An Oracle SCM AI features comparison only makes sense after separating two questions that vendors often blend together in demos. One question is whether a platform can cover enough supply chain work to reduce tool sprawl. The other is whether it gives planners the deepest demand sensing, scenario modeling, and AI-native planning experience. Oracle looks much stronger on the first question than on the second.

That distinction matters because Oracle Fusion Cloud SCM is not competing only as a planning tool. It is competing as a supply chain operating layer across procurement, manufacturing, maintenance, product lifecycle, logistics, order management, and related transactions. Blue Yonder, Kinaxis, and SAP IBP enter the comparison from different centers of gravity. Treating them as interchangeable “AI supply chain platforms” hides the decision a buyer actually has to make.

The comparison that matters first

The most useful starting point is not a feature tour. It is a source-aware comparison: what Oracle claims about functional availability, what external analysis says about planning and AI depth, how AI is priced, and how much architectural work sits behind the demo.

| Evaluation area | Oracle Fusion Cloud SCM | Blue Yonder | Kinaxis | SAP IBP |

|---|---|---|---|---|

| Functional AI breadth | Oracle rates itself “available” across 21 capability rows spanning procurement, manufacturing, EAM, PLM, WMS, TMS, contract management, and related SCM areas; this is Oracle’s own comparison and should be verified row by row. [1] | Oracle’s comparison shows gaps in manufacturing, EAM, PLM, and contract management; those ratings are Oracle’s characterization, not neutral proof of weak business value. [1] | Oracle’s comparison shows 10+ gaps, including no native manufacturing, EAM, PLM, or procurement; buyers should validate against Kinaxis’s actual deployment scope. [1] | Credible enterprise planning option, especially in SAP-centered landscapes; Oracle’s own comparison should not be treated as the final view of SAP fit. [1] |

| Planning and AI depth | ThreadMoat CHAIN scores Oracle at I=5 for integration, H=3 for planning depth, and A=3 for AI depth. [2] | ThreadMoat scores Blue Yonder at H=4 and A=5, pointing to stronger specialist AI depth than Oracle. [2] | ThreadMoat scores Kinaxis at H=5 and A=4, pointing to stronger planning depth than Oracle. [2] | Not scored in the cited CHAIN details used here; compare SAP IBP depth against the specific planning use cases under evaluation. |

| Commercial AI model | AI agents are positioned as included in the Fusion subscription, not a separate AI add-on fee; implementation work is still outside that simple licensing statement. [1] | Available materials characterize Blue Yonder AI as add-on products through its Orchestrator platform. [1] | Available materials characterize Kinaxis AI pricing as still uncertain because capabilities were in early pilot. [1] | Available materials characterize SAP Joule/IBP AI as separately licensed. [1] |

| Architecture | Oracle emphasizes one Fusion data model and security framework, with AI agents able to write back into Fusion applications. [1] | ThreadMoat’s architecture analysis points to Snowflake/Azure dependencies. [2] | ThreadMoat’s architecture analysis points to a Databricks partnership. [2] | Oracle’s comparison and available materials point to SAP Business Data Cloud as an additional data layer. [1] |

| Best-fit buying logic | Stronger when cross-functional coverage, transaction write-back, and commercial simplicity matter more than best-in-class planning depth. | Stronger when demand sensing, planning AI, and category-specific optimization are the center of the business case. | Stronger when concurrent planning, scenario speed, and planner adoption are the center of the business case. | Stronger when the supply chain planning estate is already anchored around SAP processes and data. |

There is also a credibility baseline. Oracle has been named a Leader in Gartner’s 2026 Magic Quadrant reports for supply chain planning solutions for both discrete and process industries, so the comparison should not start from the assumption that Oracle is merely an ERP vendor dabbling in planning. [3] The sharper question is where its enterprise-suite strengths stop being enough.

Oracle’s strongest AI claim is coverage

Oracle’s most defensible advantage is the number of supply chain domains where it can plausibly say AI belongs inside the same suite. Its own comparison rates Oracle as “available” across 21 capability rows, including areas that planning specialists often do not natively own: manufacturing, enterprise asset management, product lifecycle management, contract management, procurement, warehouse management, and transportation management. [1]

That breadth is not a minor procurement checkbox. In a large organization, the forecast is not an isolated artifact. It changes what procurement expedites, what manufacturing schedules, what logistics rebooks, what maintenance can afford to interrupt, and what customer service promises. A planning workbench that is excellent inside its own boundary can still leave teams negotiating handoffs through integrations, extracts, tickets, and exception spreadsheets.

