About the MHI 2025 Annual Industry Report

The MHI 2025 Annual Industry Report — formally titled The Digital Supply Chain Ecosystem: Orchestrating End-to-End Solutions — is the 12th edition of the annual series produced jointly by MHI and Deloitte. It was released on March 19, 2025, at ProMat in Chicago, and represents the most methodologically substantial edition of the series to date.

The survey base matters for any practitioner using this data to benchmark their own organization. Responses came from more than 700 manufacturing and supply chain industry leaders, with 83% holding executive-level positions. Fifty-three percent of respondents reported annual revenues above $50 million, and 21% above $1 billion. That profile makes this a peer dataset for mid-to-large enterprises — not a startup or SMB sample — which directly affects how the adoption rates should be interpreted.

| Report Attribute | Detail |

|---|---|

| Edition | 12th Annual (2025) |

| Produced by | MHI in collaboration with Deloitte |

| Release date | March 19, 2025 (ProMat, Chicago) |

| Respondents | 700+ manufacturing and supply chain leaders |

| Executive-level respondents | 83% |

| Companies with $50M+ annual revenue | 53% |

| Companies with $1B+ annual revenue | 21% |

| Technologies tracked | 11 |

| Survey timing | Late 2024 |

The 28%-to-82% Gap: What the Adoption Curve Actually Signals

Of all 11 technologies MHI tracks in its annual series, AI carries the largest single adoption trajectory: 28% of supply chain leaders report using AI today, while 82% expect to use it within five years. That 54-percentage-point projected increase is not matched by any other technology in the report. For warehouse directors evaluating whether to move now or wait, the steepness of that curve is the most operationally significant data point in the entire report.

The instinct to read this as a hype signal — another technology with inflated expectations — is understandable. But MHI CEO John Paxton's own framing cuts against that interpretation. Rather than celebrating the 82% projection, Paxton identified the knowledge gap behind the low current adoption number as the central problem the industry needs to solve.

Supply chain leaders told us they don't yet understand how to apply the AI to their operations, which makes it difficult to build a business case for the investment. — John Paxton, CEO, MHI (MHI 2025 Annual Industry Report)

That statement reframes the 28% figure. The 72% of leaders not yet using AI are not simply laggards waiting for the right moment — many of them are stuck at the business case stage because they cannot articulate what problem AI would solve in their specific operation or what a credible ROI estimate looks like. The curve's steepness means that window for deliberation is compressing.

