex requests, keep the near-term productivity case separate from the strategic-option value, even when both depend on the same data and infrastructure.

Tesla’s Q1 operating results support the argument that AI-enabled manufacturing and supply chain systems can produce measurable gains within quarters. They do not prove that every large AI infrastructure program should receive valuation credit for future business models before those businesses have revenue at scale. If the AI program improves today’s operating system, underwrite it with today’s operating metrics. If it creates a new business, underwrite it like a new business. Tesla may eventually justify more of the premium now embedded in its valuation, but its Q1 2026 earnings already offer a cleaner lesson: operational AI earns credibility when it can be followed into margin, cash, inventory, and labor economics. Speculative AI earns credibility later.

References

- Tesla Earnings Recap: Musk Braces Investors for Spending Increase, Business Insider

- Tesla Q1 2026 Earnings: Profit Structure Shifts, BingX / Nitesh Mishra

- Tesla Q2 Earnings: Robotaxis, Optimus & The AI Reality Check, Baptista Research

- 2026 capex guidance confirmation, Reuters

- 2026 capex guidance confirmation, Yahoo Finance

- What Tesla Reveals About Vertical Integration in Supply Chains, Logistics Viewpoints

- Tesla Turns Vertical Integration Into AI and Robotics Advantage, Supplychain360.io

- 6 Biggest Takeaways From Tesla's Q4 Earnings Call, Business Insider, Jan 2026

- Tesla Optimus Humanoid Robot: Key Takeaways From the Q3 Earnings Call, Motley Fool

- Tesla cuts car models in shift to robots and AI, BBC

Comments

Join the discussion with an anonymous comment.