Oracle’s 26B announcement also shows why the company is pushing the discussion from individual AI features toward agentic applications. Oracle described 12 agentic applications across 26B and 26C, including Design-to-Source Workspace, Production Shift Operations Workspace, and Sales Order Command Center, designed to coordinate multiple AI agents for more autonomous end-to-end execution. [4] The important part is not the phrase “agentic”; it is the attempt to move work across the seams where supply chain systems usually slow down.

Still, Oracle’s 21-row matrix should be used the way a serious buyer uses any vendor-authored comparison: as a checklist for scripted validation, not as a verdict. A row marked available can hide wide differences in workflow depth, configurability, performance under real data volumes, exception handling, and planner trust. If a team cares about transportation tendering, supplier risk review, maintenance scheduling, or contract clause analysis, it should make Oracle demonstrate that flow with its own roles, security rules, master data issues, and approval paths.

- Ask Oracle to show the claimed AI capability inside the transaction flow where users will actually work, not in a detached assistant window.

- Confirm whether the AI output can create, update, or recommend changes to the relevant Fusion object, and who approves the write-back.

- Check whether the same security model governs the AI action, the source data, and the transaction it touches.

- Test cross-functional handoffs, such as a planning exception that becomes a procurement action, a production shift decision, or an order promise change.

- Separate “available somewhere in the suite” from “mature enough for this operating process.”