The Technology Priority Ladder: Where AI Sits and Why It Matters

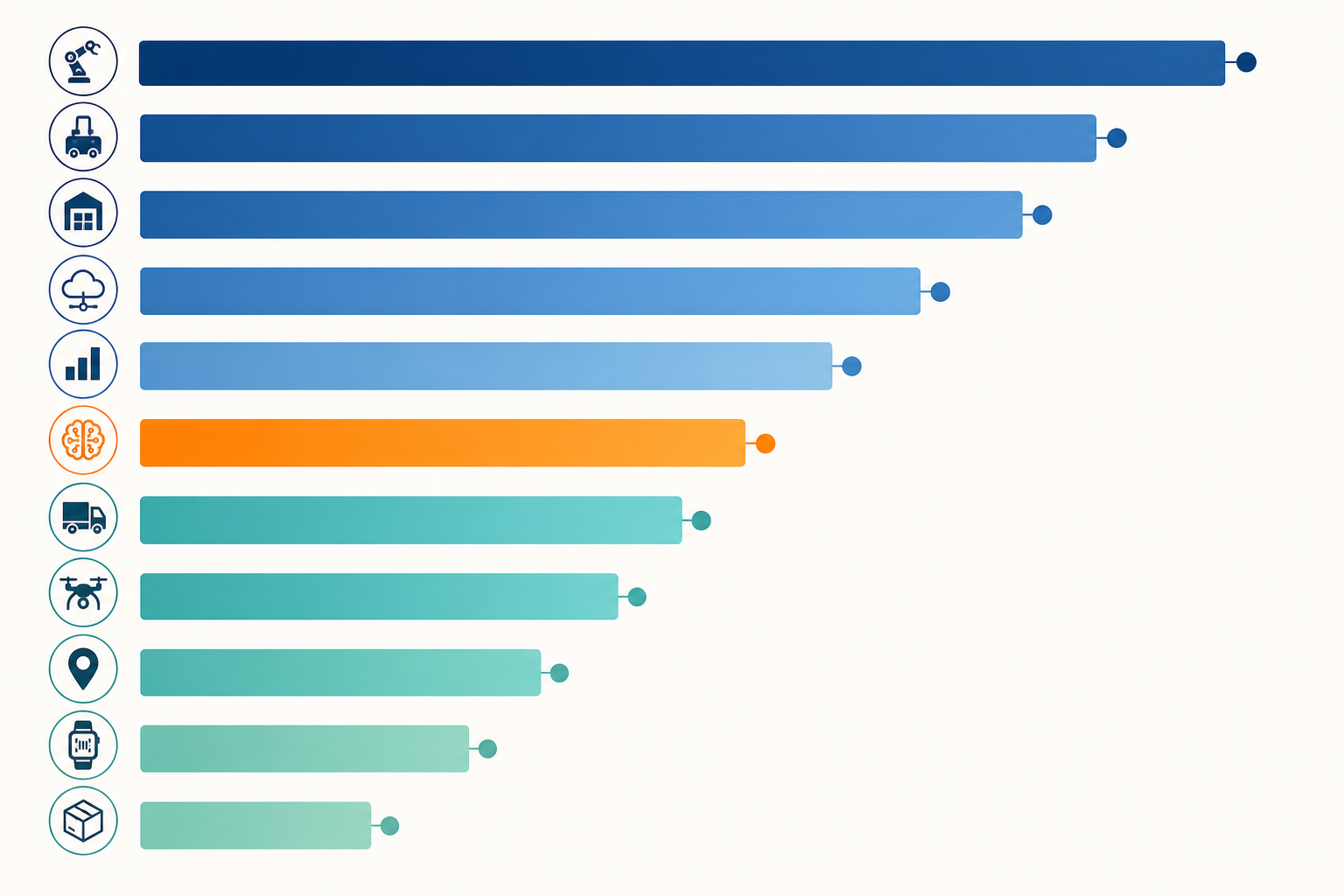

AI's 82% five-year adoption projection places it sixth in the full ranking of 11 technologies. That placement is often misread as evidence that AI is a secondary priority. The actual picture is more nuanced — and more important for warehouse leaders to understand.

| Technology | 5-Year Adoption Projection | Layer Type |

|---|---|---|

| Inventory and Network Optimization | 92% | Infrastructure / AI-embedded |

| Cloud Computing and Storage | 91% | Infrastructure / AI-embedded |

| Sensors and Automatic Identification | 88% | Infrastructure / AI-embedded |

| Predictive Analytics | 87% | AI-adjacent / often AI-powered |

| Robotics and Automation | 83% | Physical automation |

| Artificial Intelligence | 82% | Standalone AI capability |

| Internet of Things (IoT) | 77% | Data collection layer |

| Wearable and Mobile Technology | 72% | Operational interface |

| Autonomous Vehicles and Drones | 64% | Physical automation |

| 3D Printing / Additive Manufacturing | 57% | Manufacturing capability |

| Blockchain | 54% | Data integrity / traceability |

The critical editorial insight from this ranking is what the top three categories represent. Inventory and Network Optimization (92%), Cloud Computing (91%), and Sensors and Automatic Identification (88%) are not competing with AI — they are the infrastructure layers that AI increasingly runs on top of. When a warehouse deploys an AI-driven inventory optimization platform, it registers in the Inventory and Network Optimization category, not necessarily in the standalone AI category.

This explains why AI's five-year projection appears high even while its current standalone adoption is low. AI capability is already diffusing through embedded platforms — demand planning tools, WMS systems, and optimization engines — that respondents may not identify as 'AI deployments' in the traditional sense. The implication for warehouse leaders: the question is not only whether to invest in AI as a discrete tool, but whether the platforms already in use are delivering AI-driven outcomes.

Warehouse-Specific AI Use Cases Gaining Traction

The MHI 2025 report does not treat AI as a monolithic capability. John Paxton specifically named four use case categories as the primary areas where agentic AI is showing near-term relevance for warehouse operations. These are the report's own framing — not editorial extrapolation.

- Agentic process automation. AI agents that execute multi-step warehouse workflows — order picking sequencing, exception handling, replenishment triggering — without requiring human initiation at each step. The operational value is throughput consistency during high-volume periods when manual coordination breaks down.

- Real-time inventory visibility. AI systems that synthesize sensor data, RFID reads, and transaction logs to maintain a continuously accurate inventory position — not a snapshot updated on cycle count schedules. For operations running omnichannel fulfillment, the accuracy gap between periodic and real-time visibility directly affects order promising reliability.

