The useful thing about Tesla’s analyst spread is not that it is dramatic. It is that it forces a cleaner question than most AI strategy decks do: which parts of the Tesla AI supply chain story have already produced operating evidence, and which parts are still being capitalized as future scale?

As of July 17, 2026, Public.com showed a 26-analyst consensus rating of Hold at roughly $421, with price targets ranging from GLJ Research at $24.86 to Wedbush at $600, the widest target spread among Magnificent Seven stocks.[1] That gap is too large to dismiss as routine model noise. It is a public record of disagreement over what counts as evidence.

On one side are items that look like production returns: FSD subscriptions, recurring software revenue, energy storage revenue and margins, and any confirmed manufacturing cost reduction. On the other side are items that may be strategically important but still depend on timing, utilization, regulation, production learning curves, and customer adoption: Optimus, robotaxi, Cybercab, and the capital ramp behind them.

That distinction matters outside Tesla. Supply chain leaders evaluating AI vendors face the same problem in smaller form. A demo can make a future operating model feel inevitable. A capital request has to survive a different room: finance asking what has already changed in production, operations asking who will own the exception process, and IT asking whether the roadmap depends on integrations that have not been built.

What Each Side Is Treating as Real

The bull case is not just “AI will be big.” The stronger version is that Tesla has several assets already positioned to convert hardware into software, energy, and autonomy economics. Wedbush’s Dan Ives, whose $600 target sits at the top of the cited range, argues that Tesla could own about 70% of the global autonomous market over the next decade and that FSD subscriptions reposition the vehicle as a delivery mechanism for software revenue.[2] That is a forecast, not a production result, but it rests partly on an existing installed base and a subscription motion that can be tracked.

The bear case is not just “Tesla is expensive.” JPMorgan, UBS, and Wells Fargo targets cited in the research range from $130 to $247, with the common concern that a large 2026 capex program is funding AI, Optimus, robotaxi, and chip-fab build-out before those projects generate enough near-term revenue to defend the valuation.[3] Forbes separately framed the pressure around weakening core automotive signals, including Tesla’s U.S. EV market share falling from 80% in 2019 to 43.9% in 2025 and a 373x P/E ratio that is difficult to reconcile with conventional earnings support.[4]

| AI-related bet | What supporters cite | What skeptics question | Operational status |

|---|---|---|---|

| FSD subscriptions | 1.28M subscribers, up 51% year over year, and a recurring software-revenue path tied to the vehicle base.[2] | Whether subscription growth proves durable autonomy economics or mainly monetizes today’s assisted-driving customer base. | Production evidence exists, but broader valuation depends on how much of that revenue converts into scalable autonomy value. |

| Energy storage | $12.8B in 2025 revenue, up 26.6% year over year, with roughly 30% gross margins; Q4 revenue was $3.84B, up 25% year over year.[5] | Whether energy storage can carry enough profit weight if automotive margins and EV share weaken. | The cleanest non-automotive production ROI signal in the available materials. |

| Manufacturing efficiency | A LinkedIn-sourced earnings preview claims cost per vehicle fell 31% year over year in Q2 2026. | The figure is not confirmed by Tesla’s official Q2 release, which is scheduled for July 22, 2026. | Potentially important, but it should remain provisional until official filings confirm or contradict it. |

| Optimus | A production start is targeted for July/August 2026, and bulls treat humanoid robotics as a major future platform. | Current revenue is $0, and the project remains in R&D rather than scaled production. | Strategic optionality, not current ROI. |

| Robotaxi | Bullish models assign large value to autonomy, with Wedbush seeing $1T in autonomous value.[2] | Fleet counts vary by operating definition: about 500 vehicles with safety drivers versus roughly 20-50 fully driverless vehicles on road.[4] | Real-world testing is underway, but economics depend on driverless utilization, regulation, safety performance, and service density. |

| Cybercab | Production began in April 2026, making it more than a concept in the cited timeline. | Elon Musk warned output would be “agonizingly slow” initially.[4] | Early production signal, not yet a scaled cost or utilization case. |

| $25B capex ramp | Piper Sandler called the capex rise surprising but necessary for AI, Optimus, robotaxi, and chip-fab build-out.[3] | With only $2.49B spent in Q1, the full-year guide implies a steep ramp in later quarters, creating lumpy cash-flow risk.[3] | A capital-allocation bet whose payoff depends on multiple future programs arriving close enough to plan. |

The Production ROI Side of the Ledger

FSD subscriptions are the most direct bridge between Tesla’s installed vehicle base and the AI margin story. The cited 1.28M subscribers and 51% year-over-year growth are not the same as proof that full autonomy has arrived, but they do show customers paying for a software layer after the vehicle sale.[2] For a supply chain executive, that distinction is familiar: adoption of a paid module is evidence; proof that the module transforms the whole operating model is a higher bar.