Where specialists still pull ahead

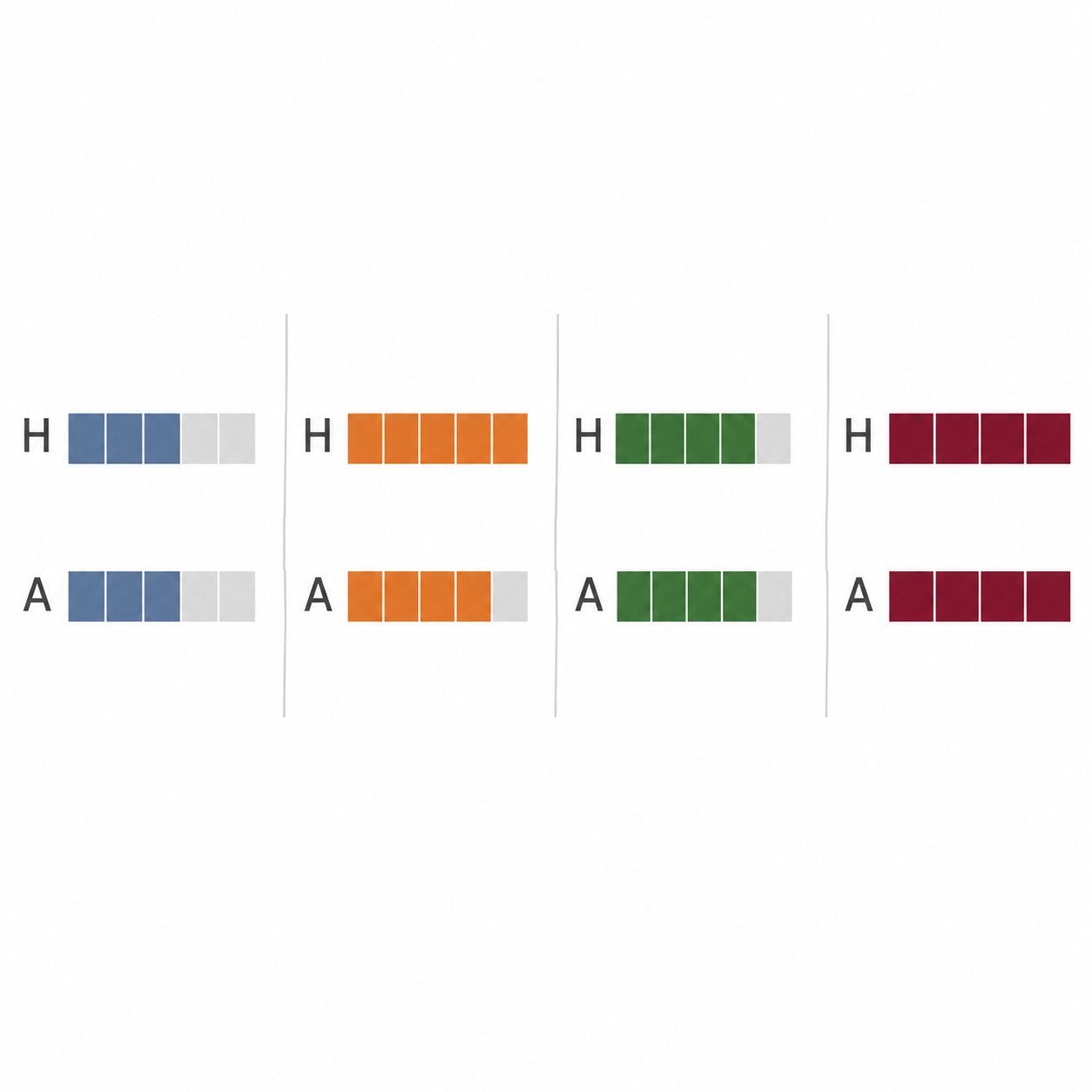

Breadth and maturity are not the same thing. This is where ThreadMoat’s June 2026 CHAIN framework becomes useful as a counterweight to Oracle’s comparison page. In that framework, Oracle scores I=5 for integration but H=3 for planning depth and A=3 for AI depth. Kinaxis scores H=5 and A=4, Blue Yonder scores H=4 and A=5, and o9 scores H=5 and A=5. [2]

Those scores should not be treated as a universal ranking. They are one analyst methodology. But they line up with a pattern many buyers recognize: Oracle’s suite argument is strongest when integration is the pain; specialist platforms are harder to dismiss when the planning organization is asking for sharper demand sensing, faster scenario comparison, and more advanced AI-native modeling.

For a planning-heavy organization, that difference is not academic. If a demand planning team lives inside promotion volatility, constrained supply, short decision windows, and constant scenario tradeoffs, the daily experience of the planning engine matters more than whether the same vendor also owns EAM or contract management. A better integrated suite can still lose if planners do not trust the recommendations or if scenario work takes too long to be useful.

Kinaxis is most dangerous to Oracle when concurrency and scenario speed sit at the center of the decision. Blue Yonder is most dangerous when demand sensing and AI-driven planning depth are the center of gravity. SAP remains credible where the broader enterprise landscape already runs through SAP and the cost of moving planning context outside that architecture would be high. Oracle’s advantage is real, but it is not the same advantage those platforms are selling.

Pricing: included AI is useful, not free transformation

Oracle’s pricing message is unusually clean for AI: AI agents are positioned as included in the Fusion subscription at no additional fee. [1] Against SAP Joule/IBP separate licensing, Blue Yonder AI add-ons through Orchestrator, and Kinaxis AI pricing uncertainty while capabilities were still in early pilot, that simplicity matters. A buyer can at least avoid a separate AI line item becoming the first fight.

But subscription inclusion should not be confused with low total cost. The license may include the AI agent capability, while the program still pays for data cleanup, role design, integration testing, change management, process redesign, consulting support, release management, and user training. The cited sources do not provide production ROI metrics or adoption rates for Oracle SCM AI features, so benefit claims should stay at the capability level unless a buyer has its own measured pilot data.

The practical procurement question is narrower: will Oracle’s included AI reduce commercial friction enough to let the team test more use cases earlier? In many enterprises, the answer may be yes. That still leaves the harder implementation question: whether the organization has enough process discipline and data quality for those agents to do useful work.

Architecture decides how much the demo has to hide

Oracle’s architecture pitch is straightforward: AI runs on the same Fusion data model and security framework as the core applications, and agents can write back transactions directly into Fusion workflows. [1] For IT architects, that is not just cleaner messaging. It can reduce the number of places where identity, access, lineage, exception handling, and transaction ownership have to be reconciled.

The competing architectures are not automatically worse. SAP’s Business Data Cloud layer, Blue Yonder’s Snowflake/Azure dependencies, and Kinaxis’s Databricks partnership can be rational choices, especially when a company wants specialist planning power and is comfortable operating a more distributed data architecture. [1][2] The tradeoff is that every additional layer has to earn its place through better planning outcomes, not just a more impressive AI story.