- Predictive maintenance. Machine learning models trained on equipment sensor data to identify failure signatures before they cause downtime. In high-throughput distribution centers, unplanned conveyor or sortation system failures carry disproportionate operational cost relative to the equipment value itself.

- Demand forecasting. AI-driven forecast models that incorporate external signals — weather, promotional calendars, regional economic indicators — alongside historical demand patterns. The warehouse-specific application is labor and dock planning: more accurate short-horizon forecasts translate directly to staffing efficiency and inbound scheduling.

Investment Signals: What Budget Data Reveals About Adoption Readiness

The MHI 2025 report's investment data tells a more complicated story than the headline suggests. The sharp decline in average annual spending — from $26 million in 2023 to $13 million in 2024 — initially reads as a retreat. Deloitte's Wanda Johnson provided the necessary context.

The $13 million figure represents a return to pre-pandemic investment levels — Deloitte's Wanda Johnson noted that average supply chain technology spending in 2019 was approximately $14 million. The 2023 peak reflected pandemic-era catch-up investment, not a new baseline.

Against that normalized baseline, the forward-looking investment signals are directionally positive. Fifty-five percent of supply chain leaders report increasing their technology budgets. Sixty percent plan to spend over $1 million on supply chain technology in the coming year, and 19% plan to spend over $10 million — figures that indicate committed capital allocation, not exploratory interest.

| Investment Signal | 2025 Data Point |

|---|---|

| Leaders increasing tech budgets | 55% |

| Planning to spend over $1M | 60% |

| Planning to spend over $10M | 19% |

| Average annual spend (2024) | $13M (normalized from $26M in 2023) |

| Pre-pandemic baseline (2019) | ~$14M (Deloitte reference point) |

| Planning automation equipment purchases within 3 years | 45% |

The 45% planning to purchase automation equipment — specifically naming AGVs, AS/RS systems, and robotics — within three years is a warehouse-specific signal worth isolating. Physical automation equipment purchases represent committed capital, not software subscription intent. When nearly half of the respondent base is planning physical automation investment within a defined timeframe, it indicates that the warehouse automation cycle is entering a deployment phase, not an evaluation phase.

Barriers Anatomy: Why Most Leaders Cannot Build an AI Business Case

The adoption barriers documented in the MHI 2025 report are not a checklist of problems to solve sequentially. They form a system where one barrier reinforces another — and understanding the system is more useful than treating each barrier as an independent obstacle.

The root constraint, per Paxton's direct statement, is comprehension: leaders cannot articulate what AI would do in their specific operation. That comprehension gap then cascades into the other barriers in a predictable sequence.

- Unclear use cases. Without a specific, bounded problem definition — 'reduce unplanned downtime on conveyor line 3 by 20%' rather than 'use AI to improve operations' — it is impossible to scope a deployment or estimate its value. Vendor conversations reinforce this problem by leading with platform breadth rather than problem specificity.

- Implementation cost uncertainty. When the use case is undefined, implementation cost estimates are necessarily wide. Finance teams cannot approve capital with a $500K–$5M cost range depending on scope. The cost uncertainty is not a pricing problem — it is a consequence of the use case clarity problem.

- Talent gaps. Most warehouse operations teams do not have in-house data science or ML engineering capability. Deploying AI requires either hiring talent that is scarce and expensive or selecting vendors whose platforms abstract that complexity — which requires enough AI literacy to evaluate vendor claims, which circles back to the comprehension problem.

- Budget constraints. Budget constraints are real, but they are the last barrier in the sequence, not the first. Operations leaders who have resolved the use case clarity and ROI estimation problems are generally able to secure budget. The barrier is rarely 'we have no money' — it is 'we cannot build a credible business case to compete for the money.'

Workforce Reskilling as a Co-Equal Investment Priority

One of the most significant year-over-year shifts in the 2025 report is the 13-percentage-point jump in workforce reskilling and retention investment — from 25% of leaders prioritizing it in 2024 to 38% in 2025. That shift is not a labor market story. It is an AI adoption prerequisite story.

AI deployments in warehouse environments do not replace the human workforce wholesale — they change the skill profile required. Workers who previously executed repetitive physical tasks need to shift toward exception handling, system monitoring, and data interpretation. Leaders who are investing in reskilling are not doing so out of altruism; they are recognizing that AI systems without trained operators produce outcomes that underperform their technical potential.