This is why the phrase “delivery mechanism” matters in the Wedbush thesis. If the vehicle becomes a software revenue channel, the supply chain question changes from unit delivery alone to lifecycle monetization, update cadence, retention, and feature attach. The evidence available today supports the existence of a recurring revenue stream. It does not, by itself, settle the market-share claim that Tesla will own about 70% of global autonomy over the next decade.[2]

Energy storage is cleaner. RoboForex’s analysis of Tesla financials identifies the storage business as producing $12.8B in 2025 revenue, up 26.6% year over year, with gross margins around 30%.[5] It also cites Q4 energy storage revenue of $3.84B, up 25% year over year, at similar margin levels.[5] Among the AI-adjacent and non-automotive themes in the materials, this is the closest thing to an operating segment with visible unit economics at scale.

That does not make energy storage an AI proof point in the narrow model-demo sense. It makes it a supply chain proof point: production, deployment, revenue recognition, margin, and repeatability can be analyzed without waiting for a regulatory breakthrough. If an investment committee is trying to distinguish operating traction from narrative extension, this category deserves different treatment from robot fleets and humanoid labor substitution.

Manufacturing efficiency would belong in the same production-return bucket if the Q2 2026 figure holds. A 31% year-over-year reduction in cost per vehicle would be a material operating signal, especially for a company whose AI story is often tied to factory learning, vertical integration, and software-defined operations. But the available figure comes from a LinkedIn-sourced earnings preview, not Tesla’s official filing. Until the July 22, 2026 earnings release confirms or contradicts it, the right treatment is provisional: important enough to monitor, not solid enough to underwrite.

Vertical integration is part of why Tesla keeps drawing this kind of operating scrutiny. Logistics Viewpoints argues that Tesla’s supply chain model gives it unusual control across hardware, software, manufacturing, and data feedback loops.[6] That control can shorten learning cycles when the system works. It can also concentrate execution risk when several capital-heavy programs need to scale at once.

Where the Capitalized Promise Begins

Optimus, robotaxi, and Cybercab should not be waved away as fantasies. Tesla has a record of making operational bets that looked unreasonable before competitors had to respond. The mistake is different: treating projects with unresolved production economics as if they deserve the same discount rate as businesses already producing revenue and margin.

Optimus is the clearest example. The project is assigned strategic value because humanoid robots could change labor availability, factory task design, and eventually the cost structure of physical operations. But in the available materials, Optimus has $0 revenue and remains in R&D, with production targeted for July/August 2026. That is not a negative verdict. It is a category label. A project can be strategically serious and still not be production ROI.

Robotaxi sits in a more complicated middle. The fleet-size discrepancy often sounds like a contradiction, but it is better understood as two different operating definitions. One figure refers to roughly 500 vehicles in testing with safety drivers; the other refers to about 20-50 fully driverless vehicles on road.[4] Those are not interchangeable. A vehicle with a safety driver can produce route, perception, intervention, and operational data. A fully driverless vehicle begins to test the economics that matter for a commercial service: utilization, remote support, cleaning, charging, incident response, insurance, local regulation, and customer wait times.

Cybercab adds another timing issue. Forbes reported that production began in April 2026, while also noting Musk’s warning that output would be “agonizingly slow” at first.[4] For valuation work, those two facts pull in opposite directions. Production start reduces concept risk. Slow ramp preserves execution risk. A supply chain leader would recognize the pattern immediately: first units are not the same as stable takt time, qualified suppliers, predictable service levels, or repeatable cost.