This is where an Oracle shortlist often becomes appealing to the people who will own the platform after selection. If procurement, planning, manufacturing, logistics, and IT each buy the tool that looks best in isolation, the enterprise may spend the next two years harmonizing item masters, supplier records, location hierarchies, calendars, security roles, and exception definitions. Oracle’s single-platform argument speaks directly to that fatigue.

How to read Oracle’s AI feature list without overbuying it

Oracle documentation presents a broad and growing list of AI features by release across Fusion applications; available materials characterize the count as 100+ features, while noting that release labels and GenAI versus AI agent categorization are not always perfectly consistent. [5] That is enough to show direction of investment. It is not enough to prove that every feature has equal production value.

A cleaner evaluation method is to map AI features to the decisions that create cost, service risk, or working-capital exposure. For example, a hypothetical electronics manufacturer might care less about the number of AI suggestions available and more about whether a supply disruption can trigger a constrained-plan review, a supplier communication, a production resequencing option, and an order-impact explanation without four teams rebuilding the same facts in different tools. The example is hypothetical; the evaluation logic is the point.

| If the decision depends on... | Oracle deserves more weight when... | A specialist deserves more weight when... |

|---|---|---|

| Cross-functional execution | The AI action must move from planning into procurement, manufacturing, logistics, or order management inside one governed transaction model. | The process can tolerate integration handoffs because planning quality is the overriding requirement. |

| Demand sensing and forecast refinement | The organization needs adequate AI support inside a broader SCM suite. | The planning team needs the strongest available specialist capability and will measure forecast and scenario performance closely. |

| Scenario planning | Scenarios are important but not the sole reason for buying the platform. | Fast concurrent scenario comparison is central to daily planning work. |

| Commercial simplicity | Included AI licensing helps the organization test use cases without separate AI add-on negotiations. | The business case can justify add-on or specialist pricing because the planning payoff is specific and measurable. |

| Data and security model | A single Fusion model reduces risk, governance work, and integration load. | The enterprise already has the architecture skill and appetite to support separate data layers for deeper planning capability. |

The buying answer is narrower than the vendor slides

Oracle is the stronger fit when the organization wants broad SCM coverage, embedded AI pricing, direct transaction write-back, and a common data and security model across supply chain functions. It is especially compelling when the real pain is not that one planning model is missing, but that too many functions are operating from partially reconciled systems.

Kinaxis or Blue Yonder should stay high on the shortlist when planning precision is the business case. If demand sensing quality, concurrent scenario speed, planner trust, and AI-native modeling determine value, the ThreadMoat scores explain why specialists still have a strong argument. [2] SAP belongs in the evaluation for SAP-centered enterprises, but the decision should be made on current planning fit and architecture, not on generic ERP loyalty.

So the useful conclusion is not that Oracle wins or loses the AI supply chain market. Oracle’s AI advantage is coverage plus commercial simplicity plus architecture. The specialists’ advantage is depth where planning teams feel the difference every day. The right shortlist depends on which of those costs the business is actually trying to reduce.

References

- Oracle vs. Competition, Oracle, https://www.oracle.com/scm/oracle-vs-competition/

- Best SCM Software 2026, DemystifyingPLM, June 2026, https://www.demystifyingplm.com/best-scm-software-2026

- Oracle Named a Leader in Two 2026 Gartner Magic Quadrant Reports for Supply Chain Planning Solutions, Oracle, April 8, 2026, https://www.oracle.com/news/announcement/oracle-named-a-leader-in-two-2026-gartner-magic-quadrant-reports-for-supply-chain-planning-solutions-2026-04-08/

- Oracle Fusion Cloud SCM 26B: Advancing Autonomous Supply Chains with Built-in AI, Oracle Blog, https://blogs.oracle.com/scm/oracle-fusion-cloud-scm-26b-advancing-autonomous-supply-chains-with-built-in-ai

- AI for Supply Chain Management, Oracle Help Center, https://docs.oracle.com/en/cloud/saas/fusion-ai/aiafl/ai-scm.html

Comments

Join the discussion with an anonymous comment.