For warehouse operations leaders building an AI roadmap, the reskilling investment data suggests that talent readiness timelines need to run parallel to technology deployment timelines — not follow them. A workforce development plan that begins after system installation is structurally too late.

Agentic AI: From Concept to Warehouse Floor

The MHI 2025 report introduced agentic AI as a distinct category — not simply a more capable version of existing AI tools, but a qualitatively different operational mode. The report's definition centers on autonomous AI agents that can execute assigned tasks independently: acquiring and processing multi-modal data, using available tools to complete tasks, and coordinating with other AI agents without requiring human initiation at each step.

The scale of projected adoption is significant. Gartner projects that by 2028, 33% of enterprise software platforms will include agentic AI — up from approximately 1% in 2024. The same projection estimates that 15% of day-to-day work decisions will be made autonomously. These are not warehouse-specific figures, but the warehouse function — with its high volume of repetitive, rule-governed decisions — is among the environments where autonomous decision-making is most operationally tractable.

Several deployments highlighted at ProMat 2025 illustrate what agentic AI looks like in production warehouse environments:

- sSy.AI's SCOTi platform launched a new version at ProMat 2025 specifically designed for the material handling industry. The platform enables warehouse operators to query warehouse data in natural language and receive actionable insights — reducing the analytical intermediary layer between operational data and operational decisions.

- Dexory's DexoryView platform uses 14-meter autonomous mobile robots (AMRs) to continuously scan warehouse inventory and feed a real-time digital twin. The system provides visibility into stock levels, location accuracy, and space utilization without requiring human-initiated cycle counts — with IKEA among its documented deployments.

- Verity's AI-powered drone system is deployed across more than 150 warehouse sites globally, including IKEA. The system uses autonomous drones for inventory scanning and is testing an RFID-based approach with documented 99.9% accuracy. The scale of deployment — 150+ production sites — distinguishes this from a pilot-stage technology.

Agentic AI is probably going to be one of the biggest revolutions in logistics that we've seen since the invention of the forklift and the pallet. — Andrei Danescu, CEO, Dexory

The common thread across these deployments is that agentic AI in warehouse settings is not replacing the entire operation — it is eliminating specific high-friction tasks (cycle counting, exception routing, data querying) that consume disproportionate labor time relative to their decision complexity. That scoping is important for warehouse leaders evaluating entry points: the question is not 'how do we make our entire warehouse agentic?' but 'which specific repetitive decision processes are candidates for autonomous execution?'

Using These Benchmarks: A Calibration Tool for 2025 and Beyond

The MHI 2025 report data is most useful not as a set of statistics to cite but as a peer comparison instrument. The 700+ respondent base — predominantly executive-level leaders at companies with $50M+ in revenue — provides a relevant reference population for most mid-to-large warehouse operations organizations.

The practical calibration questions the data supports are specific: Is your organization among the 28% currently using AI, or the 72% that are not? If not, which of the four barriers (use case clarity, cost uncertainty, talent gaps, budget constraints) is the binding constraint? Is your technology investment budget above or below the $13M normalized baseline for your peer group? Are you among the 38% investing in workforce reskilling, or the 62% that are not yet treating it as a co-equal priority?

As forward-looking context — clearly labeled as data from the separately published MHI 2026 Annual Industry Report — the trajectory predicted in the 2025 data is already materializing. By the time the 2026 report was released in April 2026, current AI adoption had risen to 41%, and 48% of leaders rated AI's disruptive impact as significant or greater — a 25-percentage-point increase from the 2025 reading.

| Metric | MHI 2025 Report (700+ respondents) | MHI 2026 Report (500 respondents) |

|---|---|---|

| Current AI adoption | 28% | 41% |

| AI impact rated significant or greater | ~23% (implied) | 48% (+25pp) |

| Leaders increasing tech budgets | 55% | 56% |

| Planning to spend over $1M | 60% | 52% |

| Planning to spend over $10M | 19% | 17% |

John Paxton's observation at Modex 2026 captures the pace of this shift in terms that warehouse leaders will recognize:

Two years ago we discussed what is AI. Last year, generative AI. This year, agentic AI. — John Paxton, CEO, MHI (Modex 2026 keynote)

The 28%-to-82% gap documented in the 2025 report is not a distant horizon. The 2026 data confirms it is already narrowing. For warehouse directors who have been in evaluation mode, the practical implication is that the population of peers who have moved from evaluation to deployment is growing faster than the annual report cycle captures — and the competitive asymmetry between early movers and late adopters in warehouse AI is beginning to compound.

Comments

Join the discussion with an anonymous comment.