The $25B capex plan is where these bets meet the cash-flow model. Yahoo Finance reported Piper Sandler’s view that the capex rise was surprising but necessary for AI, Optimus, robotaxi, and chip-fab build-out.[3] The same setup gives skeptics room to object: with $2.49B spent in Q1, reaching the full-year guidance requires a steep ramp in later quarters, which can make free-cash-flow forecasts highly sensitive to timing.[3] A quarter or two of slippage may not break a long-term platform thesis, but it can break the payback story attached to a near-term capital request.

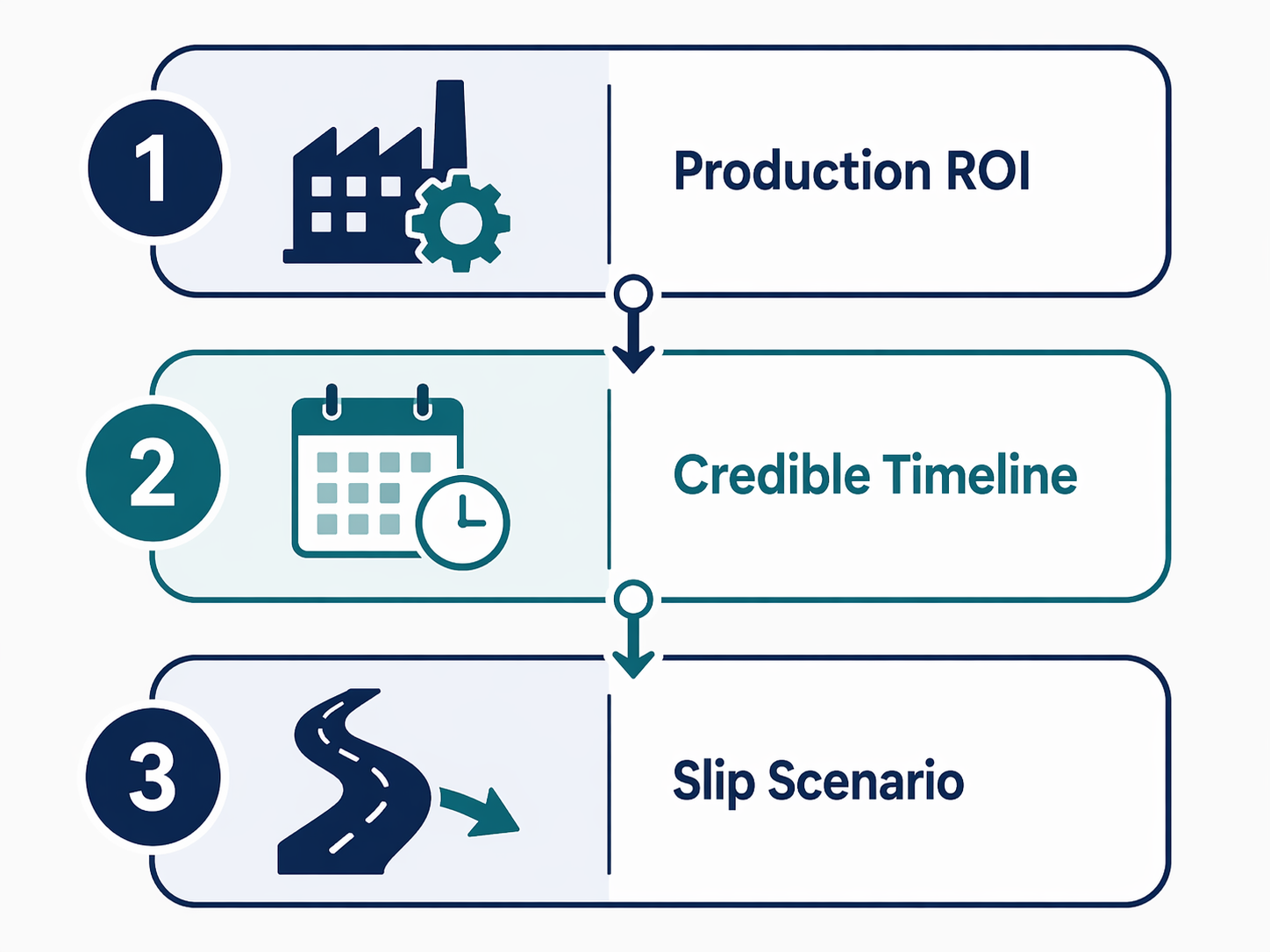

The Three Questions Supply Chain Teams Can Reuse

Tesla is an unusually public case, but the discipline transfers well to ordinary AI vendor evaluation. The point is not to reject speculative bets. The point is to stop mixing evidence types inside one blended ROI story.

Has the use case produced measurable ROI in production?

For Tesla, FSD subscriptions and energy storage margins belong closer to this category than Optimus does. The evidence is not equally strong across both. FSD subscription growth shows paid adoption of software, while energy storage shows revenue and margin at segment scale.[2][5] A procurement team should make the same separation when a vendor combines a deployed forecasting module, a pilot warehouse optimizer, and a future autonomous planning agent in one pitch.

The practical test is simple: ask what changed in production, who measured it, and whether the gain appears in a system of record that finance already trusts. Reduced expedites, lower inventory, fewer stockouts, faster planning cycles, higher asset utilization, or lower labor hours are different from user enthusiasm after a pilot. Both may matter. Only one can usually carry the first-year business case.

What is the credible timeline to scale?

The Tesla analyst divide becomes sharper when timelines enter the model. A forecast that Tesla captures a dominant share of global autonomy over the next decade is a different claim from a count of paying FSD subscribers today.[2] A production target for Optimus in July/August 2026 is different from evidence that humanoid robots are already lowering factory cost. Cybercab production beginning in April 2026 is different from a scaled fleet with known utilization and maintenance economics.[4]

Vendor reviews should force the same calendar discipline. If a supplier says the AI system will move from planning assistance to autonomous execution, the timeline should specify integration dependencies, data-quality prerequisites, exception ownership, user adoption gates, and the point at which the old process can actually be retired. A roadmap that cannot say which manual step disappears, and when, is not yet a scale plan.

What happens if the timeline slips?

This is the question that often gets postponed until after the purchase order. Tesla’s $25B capex thesis is sensitive to slip scenarios because several programs are capital intensive before they are revenue mature.[3] If robotaxi scale, Optimus production, or Cybercab output arrives later than expected, the long-term option value may still exist, but the interim cash-flow profile changes.

For an enterprise AI buyer, the same issue appears as subscription commitments, integration spending, process redesign, and internal credibility. If the vendor roadmap slips by two quarters, does the business still receive value from the deployed module? Can the contract step down? Does the team have a manual fallback? Does the CFO know which savings are confirmed and which require the next release? These questions are not pessimistic. They are how ambitious bets avoid being mispriced as completed deployments.

Why the Analyst Divide Is Useful

Investing.com’s framing is directionally right: Tesla’s valuation now hinges on AI, energy, and robotaxi scale more than EV sales alone.[7] That is exactly why the evidence has to be disaggregated. Energy storage margins should not be argued with the same verbs as Optimus. FSD subscriptions should not be treated as proof of robotaxi economics. A safety-driver test fleet should not be counted like a fully driverless commercial fleet.

The supply chain lesson is not that bold AI bets are bad. Tesla’s entire operating history makes that too easy a conclusion. The better lesson is that current operating returns and future platform optionality deserve different prices, different milestones, and different failure plans.

That is why Tesla’s analyst divide is useful even for leaders who will never buy or sell a share. It turns a noisy market argument into a practical investment habit: separate what is already measurable in production from what still depends on a credible scale timeline, then define the slip scenario before capital is committed.

References

- Tesla (TSLA) Stock Forecast: Analyst Ratings, Predictions & Price Target 2026 — Public.com, July 17, 2026

- How The Tesla (TSLA) Narrative Is Shifting With AI Ambitions And Mixed Analyst Targets — Yahoo Finance

- Tesla Q1 analyst reaction: Capex rise a surprise but needed for AI, Optimus, robotaxi, chip fab build-out — Yahoo Finance

- Tesla Stock Could Sink In The Last Half Of 2026—Here's Why — Forbes, July 16, 2026

- Tesla, Inc. (TSLA) stock analysis and forecast for 2026 — RoboForex

- What Tesla Reveals About Vertical Integration in Supply Chains — Logistics Viewpoints

- Tesla Valuation Hinges on AI, Energy, and Robotaxi Scale More Than EV Sales — Investing.com

Comments

Join the discussion with an anonymous comment.